Hydrogen is most efficient when produced and consumed in the same place — but that is rarely how the world works. Without affordable, safe, large-scale storage, hydrogen cannot realistically become the backbone of a decarbonized economy. Storage is the bottleneck of the hydrogen economy. Japan’s industrial players — from Tokuyama and Shimizu Construction to Kawasaki Heavy Industries, Chiyoda Corporation, and Iwatani — are each drawing on distinct core competencies to address the storage challenge. The outcome will shape whether Japan’s ¥150 trillion (about USD 1 trillion) hydrogen ambition becomes reality or remains a policy aspiration.

Market Landscape

Hydrogen has been called the fuel of the future for decades — but that future keeps shifting. The global hydrogen energy storage market was valued at approximately $17.6 billion in 2024 and is forecast to nearly double to $34.6 billion by 2034,FN1 yet the technology that sits at the heart of any viable supply chain remains stubbornly expensive and difficult to deploy at scale. The culprit is storage. Building a hydrogen supply chain requires four interlocking capabilities — production, storage, transport, and utilization — and of these, storage is where the economics fall apart most visibly. While localized production and consumption (the “local-for-local” model) is the most energy-efficient approach, it is rarely feasible: green hydrogen is cheapest where renewable energy is abundant, which is typically far from where industrial consumers are located.FN2

Storage Is the Backbone of the Hydrogen Economy

Japan sits at the epicenter of this challenge. The country was the first in the world to publish a national hydrogen strategy back in 2017, and its 2023 revised Basic Hydrogen Strategy now envisions ¥150 trillion in combined public-private investment over the next decade, with a goal of procuring 12 million tons of hydrogen annually by 2040.FN3 Yet geography makes domestic green hydrogen production prohibitively costly: BloombergNEF estimates Japan’s levelized cost of green hydrogen at two to more than three times that of China,FN4 owing to limited land and higher renewable energy prices. The inescapable implication is that Japan must import the bulk of its future hydrogen — and that means the storage and transport challenge is not a domestic engineering problem. It is a geopolitical and logistical one spanning oceans.

Industry Players

Japan’s hydrogen storage landscape involves a far broader cast of companies than is commonly reported, each drawing on distinct industrial competencies. The table below maps the full ecosystem — from solid-state material developers and cryogenic infrastructure builders to chemical carrier innovators and composite vessel manufacturers. Two broad technology camps are emerging: the liquefied hydrogen (LH₂) camp, led by Kawasaki Heavy Industries and Iwatani, which bets on cryogenic storage at −253°C as the optimal format for large-scale ocean transport; and the organic chemical carrier (LOHC/MCH) camp, championed by Chiyoda Corporation and ENEOS, which converts hydrogen into methylcyclohexane (MCH) — a liquid storable at ambient temperature in standard oil tankers and existing petroleum infrastructure, at roughly 530 times the energy density of gaseous hydrogen.5 Both paths have cleared initial proof-of-concept; neither has yet achieved the cost levels required for commercial viability without subsidy.

Japan Hydrogen Storage — Company Landscape

| Company | Storage Technology | Key Features & Status |

|---|---|---|

| Tokuyama (4043) | Solid-State / Metal Hydride Magnesium hydride (MgH₂) | Mass production launched April 2024 (target: 30 t/yr). H₂ released by adding water — no heating needed. Hokkaido utility heating pilot underway. Cost target: tens-of-thousands of yen/unit → thousands of yen at scale.FN5 |

| Mitsui Mining & Smelting (5706) | Solid-State / Metal Hydride Hydrogen-absorbing alloy (AB5 / AB2 type) | 30+ years supplying Ni-MH battery alloys. Near-ambient pressure/temperature operation; exempt from High Pressure Gas Safety Act. Multiple grades available. Suited to stationary and urban-distributed storage. |

| Kawasaki Heavy Industries (7012) | Cryogenic Liquid H₂ Large-scale LH₂ tank + carrier ship + H₂ co-firing engine | World’s largest 50,000 m³ LH₂ tank in fabrication (Aug 2025). Kawasaki LH₂ Terminal, Ogishima: groundbreaking Nov 2025, operations from 2030. First commercial H₂ 30%-co-firing gas engine on sale Sept 2025.FN6, FN7, FN8 |

