Asahi Kasei (3407) is building a strong early position in the green hydrogen market by leveraging its electrolysis technology, scaling production in domestic and European markets, and differentiating through resilient multi‑stack design, low‑cost catalysts, and long‑standing industrial customer relationships. Nonetheless, due to its diversified business mix and the presence of mature, low‑growth segments, it continues to trade at relatively low valuation levels compared to material‑sector peers involved in AI‑driven demand and Japan‑led strategic investment projects in the United States.

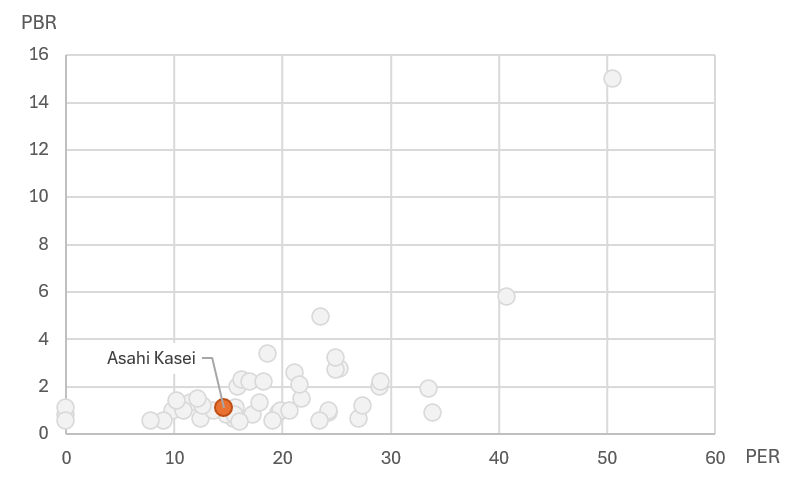

PER vs PBR Comparison: Asahi Kasei and Nikkei 225 Materials Sector

Notes: Data based on Nikkei as of March 26th, 2026. Price-to-book ratio (PBR) compares a company’s market value with the book value of its net assets, indicating how much investors are willing to pay relative to the firm’s underlying equity. Lower PBRs often signal undervaluation or structural challenges, while higher PBRs reflect strong confidence or expected future growth. Price-to-earnings ratio (PER) measures how expensive a stock is relative to its current earnings, showing how much investors pay for one unit of profit. Companies with low PERs are typically viewed as value stocks with limited near‑term growth expectations, whereas high‑PER firms are seen as having stronger growth prospects or higher investor optimism.

History and Strategic Positioning

Asahi Kasei’s alkaline water electrolysis business traces its roots back to 1923, when the company produced hydrogen using electricity from its own hydropower plant. Its technological foundation was strengthened through the launch of its ion‑exchange membrane chlor‑alkali business in 1975. Since 2010, Asahi Kasei has accelerated development of alkaline electrolysis for green hydrogen and, through NEDO‑supported demonstrations, successfully commercialized a 10‑MW‑class system. The business is now designated as a strategic growth domain in the company’s mid‑term plan, targeting revenues of around ¥100 billion (approx. USD 625 million) by 2030.

Domestic Deployment (Fukushima & Kawasaki)

In Japan, Fukushima and Kawasaki serve as the core hubs for technology validation and scale‑up. At Fukushima’s FH2R, a hybrid operation combining solar power and grid electricity is used to test responsiveness to variable renewable energy and verify the reliability of large‑scale stacks, while also supporting integrated green ammonia synthesis. In Kawasaki, a 0.8‑MW × 4 multi‑module system is being used to establish scale‑up technologies toward 100‑MW‑class systems, alongside construction of a new plant—scheduled for 2028—that will provide more than 3 GW of annual production capacity and form the backbone of commercial supply.

