The world’s largest hydrogen subsidy program is underway — but the data reveals a fundamental tension between Japan’s net-zero ambitions and the fossil-fuel-derived reality of what is actually being funded.

Key Metrics of Japan’s Hydrogen Contract for Difference (CfD) Program

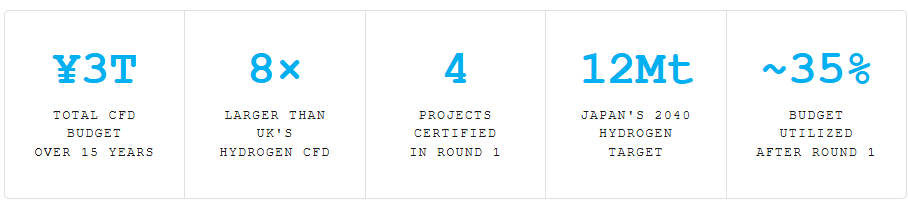

Notes: Japan’s hydrogen CfD program allocates a total budget of ¥3 trillion (around USD 20 billion) over 15 years, positioning it among the world’s largest schemes, with annual support levels estimated to be roughly eight times those of the UK and significantly above France and Australia. The first allocation round certified four projects, including two domestic initiatives announced by METI in September 2025. Japan also targets a major scale‑up of hydrogen use to 12 million tonnes per year by 2040—around six times today’s level—while early awards indicate that only about 35% of the CfD budget has been committed so far, leaving substantial room for future rounds.

How the CfD Works

Japan’s Hydrogen Society Promotion Act1, enacted May 2024 and in force since October 2024, introduced a supply-side subsidy modeled on the UK’s offshore wind Contract for Difference (CfD) mechanism. The principle: low-carbon hydrogen costs

more to produce than the fossil fuels it replaces. The CfD bridges that price gap with public funds administered by JOGMEC, giving investors 15-year revenue certainty.2

The scheme covers hydrogen, ammonia, e-methane, and synthetic fuels that meet a carbon intensity threshold of 3.4 kg CO₂ per kg H₂ (well-to-gate)3 — a 70% reduction versus fossil comparators, consistent with European standards.4 Crucially, Japan measures at the point of production, not consumption — a distinction with significant implications for the lifecycle accounting of imported blue hydrogen.5

After the 15-year support period ends, certified suppliers must continue delivering hydrogen for an additional 10 years6 — a design feature intended to ensure market continuity, but one that creates a 25-year lock-in of supply chain infrastructure decisions made today.