| Iwatani Corporation (8088) | Cryogenic Liquid H₂ LH₂ production, storage & supply infrastructure | ~100% domestic LH₂ market share; handling hydrogen since 1941. Partner in NEDO’s LH₂ supply chain demo. Co-founder of HySTRA for the Japan–Australia LH₂ corridor. |

| ENEOS Holdings (5020) | Cryogenic Liquid H₂ LH₂ + MCH (dual approach) | In NEDO LH₂ demo consortium with Kawasaki and Iwatani. Also pursuing MCH route to leverage existing refinery tanks and tankers. Projects active in Australia, Southeast Asia, and Middle East. |

| Chiyoda Corporation (6366) | Organic Carrier — LOHC MCH (SPERA H₂™) | Developed MCH dehydrogenation catalyst from 2002. Completed world’s first international H₂ supply chain demo (Brunei → Kawasaki) in 2020. MCH is ~530× denser than gaseous H₂ and ships in standard oil tankers. Co-developing electrolysis systems with Toyota.FN13 |

| Teijin (3401) | Composite Pressure Vessel Carbon-fibre composite vessel (“Ultrexa”) | Japan’s first CFRP pressure vessel (since 1987); 400,000+ units shipped. Covers H₂ trailers, FCV tanks, and drone cylinders — ⅓ the weight of steel, rated to 45 MPa+. Partnered with Denyo on 3 kVA H₂ fuel-cell generator (Feb 2025).FN14 |

| Shimizu Construction (1803) | Building-Integrated “Hydro Cubic” — building-embedded LH₂ | Modular LH₂ storage built into building infrastructure (e.g., underground at Akasaka, Tokyo). Brings storage to existing demand nodes. Key bottleneck: securing offtaker commitments to justify scale-up.FN5 |

Notes: All tickers refer to companies listed on the Tokyo Stock Exchange (TSE) Prime Market, with codes verified as of March 2026. Technology classifications reflect each firm’s primary storage mechanism; ENEOS appears under the LH₂ category because its NEDO‑funded commercialisation project is LH₂‑based despite also pursuing MCH/LOHC, while Teijin is included as an enabling component supplier rather than a storage‑medium provider. Sources include company IR disclosures, press releases, and official websites accessed between February and March 2026, as well as Tokuyama Corporation’s April 3, 2024 announcement; Kawasaki Heavy Industries releases from August 7, September 30, and November 27, 2025; Chiyoda Corporation’s SPERA Hydrogen project documentation and its February 2024 joint development announcement with Toyota; Teijin’s February 17, 2025 release; Mitsui Mining & Smelting’s functional powder product materials; Iwatani Corporation’s hydrogen business disclosures and HySTRA consortium publications; and ENEOS Holdings’ hydrogen strategy documentation. This table is provided for informational purposes only and does not constitute investment advice; market positions and development stages reflect publicly available information at the time of publication and may change.

Company Landscape and Case Studies

Kawasaki Heavy Industries has mounted perhaps the most vertically integrated push of any single company: fabricating a 50,000 m³ LH₂ storage tank at its Harima Works,FN6 breaking ground on the Kawasaki LH₂ Terminal in November 2025,FN7 and launching commercial sales of a 30%-hydrogen-blend co-firing engine in September 2025.FN8 Chiyoda’s SPERA system takes the opposite infrastructure approach — converting hydrogen into ambient-temperature MCH that ships in standard oil tankers. Having completed the world’s first international hydrogen supply chain demonstration (Brunei → Kawasaki) in 2020, Chiyoda is now co-developing large-scale electrolysis with Toyota for rollout from 2025.FN13

The Core Challenges

The obstacles are structurally similar across all players. Cost parity remains the primary hurdle: Japan’s government targets ¥30/Nm³ by 2030 and ¥20/Nm³ by 2050,FN9 yet independent analysis suggests domestically produced green hydrogen in 2030 will land roughly 1.6 times that target even under optimistic assumptions.FN10 The second obstacle is the classic chicken-and-egg dynamic: storage cannot be cheapened without scale, but scale requires demand that does not yet exist. Tokuyama’s Hokkaido heating pilot,FN5 Shimizu’s Akasaka building installation,FN5 and Teijin’s portable hydrogen fuel-cell generatorFN14 are deliberate attempts to seed that demand. The third challenge is project execution: the Hydrogen Council estimates only around 9% of announced global hydrogen projects have reached final investment decision.FN11