Overseas Deployment (Finland & Germany)

Internationally, Finland and Germany anchor Asahi Kasei’s commercial expansion and demand creation. In Finland, a 1‑MW containerized system has been installed next to a hydrogen refueling station to demonstrate a cold‑climate, localized production‑and‑use model—positioned as the company’s first commercial unit for distributed, small‑scale applications. In Germany, Asahi Kasei supplies green hydrogen to chemical manufacturers as a replacement for gray hydrogen, securing stable industrial demand. The company also participates in SAF production and CO₂‑utilization projects, broadening its role as a provider of decarbonization solutions.

Competitive Advantages (Technology, Cost, Customer Base)

Asahi Kasei’s competitive strengths lie in the operational resilience of its multi‑stack architecture, the cost advantage of not relying on precious‑metal catalysts, and the synergies derived from decades of chlor‑alkali operations and customer relationships. In particular, the ability to support industrial users transitioning from gray to green hydrogen provides a stable demand pathway and mitigates risks in a market where growth remains gradual.

By strengthening its technical and production base in Japan while advancing commercialization and demand creation overseas, Asahi Kasei is establishing a solid position in the early green hydrogen market. With a scalable product lineup and a strong industrial customer network, the company is well‑placed to compete as global demand accelerates.

Hydrogen Strategy and Market Valuation Gap

Yet the market has been slow to price in these strengths. As of March 26th, 2026, Asahi Kasei appears relatively undervalued within the Nikkei 225 materials sector, trading around 15x PER and 1x PBR, while peers such as Fujikura, Furukawa Electric, and Mitsubishi Materials command higher valuations due to their direct exposure to structural growth drivers like AI servers, data centers, semiconductor materials, and Japan‑led strategic investment projects in the United States. Despite having promising growth areas of its own—such as hydrogen electrolysis systems, battery separators, and healthcare—Asahi Kasei continues to be viewed by the market as a diversified general chemical manufacturer, where a broad mix of businesses and the presence of mature, low‑growth segments dilute the visibility of its growth story and weigh on overall profitability metrics. As a result, investors find it harder to identify a clear, dominant growth engine, leaving the company’s valuation multiples lower than those of materials companies more tightly aligned with AI‑driven and policy‑supported demand.

Financial Benchmark: Six Major Japanese Companies in Materials Sector (USD-based estimates)

| Name (ticker) | USD Million Estimates | Asahi Kasei (3407) | Teijin (3401) | Toray (3402) | Fujikura (5803) | Furukawa (5801) | Mitsubishi Materials (5711) |

| Financials | Equity Ratio | 48% | 39% | 50% | 57% | 37% | 25% |

| Financials | Debt with Interests | 6,862 | 2,266 | 5,888 | 783 | 1,984 | 4,286 |

| Cash Flow | Operating Cash Flow | 18,838 | 4,363 | 15,938 | 7,244 | 3,738 | 3,675 |

| Cash Flow | Cash and Equivalent | 24,375 | 6,719 | 14,825 | 11,513 | 4,125 | 5,538 |

| Sales | 2023 | 17,041 | 6,367 | 15,558 | 5,040 | 6,665 | 10,162 |

| Sales | 2024 | 17,405 | 6,455 | 15,404 | 4,999 | 6,603 | 9,629 |

| Sales | 2025 | 18,983 | 6,284 | 16,021 | 6,121 | 7,511 | 12,263 |

| Forecast | 2026 | 19,156 | 5,375 | 16,250 | 7,144 | 8,125 | 11,000 |

| Forecast | 2027 | 19,988 | 5,063 | 17,375 | 7,813 | 8,875 | 10,938 |

Notes: All USD values are converted at 1 USD = 160 JPY. Equity ratios are presented as reported. Debt with interests refers to interest-bearing liabilities including borrowings and bonds. Sources: Company financial statements and securities reports (FY2023–FY2025), company earnings presentations and IR materials, forecast values based on company guidance and market analyst estimates, data referenced from Toyo Keizai Shinpo-sha’s Shikiho (Japan Company Handbook as of Spring 2026), and exchange rate assumptions based on Ministry of Finance and market averages (2024–2025).