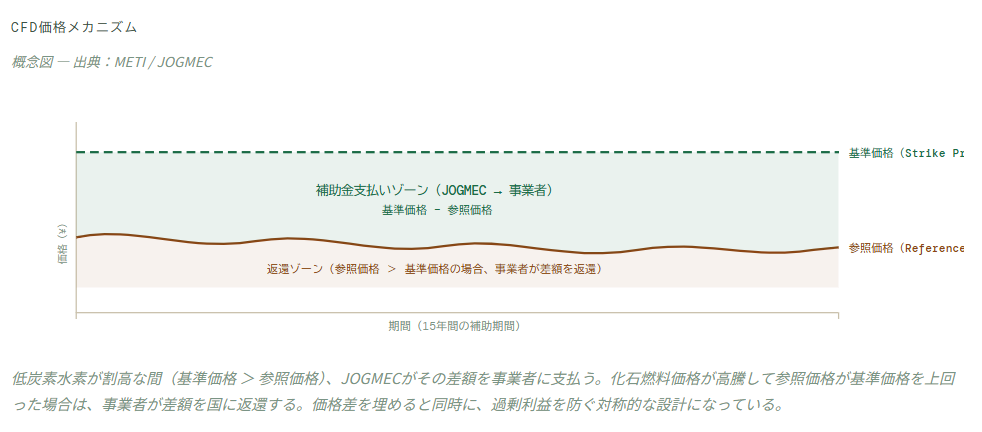

CfD Price Mechanism simplified illustration

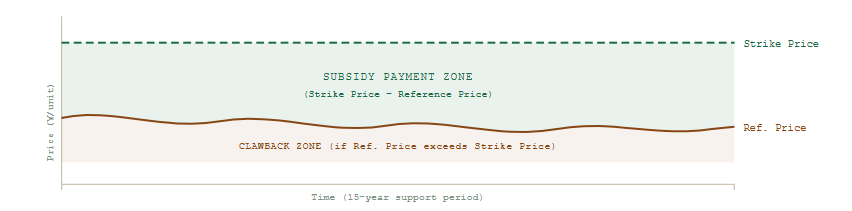

source: METI / JOGMEC Notes: Japan’s hydrogen CfD works by guaranteeing suppliers a “Strike Price” — the level needed to recover production, import, and delivery costs with a reasonable return — while benchmarking it against a fluctuating “Reference Price,” the landed cost of the fossil fuel being replaced. When low‑carbon hydrogen is more expensive (Strike > Reference), JOGMEC pays the difference; when fossil fuels become costlier (Reference > Strike), suppliers must return the surplus, preventing windfall gains. In essence, the CfD bridges today’s cost gap between hydrogen and fossil fuels while ensuring symmetrical clawbacks if market conditions reverse.

What Round 1 Actually Certified

As of December 2025, four projects have been certified.7 The first two — small domestic projects — were selected in September 2025. The high-profile JERA and Mitsui awards followed in December, marking the first large-scale international supply chain projects under the program.8

Table 1. Round 1 certified projects as of December 2025

| Lead | Type | Volume | Origin | End Use | Start |

|---|---|---|---|---|---|

| Toyota Tsusho consortium | Green H₂ | 1,600 t/yr | Wind, electrolysis | Aichi Steel (industrial) | 2030 |

| Resonac + Nippon Shokubai | Low-carbon NH₃ | 20,000 t/yr | Waste plastic gasification | Acrylonitrile production | 2030 |

| JERA consortium | Blue NH₃ | 500,000 t/yr | Blue Point, Louisiana (US) | Coal co-firing, Hekinan | Feb 2030 |

| Mitsui consortium | Blue NH₃ | 280,000 t/yr | Blue Point, Louisiana (US) | Coal co-firing, Hokkaido + industrial | Jan 2031 |

Sources: S&P Global,7 Wood Mackenzie.9

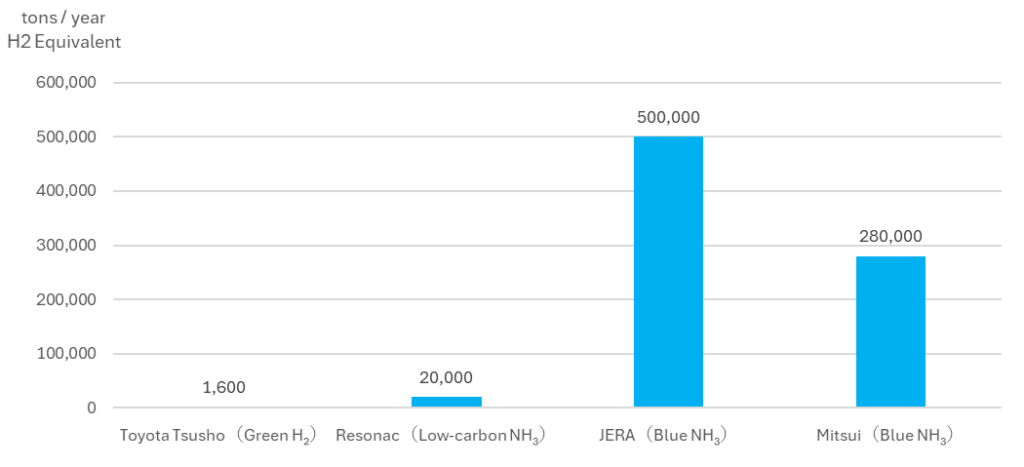

Round 1 certified volume by project tons/yr, hydrogen equivalent

Source: S&P Global, Wood Mackenzie

The volume asymmetry is stark. The two blue ammonia projects from Louisiana account for roughly 98.5% of all Round 1 certified volume.9 The sole green hydrogen project — Toyota Tsusho’s wind electrolysis plant in Aichi — represents just 1,600 t/yr out of approximately 123,000 tons of hydrogen equivalent in total.