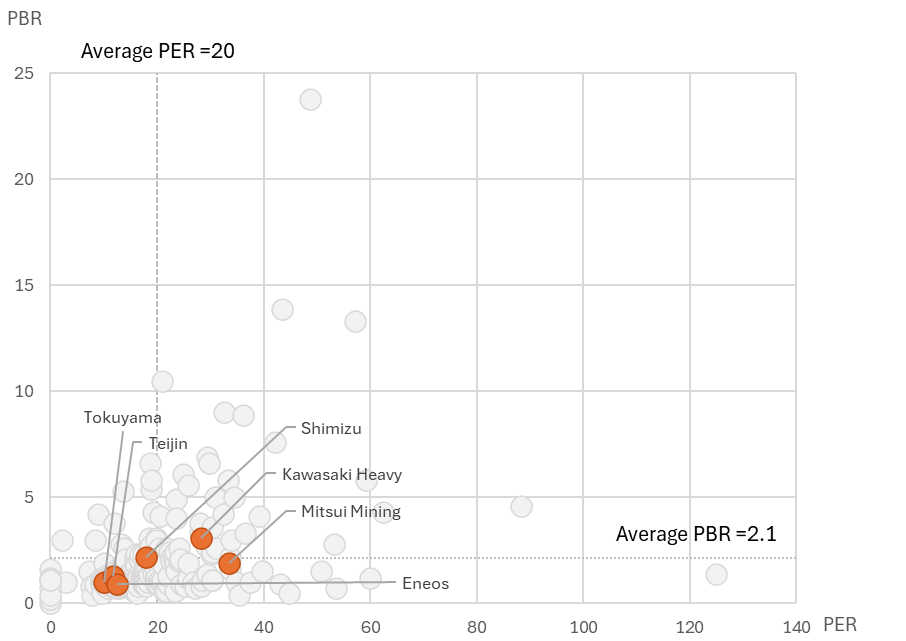

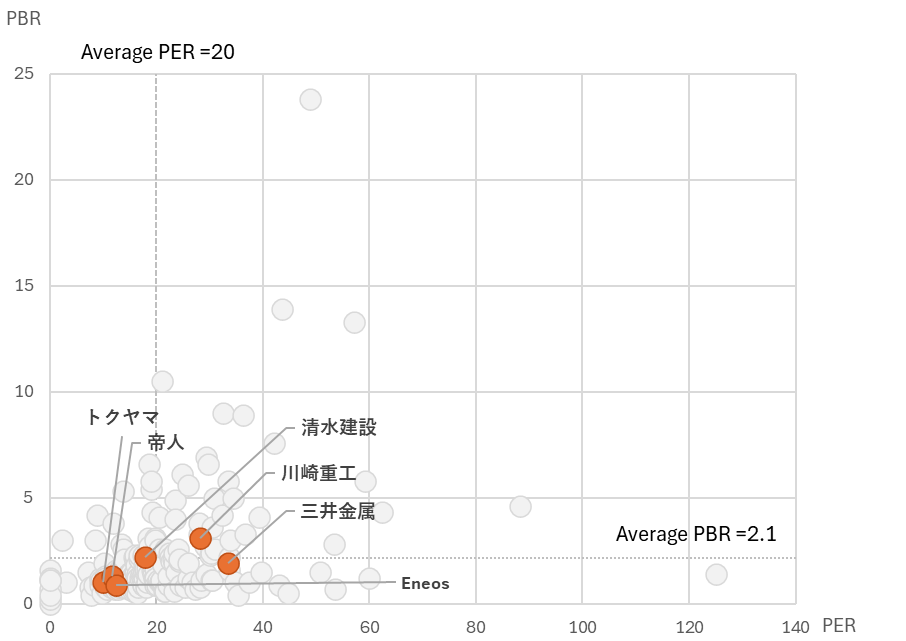

PER / PBR Positioning of Hydrogen Storage Stocks — Nikkei 225 Constituents

Notes: This analysis covers only Nikkei 225 constituents and therefore excludes Iwatani Corporation (8088) and Chiyoda Corporation (6366), which are not part of the index. The scatter‑plot reference lines—PER 20× and PBR 2.1×—reflect Nikkei 225 index averages. PER and PBR figures are based on closing prices as of March 27, 2026, sourced from the March 28, 2026 edition of the Nikkei Shimbun.