Japanese translations

Title: 旭化成のアルカリ水電解事業:国内外展開と競争優位性の実像

旭化成のアルカリ水電解事業は、1923年の創業期に自社水力発電を使って水素を製造した歴史を起点とし、1975年の食塩電解事業化で培った電解技術を基盤に発展してきた。2010年以降はグリーン水素向けアルカリ水電解の開発を本格化し、NEDO実証を通じて10MW級の大型装置を実用化。現在は中期経営計画で「戦略的育成事業」と位置づけられ、2030年に1,000億円規模の売上を目指す成長領域となっている。

事業展開は福島・川崎・フィンランド・ドイツの4拠点で用途別に進む。福島では太陽光と系統電源を組み合わせたハイブリッド運転でグリーン水素を製造し、変動電源への追従性を実証。川崎では0.8MW×4のマルチモジュール設備で100MW級へのスケールアップ技術を確立しつつ、電解枠・膜の新工場建設で年間3GW超の生産体制を構築する。フィンランドでは1MW級コンテナ型装置を水素ステーション隣接地に設置し、寒冷地での地産地消モデルを実証。ドイツでは化学メーカー向けにグレー水素代替のグリーン水素供給を進め、産業用途での安定需要を確保している。

競争優位性は、①複数スタック構成による高い運転継続性(不具合スタックを切り離しても製造継続可能)、②貴金属不使用によるコスト優位性と大規模展開のしやすさ、③食塩電解事業との技術・顧客基盤シナジーの3点に集約される。特に既存の化学メーカーとの関係性を活かした「グレー水素のグリーン化」需要の取り込みは、需要立ち上がりが緩やかな市場環境において事業リスクを抑える戦略として機能している。旭化成は100MW超級システムやマレーシアでの大規模案件を次のステップとし、分散型から大規模まで対応可能なスケーラブルな水電解サプライヤーとしての地位確立を目指している。

それでも、市場はこうした強みを十分に織り込むのが遅れている。旭化成は日経225の素材セクター内で相対的に割安に評価されており、PERは約15倍、PBRは1倍前後で推移している。一方、フジクラ、古河電工、三菱マテリアルといった企業は、AIサーバー、データセンター、半導体材料、さらには日本主導の対米戦略投資プロジェクトといった構造的な成長ドライバーに直接関与していることから、より高いバリュエーションを獲得している。旭化成自身も水素電解システム、電池セパレータ、ヘルスケアなど有望な成長領域を持つものの、市場では依然として総合化学メーカーとして認識されており、多角化した事業構成や成熟した低成長セグメントの存在が成長ストーリーの見えにくさや収益性指標の伸び悩みにつながっている。その結果、投資家は明確な成長エンジンを見出しにくく、AI関連や政策支援の恩恵をより直接受ける素材企業と比べて、同社のバリュエーションは低位にとどまっている。

素材セクターに属する主要6社の財務ベンチマーク

| Name (ticker) | JPY Million | 旭化成(3407) | 帝人 (3401) | 東レ (3402) | フジクラ(5803) | 古川電 (5801) | 三菱マテリアル(5711) |

| 財務 | 自己資本比率 | 48% | 39% | 50% | 57% | 37% | 25% |

| 財務 | 有利子負債 | 1,097,915 | 362,548 | 942,123 | 125,232 | 317,465 | 685,689 |

| キャッシュフロー | 営業 Cash Flow | 3,014,000 | 698,000 | 2,550,000 | 1,159,000 | 598,000 | 588,000 |

| キャッシュフロー | 現金同等物 | 3,900,000 | 1,075,000 | 2,372,000 | 1,842,000 | 660,000 | 886,000 |

| 売上高 | 2023年 | 2,726,485 | 1,018,751 | 2,489,330 | 806,453 | 1,066,326 | 1,625,933 |

| 売上高 | 2024年 | 2,784,878 | 1,032,773 | 2,464,596 | 799,760 | 1,056,528 | 1,540,642 |

| 売上高 | 2025年 | 3,037,312 | 1,005,471 | 2,563,280 | 979,375 | 1,201,762 | 1,962,076 |

| 予想 | 2026年 | 3,065,000 | 860,000 | 2,600,000 | 1,143,000 | 1,300,000 | 1,760,000 |

| 予想 | 2027年 | 3,198,000 | 810,000 | 2,780,000 | 1,250,000 | 1,420,000 | 1,750,000 |