Other data suggests 27 proposals were submitted to Round 1 — collectively exceeding the total available CfD budget. The selection process delayed awards by approximately nine months beyond the March 2025 submission deadline.10

Three Tensions the Data Reveals

Japan’s CfD is, by most measures, the most ambitious hydrogen subsidy program in the world. Yet a close reading of its design, first-round outcomes, and independent research identifies three unresolved tensions that will determine whether ¥3 trillion delivers on its decarbonization promise — or becomes an expensive lock-in of transitional infrastructure.

Annual hydrogen CfD support vs. peer economies

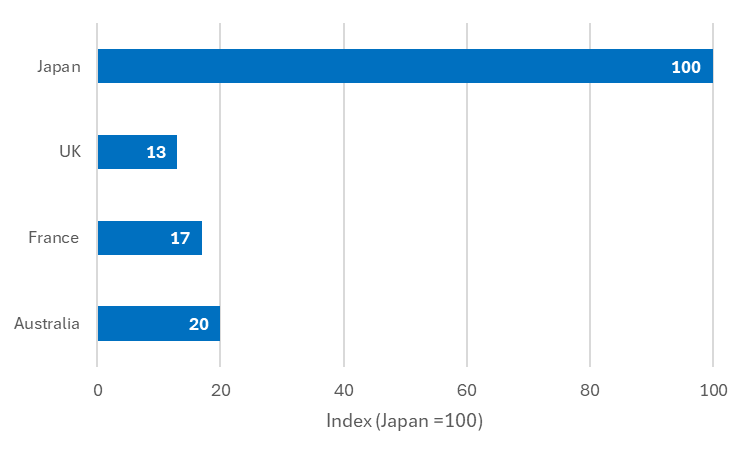

Index: Japan = 100 — Source: Trencher et al. (2026) Notes: Trencher et al. (2026) reports that Japan’s annual hydrogen CfD support is approximately 8×, 6×, and 5× larger than equivalent instruments in the UK, France, and Australia. Using Japan’s total CfD budget of ¥3 trillion (USD 19.2 billion) over 15 years—implying an annual average of roughly USD 1.3 billion—these multipliers suggest indicative annual support levels of around USD 160 million for the UK, USD 215 million for France, and USD 260 million for Australia. These figures are back‑calculated estimates only, as absolute values for peer economies are not disclosed, and each country’s support mechanism differs in structure and scope.

Tension 1 — Scale vs. sufficiency. ¥3 trillion is large in absolute terms and almost certainly insufficient relative to Japan’s own targets. According to a March 2025 report by the Green Hydrogen Organisation, ENEOS — one of Japan’s largest petroleum companies — assessed that the scheme would barely cover a fraction of what is needed to reach the 12 Mt/yr target by 2040.11 Per independent academic analysis, Japan’s annual CfD support is approximately 8× larger than the UK’s equivalent instrument, 6× France’s, and 5× Australia’s12 — yet the first round drew 27 proposals that already exceeded the total budget, suggesting the subsidy envelope is binding well before it can reshape the entire market.10

Tension 2 — Blue dominance vs. green trajectory. Round 1 awarded over 98% of certified volume to blue ammonia destined for coal power plant co-firing. This reflects a deliberate design choice: Japan’s carbon intensity standard is technology-neutral, and blue hydrogen (from natural gas with CCS) currently satisfies the 3.4 kg CO₂/kg threshold more cheaply than electrolytic green hydrogen.4 But locking in 25-year supply chains for blue ammonia from Louisiana creates a path dependency that may prove costly to unwind as electrolyzer costs fall and green hydrogen becomes price-competitive — potentially within the same 15-year support window. Green hydrogen production costs in Japan currently range between $3.0–$10.3/kg H₂, compared to $1.2–$2.3/kg for blue hydrogen produced via SMR with CCS.13

Tension 3 — Measurement methodology vs. real-world emissions. Japan’s well-to-gate standard means upstream methane leakage during natural gas extraction and transport is not fully captured in eligibility assessments. TransitionZero finds that 20% ammonia co-firing at coal plants would still generate nearly double the emissions of conventional gas-fired generation.14 The Breakthrough Institute notes that, depending on methane leakage rates, ammonia co-firing could in some scenarios exceed the emissions of simply burning coal.15 Japan’s government counters that rising carbon prices under the GX cap-and-trade scheme will correct these incentives over time16 — but the system becomes mandatory only for emitters above 100,000 t CO₂/yr in 2026–27, and its price trajectory remains uncertain.