The valuation spread is striking. Kawasaki Heavy trades at 3.1× book — a level that implies the market has already awarded significant value to its liquefied hydrogen infrastructure ambitions well before the Kawasaki LH₂ Terminal opens in 2030; this is a bet, not a reward for delivered results. ENEOS, by contrast, sits below book value (0.9× PBR), reflecting skepticism toward refinery‑era incumbents pivoting to hydrogen despite its pragmatic MCH/LOHC approach. Tokuyama and Teijin, both at 1.0–1.3× PBR, show that their hydrogen businesses are real but still too small to reprice the stock, offering only a free option if magnesium hydride or composite‑vessel markets scale. The key takeaway is that the market is not treating “hydrogen storage” as a monolithic theme: risk premiums vary sharply by proximity to investable cash flows, with Kawasaki the only name where hydrogen is already a primary valuation driver.

Strategic Outlook

Japan’s hydrogen storage ecosystem amounts to a national portfolio hedge against technological uncertainty. With no single format winning across all scales and use cases, companies spanning materials science, heavy engineering, chemicals, construction, and energy distribution are advancing solutions in parallel. Kawasaki’s co-firing engine strategy is instructive: it creates hydrogen demand now, within existing infrastructure, buying time for the supply chain to mature. The country faces structural headwinds — green hydrogen costs two to three times higher than China’s, a potential swap of one import dependency for another, and an absence of clear government guidance on how 12 million tons of annual hydrogen will be allocated by 2040.FN3, FN12 But the infrastructure being built today — tanks, terminals, MCH carriers, metal hydride materials, and composite vessels — is tangible. Whether it arrives on time and on cost will determine Japan’s energy trajectory for decades to come.

Disclaimer — This article is provided for informational purposes only and does not constitute investment advice.

Japanese translations

Title: 水素を「貯める」技術の最前線

水素エネルギーの効率は、地産地消されたときに最大化される。だが現実は、それを許さないことの方が多い。手頃で安全な大規模貯蔵なくして、水素は脱炭素経済の基盤にはなれない。水素経済における中心は「貯蔵」にある。川崎重工・千代田化工建設・岩谷産業をはじめとする日本の産業プレーヤーは、それぞれの中核技術を活かして貯蔵課題に取り組んでいる。その成否が、日本の150兆円規模の水素構想を現実にするか、政策目標にとどめるかを左右する。

水素はかねてより「未来の燃料」と呼ばれてきたが、その未来は常に先送りされてきた。世界の水素エネルギー貯蔵市場は2024年に約176億ドル規模に達し、2034年には346億ドルへと倍増すると予測されている。1 しかし、実行可能なサプライチェーンの中核をなす技術は、依然としてコストが高く、大規模展開が難しいままだ。その主因が「貯蔵」である。水素サプライチェーンの構築には、製造・貯蔵・輸送・利活用という四つの要素が必要だが、このうち経済性が最も崩れやすいのが貯蔵の工程だ。地産地消モデル(製造と消費が近接している場合)は最もエネルギー効率が高いが、現実には実現しにくい。グリーン水素は再生可能エネルギーが豊富な地域ほど安く製造できるが、そうした地域は工業消費地から遠く離れていることが多い。2

市場の現状

日本はこの課題の震源地に位置する。2017年に世界初の国家水素戦略を策定した日本は、2023年改訂の「水素基本戦略」において今後10年間で官民合計150兆円の投資と2040年までの年間1,200万トン調達を目標に掲げた。3 しかし地理的条件が国内でのグリーン水素製造を困難にしている。BloombergNEFによれば、日本のグリーン水素レベライズドコストは中国の2〜3倍以上に達する。4 これが意味するのは、日本は将来の水素の大部分を輸入に頼らざるを得ないということ——すなわち、貯蔵・輸送の課題は国内の工学的問題ではなく、海を越えた地政学的・物流的問題だということだ。

企業動向

日本の水素貯蔵エコシステムには、一般に報告される以上に多くのプレーヤーが参入しており、それぞれ異なる産業基盤から課題にアプローチしている。下表はその全体像を示す——固体材料開発から極低温インフラ整備、化学的水素キャリア、複合材圧力容器まで多岐にわたる。大きく二つの技術陣営が形成されている。川崎重工・岩谷産業が主導する液化水素(LH₂)陣営は、−253℃での極低温貯蔵を大規模海上輸送の最適フォーマットと位置づける。一方、千代田化工建設・ENEOSが推進する有機水素キャリア(LOHC/MCH)陣営は、水素をメチルシクロヘキサン(MCH)という常温常圧の液体に変換し、既存の石油タンカーや石油インフラで貯蔵・輸送する。MCHは気体水素に比べ体積エネルギー密度が約530倍に達する。5 いずれの路線も初期実証を終えているが、補助金なしで商業的に成立するコスト水準にはまだ到達していない。