注記:有利子負債(Debt with interests)は、借入金や社債などの利息負担のある負債を指す。出典:各社の財務諸表および有価証券報告書(FY2023〜FY2025)、決算説明資料およびIR資料、企業ガイダンスおよび市場アナリスト予測に基づく数値、東洋経済新報社『会社四季報』(2026年春号)、および財務省・市場平均に基づく為替前提(2024〜2025年)。

(References)

- 旭化成株式会社「旭化成が目指す水素社会、世界をリードする水素製造技術」Tomorrow’s Stories(https://www.asahi-kasei.com/jp/asahikasei-brands/stories/hydrogen.html)

- 旭化成株式会社「川崎製造所における水素製造用アルカリ水電解パイロット試験設備を本格稼働」2024年5月14日プレスリリース(https://www.asahi-kasei.com/jp/news/2024/ze240514.html)

- 旭化成株式会社「フィンランドの水素プロジェクトにコンテナ型アルカリ水電解システムAqualyzer™-C3を供給」2025年7月30日プレスリリース(https://www.asahi-kasei.com/jp/news/2025/ze250730.html)

- 旭化成株式会社「フィンランドの水素プロジェクトでコンテナ型アルカリ水電解システムAqualyzer™-C3の設置開始」2026年プレスリリース(https://www.asahi-kasei.com/jp/news/2025/ze260312.html)

- 旭化成株式会社「クリーン水素製造用アルカリ水電解システムの生産能力を拡大」2025年10月23日プレスリリース(https://www.asahi-kasei.com/jp/news/2025/ze251023.html)

- 旭化成株式会社「旭化成が製造する水素を用いた日揮HDのグリーンアンモニア実証プラントが始動」2025年プレスリリース(https://www.asahi-kasei.com/jp/news/2025/ze260128.html)

- 旭化成株式会社「Aqualyzer™ 水素製造アルカリ水電解システム」製品サイト(https://ak-green-solution.com/)

- 旭化成株式会社「水素製造用アルカリ水電解パイロット試験設備の着工について」2022年11月7日プレスリリース(https://www.asahi-kasei.com/jp/news/2022/ze221107.html)

- 旭化成株式会社「水素社会に向けた取組」第28回水素・燃料電池戦略協議会資料(2023年3月6日)(https://www.meti.go.jp/shingikai/energy_environment/suiso_nenryo/pdf/028_05_00.pdf)

- 旭化成株式会社「水素社会の実現に向けた取組み」2025年1月31日(https://www.tokyo-h2-navi.metro.tokyo.lg.jp/assets/pdf/torikumi/event/haneda-minnanomirai/document_05.pdf)

- NEDO「大規模アルカリ水電解水素製造システムの開発およびグリーンケミカルプラントの実証」成果発表(https://www.nedo.go.jp/content/100980855.pdf)

- 日本化学工業協会「SDGs事例集2019 旭化成のアルカリ水電解システム」(https://www.nikkakyo.org/sites/default/files/alkaline_water_electrolysis_system.pdf)

- 日経新聞「旭化成、水素製造用膜の新工場 兼用設備でリスク軽減」2024年12月18日

- 日経新聞「旭化成、再エネ使いグリーン水素を安価に量産 設備コスト3分の1に」2025年2月17日

- 日経新聞「旭化成、水素製造システムで初の商用受注 フィンランドで26年稼働」2025年7月30日

- ニュースイッチ(日刊工業新聞)「旭化成は10万キロ級アルカリ水電解装置狙う」(https://newswitch.jp/p/43266)

- JETRO「グリーン水素で世界の水素利用牽引役を目指すドイツ」地域・分析レポート(https://www.jetro.go.jp/biz/arearepoareareports/2020/e8e7735fb91b5047.html)