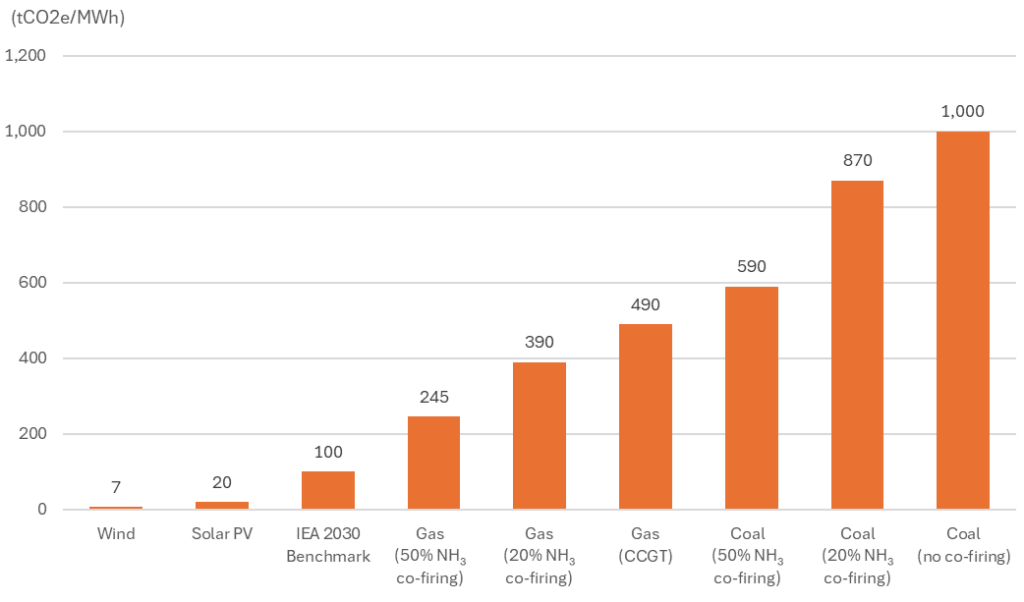

Indicative CO₂ emissions intensity by generation type

Notes: tCO₂-eq per MWh. Ammonia co‑firing offers a pathway for gradually reducing CO₂ emissions from existing thermal assets, with gas turbines showing proportional reductions as blend ratios increase: indicative estimates based on IEA blue‑ammonia factors suggest that 20% and 50% NH₃ co‑firing lower emissions to roughly 390 kg and 245 kg/MWh, even though both remain above the IEA’s 2030 net‑zero benchmark of ~100 kg CO₂‑eq/MWh. Coal units also achieve measurable reductions: TransitionZero finds that 20% co‑firing still emits nearly double Gas (CCGT) and around five times the net‑zero benchmark, while BNEF estimates that 50% co‑firing cuts emissions by ~40% relative to a pure‑coal baseline, though still above unabated gas at blend rates below 50%. These results highlight that ammonia co‑firing is not a net‑zero solution today, but it is a technology capable of incrementally lowering emissions, with the potential for deeper reductions as blend ratios rise and as upstream ammonia production—particularly methane leakage and CCS performance—continues to decarbonize. Sources: TransitionZero, IEA, Breakthrough Institute.

The Bull Bet

Wood Mackenzie notes that by stacking Japan’s CfD with US 45Q tax credits, the JERA/Mitsui Blue Point deals represent a genuinely cost-effective pathway to de-risk large-scale low-carbon ammonia supply.9 JERA achieved the world’s first 20% ammonia co-firing demonstration at Hekinan in 2024, with commercial operation targeted for fiscal year 2029–30.8

What to Watch in 2026

IRA uncertainty spillover: Japanese firms had structured US-based hydrogen projects around stacking CfD support with IRA incentives (particularly 45Q). Further rollback of US clean energy policy could redirect Japanese capital toward Middle Eastern, Australian, or domestic production.10

Remaining Round 1 awards: METI is expected to certify additional projects in spring–summer 2026 before closing out Round 1. Projects in the Middle East and India — including ACME’s green hydrogen scheme involving IHI — are reportedly under consideration.10 The green/blue ratio of remaining awards will be closely watched.

