Sekisui Chemical’s commercial debut is a genuine inflection point — but Japan’s path from first-mover to market leader runs through durability gaps, cost hurdles, IP risk, and a China already manufacturing at gigawatt scale.

SOLAFIL Launch

On 27 March 2026, Sekisui Solar Film — unlisted, 86% Sekisui Chemical 4204 JP became the first Japanese manufacturer to sell perovskite solar cells commercially, launching its film-type product under the brand SOLAFIL.1 The strategic rationale is structural: Japan’s per-capita flat land available for solar is already the highest of any major economy, average wind speeds are materially lower than in Europe or North America, and conventional silicon panels cannot be installed on low-load-bearing rooftops, facades, wind turbine towers, or agricultural land.2 Perovskite — lightweight, thin, and flexible — unlocks all of those surfaces simultaneously. The government has codified the opportunity: the 7th Basic Energy Plan targets 20 GW of perovskite by 2040, equivalent to 20 nuclear reactors, backed by up to ¥157.25bn in METI GX subsidies already committed to Sekisui alone.3 Japan also holds a raw-material edge: iodine, the key perovskite input, is produced domestically at the world’s second-largest scale.

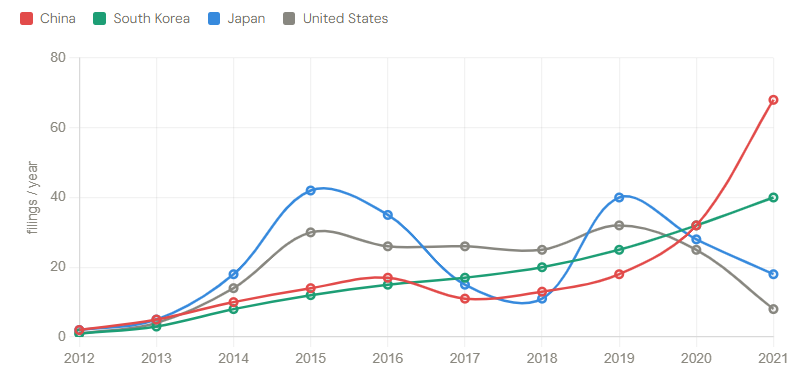

Perovskite-related international patent filings by country (filings / year)

Source: Clarivate Analytics Japan.4 “Related patents” = filed in 2+ countries; single-country filings excluded.

Technology Analysis

Japan’s technology lead is real but narrowing fast. Multiple domestic firms are advancing along distinct product vectors: Panasonic HD 6752 JP targeting glass-type BIPV trial sales in FY2026; Kaneka 4118 JP with a 32.5% tandem efficiency record and NEDO GX fund adoption for 2028 mass production; Enecoat Technologies — unlisted (Toyota/Woven Capital and INPEX-backed) achieving 30.4% tandem efficiency with Toyota and targeting a 2027 production line;5 and a broad materials ecosystem spanning AGC 5201 JP and Nippon Sheet Glass 5202 JP on glass substrates, Toray 3402 JP on encapsulants, Nissan Chemical 4021 JP on hole transport materials, Canon 7751 JP on coatings, and Fujifilm 4901 JP and Ricoh 7752 JP on specialty materials.6

Against this, China is already manufacturing at GW scale: GCL Optoelectronics 3800 HK opened a gigawatt factory in Kunshan in June 2025 at $700m, achieving 29.51% certified module efficiency; UtmoLight (private) launched a 1 GW line in February 2025 with a 25-year output warranty; and LONGi 601012 CH holds the NREL-certified world record at 34.85% tandem efficiency.7 Korea’s Hanwha Solutions 009830 KS has committed ~$1.6bn to perovskite tandem production.8 China brings lab results to market in under two years versus five in Japan — and Sekisui’s planned 100 MW plant costs ~$600m against GCL’s $700m for ten times the capacity. Three challenges must be addressed at speed: closing the manufacturing cost gap, extending outdoor durability from 10 years (current SOLAFIL rating) to the 25-year commercial standard, and protecting IP across the full supply chain to avoid repeating silicon solar’s history of technology leakage.9

The most important near-term fact is the commercialization gap. Sekisui Chemical is the only listed Japanese company currently generating perovskite revenue. Every other name remains in the investment or pre-revenue phase.