企業一覧

| 企業 | 貯蔵技術 | 特徴・開発状況 |

|---|---|---|

| トクヤマ (4043) | 固体・金属 水素化物水素化マグネシウム(MgH₂) | 2024年4月に量産開始(目標:年産30トン)。水を加えるだけで水素を放出——加熱不要。北海道の企業との暖房用途パイロット実施中。コスト目標:数万円/ユニット→数千円/ユニット(量産時)。5 |

| 三井金属鉱業 (5706) | 固体・金属 水素化物水素吸蔵合金(AB5 / AB2型) | ニッケル水素電池向けに30年超の供給実績。常温常圧に近い低圧運用が可能で、高圧ガス保安法の対象外。複数グレードを揃え、定置型・分散型都市ストレージに適合。 |

| 川崎重工業 (7012) | 液化水素(LH₂) 大型LH₂タンク+運搬船+H₂混焼エンジン | 世界最大の5万m³ LH₂タンクを製作中(2025年8月着手)。川崎LH₂ターミナル(扇島)起工式:2025年11月、2030年稼働予定。世界初のH₂30%混焼大型ガスエンジンを2025年9月に商用販売開始。6,7,8 |

| 岩谷産業 (8088) | 液化水素(LH₂) LH₂製造・貯蔵・供給インフラ | 国内LH₂市場シェア約100%、水素取扱い開始は1941年。NEDOグリーンイノベーション基金のLH₂サプライチェーン商用化実証に参画。日豪LH₂回廊を目指すHySTRA設立メンバー。 |

| ENEOSホールディングス (5020) | 液化水素(LH₂) LH₂ + MCH(二軸アプローチ) | 川崎重工・岩谷とともにNEDO LH₂実証コンソーシアムに参加。既存製油所タンク・タンカーを活用するMCH路線も並行推進。豪州・東南アジア・中東でプロジェクト展開中。 |

| 千代田化工建設 (6366) | 有機水素キャリア — LOHC MCH(SPERA H₂™) | 2002年からMCH脱水素触媒を開発。2020年に世界初の国際水素サプライチェーン実証(ブルネイ→川崎)を完了。MCHは気体H₂の約530倍のエネルギー密度。常温常圧で既存石油タンカーに搭載可能。トヨタと大規模水電解システムを共同開発中。13 |

| 帝人 (3401) | 複合材圧力容器 炭素繊維複合材容器 (「ウルトレッサ」) | 日本初のCFRP複合材圧力容器(1987年〜)、国内累計出荷40万本超。水素トレーラー・FCV車載タンク・ドローン用シリンダーに展開。スチール製の1/3の重量、45MPa以上の耐圧。デンヨーと3kVA級H₂燃料電池発電装置を共同開発(2025年2月)。14 |

| 清水建設 (1803) | 建物組込み型 「ハイドロ・キュービック」— 建物埋込みLH₂ | 建物インフラに組み込むモジュール型LH₂貯蔵(例:赤坂ビル地下)。既存の需要地点に貯蔵を近接させ、新規インフラ回廊を不要にする。最大のボトルネック:スケールアップを正当化するオフテイカー(需要家)の確保。5 |

注記・出典 ティッカー — 掲載企業はすべて東京証券取引所(TSE)上場。ティッカーコードは2026年3月時点で確認済み(千代田化工建設はTSEスタンダード市場)。技術分類 — 各社の主要な貯蔵メカニズムを基準に分類。ENEOSはMCH/LOHCも推進しているが、NEDO助成の商用化実証がLH₂ベースのため液化水素カテゴリーに掲載。帝人は貯蔵媒体ではなく圧力容器(ハードウェア)の供給者として、貯蔵バリューチェーンの構成要素として掲載。出典 — 各社IRディスクロージャー・プレスリリース・公式ウェブサイト(2026年2〜3月閲覧)。トクヤマ2024年4月3日リリース5、川崎重工2025年8月7日・9月30日・11月27日リリース6,7,8、千代田化工建設SPERAプロジェクト資料・トヨタとの2024年2月共同開発発表13、帝人2025年2月17日リリース14、三井金属機能性粉体事業部製品資料、岩谷産業水素事業資料・HySTRAコンソーシアム資料、ENEOSホールディングス水素戦略資料。免責 — 本表は情報提供を目的としており、投資助言を構成するものではありません。