GX cap-and-trade launch: Mandatory participation for emitters above 100,000 t CO₂/yr begins 2026–2027.16 The carbon price trajectory will determine how quickly the CfD subsidy gap narrows without additional public funding.

Round 2 decision: A government decision on whether to launch a second CfD tranche will signal confidence in Round 1’s performance. No timeline has been confirmed; the review period is ongoing.10

Conclusions

Japan’s ¥3 trillion hydrogen CfD is a strong industrial policy that deliberately prioritizes building large‑scale supply chain infrastructure before tightening carbon standards. It was designed to treat all technologies equally and let the most cost‑effective options win. The real test is whether the system can stay aligned with climate goals, which hinges on strict oversight of upstream methane emissions in blue‑ammonia supply chains. Over the next 18 months, remaining awards, GX carbon‑price decisions, and tighter emissions rules will determine whether the ¥3 trillion program becomes the foundation of Japan’s hydrogen transition — or risks becoming an expensive bridge to a fossil‑fuel extension.

Japanese translations

Title:世界最大の水素補助金:3兆円CfDが示すデータの現実

世界最大規模の水素補助金プログラムが動き出した。しかしデータを精査すると、日本のネットゼロ目標と、実際に資金が投じられている化石燃料由来の現実との間に、根本的な緊張関係が浮かび上がる。

| ¥3T CfD総予算 (15年間) | 8× 英国の水素CfD より大きい規模 | 4 第1ラウンド認定プロジェクト数 | 12Mt 日本の2040年 水素利用目標 | ~35% 第1ラウンド後の 予算消化率 |

CfDの仕組み

2024年5月に成立し、同年10月に施行された水素社会推進法1は、英国の洋上風力向けCfD(差額決済契約)を参考にした供給側補助金制度を導入した。基本的な考え方はシンプルだ——低炭素水素の製造コストは、代替する化石燃料より高い。CfDはその価格差をJOGMEC(石油天然ガス・金属鉱物資源機構)が補填することで、事業者に15年間の収益確実性を与える。2

対象燃料は水素・アンモニア・e-メタン・合成燃料で、炭素集約度3.4 kg CO₂/kg H₂(ウェルトゥゲート基準)3以下が要件。化石燃料比で70%以上の削減に相当し、欧州基準とも整合する。4 ただし日本が採用する「生産地点」基準は、欧州の「消費地点」基準とは異なり、輸入ブルー水素のライフサイクル排出量の評価に重大な影響を及ぼす。5

補助期間の15年が終了した後も、認定を受けた事業者はさらに10年間の供給継続義務6を負う。市場の継続性を担保する設計だが、言い換えれば今日のサプライチェーン投資判断が25年間固定化されることを意味する。

第1ラウンドで実際に認定されたもの

2025年12月時点で、4件のプロジェクトが認定されている。7 最初の2件(小規模な国内プロジェクト)は2025年9月に選定。JERAと三井物産が主導する大規模案件は同年12月に認定され、同制度初の国際サプライチェーン案件となった。8

表1. 第1ラウンド認定プロジェクト(2025年12月時点)

| 主体 | 種別 | 供給量 | 調達元 | 用途 | 開始 |

|---|---|---|---|---|---|

| 豊田通商コンソーシアム | グリーンH₂ | 1,600 t/年 | 風力 電解、(愛知) | 愛知製鋼(産業用) | 2030年 |

| レゾナック+日本触媒 | 低炭素NH₃ | 2万 t-NH₃/年 | 廃プラスチックガス化 | アクリロニトリル製造 | 2030年 |

| JERAコンソーシアム | ブルーNH₃ | 50万 t/年 | ブルーポイント(米・ルイジアナ) | 石炭混焼、碧南火力 | 2030年2月 |

| 三井物産コンソーシアム | ブルーNH₃ | 28万 t/年 | ブルーポイント(米・ルイジアナ) | 石炭混焼(北海道)+産業用 | 2031年1月 |

出典:S&P Global 7、Wood Mackenzie 9

量的な非対称性は際立っている。ルイジアナ産のブルーアンモニア2案件だけで、第1ラウンド認定量の約98.5%を占める。9 グリーン水素は豊田通商の愛知案件のみで、総認定量(水素換算で約12万3,000 t/年)のうちわずか1,600 t/年にとどまる。

第1ラウンド認定プロジェクト別の水素製造量(t/年、H₂換算)

出典:S&P Global 7、Wood Mackenzie 9

データポイント

第1ラウンドには27件の提案が提出され、合計申請規模は総予算を上回った。2025年3月の申請締め切りから認定まで約9か月を要した。10

データが示す3つの緊張関係

多くの指標で見て、日本のCfDは世界で最も野心的な水素補助金プログラムだ。しかしその設計・第1ラウンドの結果・独立機関の研究を丁寧に読み解くと、3兆円が脱炭素化の約束を果たすのか、それとも高コストな「移行期インフラ」の固定化で終わるのかを左右する、3つの未解決の緊張関係が見えてくる。

緊張関係 1:規模 vs. 十分性

3兆円は絶対額では大きいが、日本自身の目標と比較すると、ほぼ確実に不足している。グリーン水素機構(GH2)の2025年3月レポートによれば、ENEOSをはじめとする業界関係者は、この補助金が2040年に向けた12 Mt/年目標を達成するために必要な規模のごく一部しかカバーできないと評価している。11 学術研究によれば、日本のCfD年間支援規模は英国の同等制度の約8倍、フランスの6倍、オーストラリアの5倍にのぼる。12 それでも第1ラウンドには予算総額を超える27件の提案が集まり、補助金の枠が市場全体を変える前に使い切られてしまうことを示唆している。10

日本の水素CfD支援額の国際比較(年次ベース)

注記:日本=100(指数) — 出典:Trencher (2026)Trencher et al.(2026)は、日本の水素CfDによる年間支援額が、英国・フランス・オーストラリアの同種制度と比べて、それぞれ約8倍、6倍、5倍の規模に達していると報告している。日本のCfD総予算は15年間で3兆円(192億ドル)であり、年平均に換算すると約13億ドルとなる。この前提に倍率を適用すると、英国は約1.6億ドル、フランスは約2.15億ドル、オーストラリアは約2.6億ドルの年間支援規模に相当する。ただし、これらはあくまで倍率から逆算した参考値であり、各国の絶対額は公表されていないうえ、制度の構造や対象範囲も国ごとに異なる点に留意が必要である。

緊張関係 2:ブルー支配 vs. グリーンへの軌跡

第1ラウンドの認定量の98%以上が、石炭火力の混焼向けブルーアンモニアに集中した。これは意図的な設計判断の結果だ。日本の炭素集約度基準は技術中立であり、CCS付き天然ガス由来のブルー水素は、電気分解によるグリーン水素より安価に3.4 kg CO₂/kgの閾値を満たせる。4 しかしルイジアナ産ブルーアンモニアへの25年間のサプライチェーン固定化は、電解槽コストの低下とともにグリーン水素が価格競争力を持つ将来——場合によっては同じ15年の補助期間内——に解消しにくい経路依存性を生む。日本のグリーン水素製造コストは現在3.0〜10.3ドル/kg H₂で、CCS付きSMRによるブルー水素の1.2〜2.3ドル/kgと大きな差がある。13

緊張関係 3:測定手法 vs. 実際の排出量

日本のウェルトゥゲート基準では、天然ガスの採掘・輸送中に発生するメタン漏洩が適格性評価に十分反映されない。TransitionZeroの分析では、石炭火力への20%アンモニア混焼は、通常のガス火力(CCGT)のほぼ2倍の排出量を依然として生じさせる。14 Breakthrough Instituteはメタン漏洩率によっては、アンモニア混焼が石炭単独燃焼を上回るケースもあり得ると指摘する。15 政府はGXキャップ&トレード制度の下での炭素価格上昇がインセンティブを是正すると反論するが、16 同制度が年間10万 t CO₂以上の排出事業者に義務化されるのは2026〜27年であり、炭素価格の軌跡はいまだ不確実だ。