企業別分析

川崎重工業は、単一企業としておそらく世界最も垂直統合度の高い水素展開を進めている。播磨工場で5万m³ LH₂タンクの製作を開始し、6 2025年11月に川崎LH₂ターミナルの起工式を行い、7 同年9月には水素30%混焼エンジンの商用販売を開始した。8 千代田化工建設のSPERAシステムは、インフラ面で対照的なアプローチを取る——水素を常温のMCHに変換し、既存の石油タンカーで輸送する。2020年に世界初の国際水素サプライチェーン実証(ブルネイ→川崎)を完了した千代田は、現在トヨタと大規模水電解システムを共同開発し、2025年度からの展開を目指している。13

課題の構造

各社が直面する障壁の構造は、技術が異なっていても本質的に共通している。最大のハードルはコストパリティだ。日本政府はNm³当たり30円(2030年目標)、20円(2050年目標)という供給コスト目標を掲げているが、9 独立した分析によれば、楽観的な前提のもとでも2030年の国産グリーン水素コストはこの目標の約1.6倍になると見込まれる。10 第二の障壁は古典的な「鶏と卵」問題だ。スケールなくしてコスト削減はなく、コスト競争力なくして需要は生まれない。トクヤマの北海道暖房パイロット、5 清水建設の赤坂ビル実装、5 そして帝人の可搬式水素燃料電池発電機14 は、この連鎖を断ち切る「最初の需要」を生み出す試みだ。第三の課題はプロジェクト実行力——水素評議会(Hydrogen Council)によれば、世界で発表されたH₂プロジェクトのうち最終投資決定(FID)に至ったのは約9%に過ぎない。11

バリュエーション分析

注記・出典 分析対象 — 日経225構成銘柄のみを対象。岩谷産業(8088・TSEプライム)および千代田化工建設(6366・TSEスタンダード)は水素貯蔵における重要プレーヤーだが、日経225非採用のため本バリュエーション表から除外。両社の戦略は上記企業一覧に記載。参照ライン — 散布図の参照ラインはPER 20倍・PBR 2.1倍(いずれも日経225の平均値)。出典 — PER・PBR・配当利回り・時価総額は、2026年3月28日付『日本経済新聞』掲載値(2026年3月27日終値ベース)を参照。本表は情報提供目的であり、投資助言を構成するものではありません。散布図——「日経225構成銘柄における水素貯蔵関連株のPER/PBRポジショニング」——は、6社を日経225の平均PER(20倍)および平均PBR(2.1倍)と対比させ、三つの異なる投資家クラスターを浮かび上がらせる。分析対象は日経225構成銘柄に限定されるため、水素貯蔵の重要プレーヤーである岩谷産業(8088)と千代田化工建設(6366)は同指数の構成銘柄でないことから除外されている。

バリュエーションの格差は示唆に富む。川崎重工はPBR 3.1倍で取引されており、川崎LH₂ターミナルが2030年に稼働する前から、市場が液化水素インフラの将来価値をすでに相当程度織り込んでいることを示す——これは実績への報酬ではなく、未来への賭けとも捉えられる。一方のENEOSはPBR 0.9倍と1倍割れで、現実的なMCH/LOHCアプローチにもかかわらず、石油元売り企業が水素にピボットすることへの市場の懐疑を映している。トクヤマと帝人はいずれもPBR 1.0〜1.3倍と簿価近辺で推移しており、水素事業が「本物だが株価を動かすにはまだ小さい」という段階を示す——MgH₂や複合材容器の市場が拡大すれば、忍耐強い投資家にとって「タダのオプション」になり得る。重要な示唆は、市場が「水素貯蔵」を一括のテーマとして評価していないという点だ。投資可能なキャッシュフローへの距離に応じてリスクプレミアムは大きく異なり、現時点で水素を主たるバリュエーションドライバーとして評価されているのは川崎重工のみだ。