発電方式別のCO₂排出強度(参考値)

注記(tCO₂-eq/MWh): アンモニア混焼は既存の火力設備からのCO₂排出を段階的に削減する手法として位置づけられ、特にガスタービンでは混焼率の上昇に応じて排出量が比例的に低下する傾向が示されている。IEAのブルーアンモニア排出係数に基づく参考値では、20%および50%混焼時の排出量はそれぞれ約390 kg、約245 kg/MWhとなるが、いずれもIEAが示す2030年ネットゼロ基準(約100 kg CO₂-eq/MWh)を上回る。一方、石炭火力でも一定の削減効果は確認されており、TransitionZeroは20%混焼でもガス火力(CCGT)の約2倍、ネットゼロ基準の約5倍の排出が残ると指摘する。BNEFは50%混焼で石炭単独比約40%の削減が可能とするが、50%未満の混焼率では無対策ガス火力より排出が高い。総じて、アンモニア混焼は現時点でネットゼロ解ではないものの、混焼率の向上や上流側の脱炭素化(メタン漏洩対策やCCS性能向上)により、段階的な排出削減を実現し得る技術として位置づけられる。出典:TransitionZero、IEA、Breakthrough Institute

強気の見方

Wood Mackenzieは、日本のCfDと米国45Qタックスクレジットを組み合わせることで、JERA・三井のブルーポイント案件は大規模低炭素アンモニア供給のリスクを低減する真にコスト効率の高い経路を示すと評価している。9 JERAは2024年に碧南火力発電所で世界初の商業規模20%アンモニア混焼実証に成功し、2029〜30年度の本格商業運転を目指している。8

2026年に注目すべき4つのポイント

- 第1ラウンド残余認定:METIは2026年春〜夏にかけて追加案件を認定し、第1ラウンドを締め括る見通し。中東・インド発のプロジェクト(IHI関与のACMEグリーン水素案件など)が候補に挙がっている。10 残余認定でグリーン/ブルー比率がどう変化するかに注目が集まる。

- GXキャップ&トレード本格化:年間10万 t CO₂以上の排出事業者への義務適用が2026〜27年に始まる。16 炭素価格の軌跡が、追加の公的資金なしにCfD補助ギャップがどれだけ早く縮小するかを左右する。

- 第2ラウンドの判断:第2ラウンドを実施するかどうかの政府判断が、第1ラウンドへの評価を示す指標となる。現時点でタイムラインは未確定。10

- IRA不確実性の波及:日本企業は米国の水素プロジェクトをCfDと45Qクレジットの組み合わせで組み立てていた。米国の再生可能エネルギー政策が後退すれば、日本の投資資本が中東・豪州・国内生産へとシフトし、認定サプライチェーンの地理的構成が変わる可能性がある。10

日本の3兆円規模の水素CfDは、まず大規模なサプライチェーン基盤の構築を優先するという、意図的で堅実な産業政策として位置づけられる。制度は特定の技術を優遇せず、最も費用対効果の高い選択肢が選ばれるように設計されている。今後の焦点は、この仕組みが気候目標と整合し続けられるかどうかであり、その鍵となるのはブルーアンモニアのサプライチェーン上流におけるメタン排出の厳格な監視だ。今後18か月の追加採択、GXカーボンプライスの動向、排出会計基準の強化が、3兆円が日本の水素転換の基盤として機能するのか、それとも化石燃料延命の高コストな橋渡しに傾くのかが方向づけられていく可能性がある。

(References)

- The Act on Promotion of Supply and Utilization of Low-Carbon Hydrogen and its Derivatives (“Hydrogen Society Promotion Act”) was enacted by the Japanese Diet in May 2024 and came into force October 2024. It established the legal framework for the CfD subsidy scheme and the Clusters Support Scheme. See: White & Case LLP, “Japan enacts its first legislation on hydrogen and CCS,” July 2024.

- Norton Rose Fulbright, “Understanding hydrogen in Japan,” updated March 2026. Total CfD budget stated as JPY 3 trillion (c. US$19 billion) over 15 years. JOGMEC administers subsidy payments.