戦略的展望

日本の水素貯蔵エコシステムは、技術的不確実性に対する国家レベルのポートフォリオ・ヘッジとして機能している。あらゆる規模・用途で勝者となる単一フォーマットが存在していない以上、素材科学・重工業・化学・建設・エネルギー流通にまたがる各社が並行してソリューションを開発する戦略は合理的だ。川崎重工の混焼エンジン戦略は示唆に富んでいる——既存インフラを使って今すぐ水素需要を創出し、サプライチェーン整備の時間を稼ぐという発想だ。日本は構造的な問題を抱えている——中国比2〜3倍の高いグリーン水素コスト、化石燃料輸入依存の別形態への転換リスク、そして1,200万トンの年間目標をどのセクターにどう配分するかを示す政府指針の欠如。3,12

しかし、今まさに建設・開発が進む水素貯蔵タンク・水素ターミナル・MCHキャリア・金属水素化物材料・複合材容器は紛れもなく現実のものだ。それらが予定通りのコストと時間軸で実現するかどうかが、今後数十年の日本のエネルギーの行方を決める。

免責 — 本記事は情報提供を目的としており、投資助言を構成するものではありません。

References

FN1 — Precedence Research, Hydrogen Energy Storage Market Size and Forecast to 2034, July 2025. Market valued at $17.59B in 2024; projected at $34.56B by 2034 at CAGR of 7.01%.

FN2 — IEA, Global Hydrogen Review 2024. Global hydrogen demand reached 97 Mt in 2023, with low‑emission hydrogen accounting for less than 1% of total production.

FN3 — World Economic Forum / Green Hydrogen Organisation, Japan’s Hydrogen Strategy, 2025. Japan targets 12 million tons per annum by 2040; ¥150 trillion combined investment target over ten years per the revised 2023 Basic Hydrogen Strategy.

FN4 — IEEFA, Japan’s bet on hydrogen is still unwavering despite decades of lackluster progress. Citing BloombergNEF levelized cost data showing Japan at 2–3× China’s green hydrogen production cost.

FN5 — Company disclosures and presentation materials: Tokuyama Corporation, Shimizu Construction. Cost figures and Hokkaido pilot details from source materials provided.

FN6 — Kawasaki Heavy Industries press release, August 7, 2025: “Fabrication of Large Liquefied Hydrogen Storage Tank Launched.” Tank capacity: 50,000 m³; fabrication site: Harima Works, Hyogo Prefecture.

FN7 — Kawasaki Heavy Industries / Japan Suiso Energy press release, November 27, 2025: Groundbreaking ceremony for Kawasaki LH₂ Terminal, Ogishima, Kawasaki City. Operations planned from 2030.

FN8 — Kawasaki Heavy Industries press release, September 30, 2025: “World’s First Commercial Launch of Hydrogen 30% Co‑Firing Large Gas Engine System.” Verification testing ran October 2024 – September 2025.

FN9 — HyResource Japan, Japan Hydrogen Policy Overview, updated December 2025. Government supply cost targets: ¥30/Nm³ (CIF) by 2030; ¥20/Nm³ by 2050.

FN10 — Renewable Energy Institute, Re‑examining Japan’s Hydrogen Strategy. Based on electrolyzer cost targets for 2030 (¥52,000/kW alkaline) and solar PV procurement price projections, estimated domestic green hydrogen cost in 2030 is approximately ¥48.4/Nm³ — roughly 1.6× the government’s ¥30 target.

FN11 — Hydrogen Council, Hydrogen Insights 2024. More than 1,000 hydrogen projects announced globally; approximately 9% have reached final investment decision.

FN12 — World Economic Forum, “Japan’s hydrogen gamble: Learning from Japan’s energy bet”, April 2025. Analysis of Japan’s structural import dependency risk and strategic planning gaps.

FN13 — Chiyoda Corporation, SPERA Hydrogen System (accessed March 2026). MCH technology development began 2002; commercial‑grade dehydrogenation catalyst confirmed after 10,000+ hours of testing. World’s first international H₂ supply chain demonstration (Brunei–Kawasaki) completed December 2020. Chiyoda–Toyota joint electrolysis development announced February 2024; pilot deployment at Toyota Honsha plant planned from FY2025.

FN14 — Teijin / Teijin Engineering press release, February 17, 2025: Joint development of 3 kVA hydrogen fuel‑cell generator with Denyo Corporation using “Ultrexa” large portable composite pressure vessel. Ultrexa series launched 1987; cumulative domestic shipments exceed 400,000 units; rated to 45 MPa; weight approximately one‑third of steel equivalents.