- Carbon intensity threshold of 3.4 kg CO₂/kg H₂ (well-to-gate) for hydrogen; 0.84 kg CO₂/kg NH₃ (gate-to-gate) for ammonia. Source: METI Basic Policy, October 2024; Green Hydrogen Organisation, “Japan,” 2025.

- The 70% GHG reduction requirement is consistent with EU low-carbon hydrogen standards, but Japan’s well-to-gate (production point) measurement differs from Europe’s well-to-stack (consumption point) approach. Norton Rose Fulbright, op. cit. [fn2]. Jones Day, “Hydrogen Supply and Utilization Promotion Bill,” May 2024.

- The distinction between well-to-gate and well-to-stack/consumption measurements is central to lifecycle emissions debates for blue hydrogen. Methane leakage during upstream extraction and LNG transport is not captured under Japan’s standard. See: MDPI Hydrogen, “Hydrogen and Japan’s Energy Transition,” Vol. 6(3), August 2025.

- Hydrogen Society Promotion Act stipulates a 15-year CfD support period followed by a mandatory 10-year continued supply obligation. Source: OECD, “Case study — Japanese government subsidy scheme,” 2024.

- S&P Global Commodity Insights, “Japan certifies JERA-, Mitsui-led ammonia projects under Yen 3 trillion price-gap subsidy,” December 19, 2025. First two domestic projects were certified September 30, 2025 per METI announcement.

- JERA’s Hekinan coal-fired power station (Unit 4, 1 GW) conducted the world’s first 20% ammonia co-firing demonstration in commercial scale in 2024. Commercial operation at 20% co-firing is targeted for fiscal year 2029–30. JERA holds 35% equity in Blue Point; Mitsui holds 25%; CF Industries 40%. Source: S&P Global [fn7]; Wood Mackenzie [fn9].

- Wood Mackenzie, “Japan hydrogen CfD 2025,” press release, January 15, 2026. Estimates ~65% of CfD funding pool remaining after Round 1 JERA/Mitsui awards. Combined Round 1 blue ammonia volume: ~772,000 t/yr (equivalent to ~120,000 t H₂/yr).

- Energy Intelligence, “Japan’s Hydrogen Push Starts to Gain Momentum,” January 15, 2026. 27 proposals submitted to Round 1, collectively exceeding budget. Awards delayed approximately nine months post-March 2025 deadline. Middle East and India projects cited as candidates for further awards.

- Green Hydrogen Organisation / GH2, “Accelerating the Truly Low-Carbon Hydrogen Transition in Japan,” March 2025. Cites ENEOS assessment that ¥3 trillion would barely cover ~0.5% of required investment to sufficiently incentivize low-carbon hydrogen production at Japan’s target scale.

- Trencher, G. et al., “Acknowledging while doubling down: Japan’s responses to uncertainty in the hydrogen sector,” Technological Forecasting and Social Change, March 2026. Japan’s annual CfD support is approximately 8× the UK’s, 6× France’s, and 5× Australia’s equivalent hydrogen support instruments. Public hydrogen support increased from avg. ¥46bn/yr (2010–2019) to ¥184bn/yr for 2020–2040 projects.

- Green hydrogen production costs in Japan estimated at $3.0–$10.3/kg H₂ (PEM/alkaline electrolysis, 2023–2025), highly dependent on electricity price and scale. Blue hydrogen via SMR + CCS estimated at $1.2–$2.3/kg H₂. Source: MDPI Hydrogen [fn5].

- TransitionZero analysis cited in: Energy Tracker Asia, “The Environmental and Climate Impacts of False Solutions on Japan,” April 2024. Finds that Japan’s 20% ammonia co-firing goal at domestic coal power plants by 2030 will still generate nearly double the emissions of standard gas-fired power plants.

- Breakthrough Institute analysis cited in: IEEFA, “Japan’s bet on hydrogen is still unwavering despite decades of lackluster progress.” Notes ammonia co-firing may result in more emissions than burning coal or gas depending on upstream methane leakage assumptions.

- Japan’s GX (Green Transformation) cap-and-trade system, launched as the voluntary GX League (747 entities as of March 2024), becomes mandatory for entities emitting above 100,000 t CO₂/yr in 2026–27. Source: GH2 [fn11]; Trencher et al. [fn12].