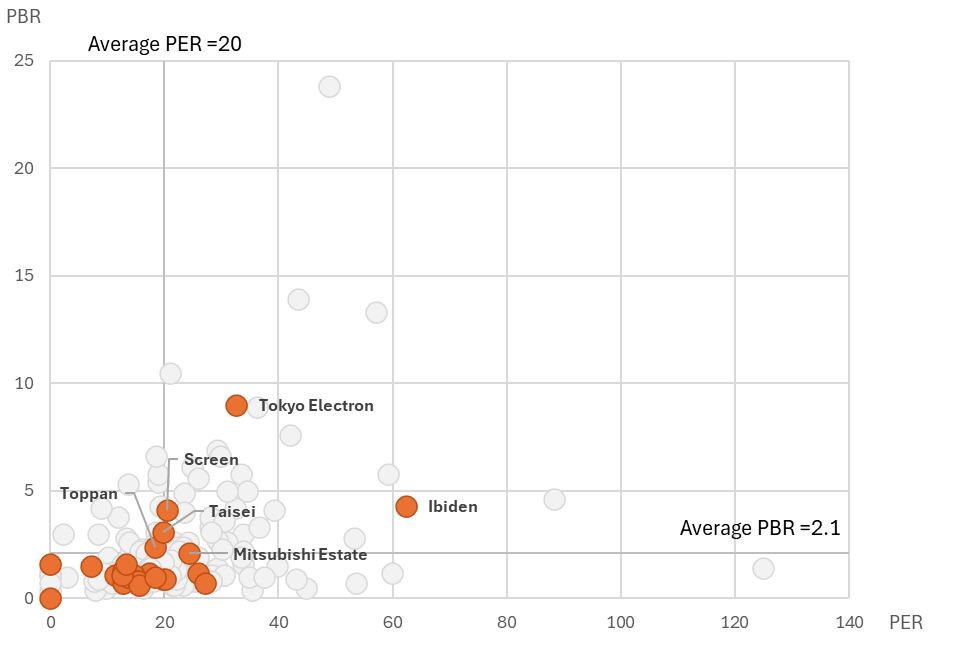

Valuation Analysis

PER / PBR Positioning of Perovskite Solar Stocks — Nikkei 225 Constituents

Notes: This analysis covers only Nikkei 225 constituents and therefore excludes Iwatani Corporation (8088) and Chiyoda Corporation (6366), which are not part of the index. The scatter‑plot reference lines—PER 20× and PBR 2.1×—reflect Nikkei 225 index averages. PER and PBR figures are based on closing prices as of March 27, 2026, sourced from the March 28, 2026 edition of the Nikkei Shimbun.

The PER/PBR scatter maps the commercialization gap directly onto market pricing. Tokyo Electron 8035 JP (PER ~35x, PBR ~9–10x) and Screen HD 7735 JP trade well above both market averages — but for reasons largely unrelated to perovskite. Tokyo Electron’s multiple reflects AI semiconductor equipment dominance; any perovskite optionality is incidental. Screen is the more interesting case: its elevated multiple is similarly rooted in semiconductor wafer cleaning (world #1 share), but its roll-to-roll direct-coating technology — originating in its printing heritage — is simultaneously in commercial production for green hydrogen catalyst-coated membranes (CCM), with Tokyo Gas beginning orders in December 2025 and a ¥10bn PEM electrolyser revenue target by 2030.11 The identical process IP applies directly to perovskite layer deposition, making Screen the clearest cross-theme infrastructure play in the universe — one where the same core capability underpins both the hydrogen and solar transitions. The bulk of the orange cluster, however, sits below and to the left of both averages: Toppan HD 7911 JP, Taisei Construction 1801 JP, Mitsubishi Estate 8802 JP, and the materials names trade at or below market multiples, implying perovskite exposure is priced at zero. This is rational given the timeline risk — but for investors who believe the 20 GW by 2040 target has a credible execution path, that cluster offers the asymmetric structure thematic investing rewards: current-earnings businesses carrying an unpriced call option on a national policy priority.12

| Cell manufacturers & developers | Functional materials & coatings |

| Sekisui Chemical / SSF4204 | Nissan Chemical 4021 |

| Panasonic HD6752 | Sumitomo Chemical 4005 |

| Kaneka 4118 | Mitsubishi Chemical G 4188 |

| Toshiba 6502 | Asahi Kasei 3407 |

| Aisin 7259 | Fujifilm HD 4901 |

| Ricoh 7752 | Canon 7751 |

| Glass substrates & encapsulants | Investment, deployment & real estate |

| AGC 5201 | Toyota Motor 7203 |

| Nippon Electric Glass 5214 | INPEX 1605 |

| Toray 3402 | Mitsubishi Estate 8802 |

| Nitto Denko 6988 | Dai-ichi Life HD 8750 |

| Toppan HD 7911 | Taisei Construction 1801 |

| Dai Nippon Printing 7912 | Sharp 6753 |

| Equipment & process technology | Tokyo Electric Power HD 9501 |

| Screen HD 7735 | Tokyo Gas 9531 |

| Tokyo Electron 8035 | DBJ (Dev. Bank of Japan) Unlisted |

| Kyocera 6971 |

Japan developed perovskite solar technology, and its future now depends less on invention than on how quickly it can build scale. Sekisui’s first commercial sales, the policy support in place, and the depth of Japan’s materials ecosystem all point to real potential, but China’s gigawatt factories and Korea’s large commitments have already set a faster global pace. Japan still has a credible path, yet the outcome will hinge on how steadily and how quickly it can move over the next few years.

Japanese translations

Title: 日本のペロブスカイト転換点:量産化への競争

2026年3月27日、Sekisui Solar Film(非上場、積水化学工業〈4204 JP〉が86%保有)は、日本企業として初めてペロブスカイト太陽電池の商業販売を開始し、フィルム型製品をSOLAFILのブランドで発売した。1

この戦略的背景は構造的なものだ。日本は主要国の中で、一人当たりの平地面積あたり太陽光発電の導入量がすでに最大であり、平均風速は欧米より低い。また、従来のシリコンパネルは、低荷重屋根、ビル外壁、風車タワー、農地などには設置できない。一方、ペロブスカイトは軽量・薄型・柔軟で、これらの面を同時に活用できる。

政府もこの機会を制度化している。第7次エネルギー基本計画では2040年までに20GWのペロブスカイト導入(原発20基相当)を掲げ、すでに積水化学向けに1,572.5億円のGX補助金がコミットされている。3 日本は原材料面でも優位性があり、主要原料であるヨウ素は世界第2位規模で国内生産されている。

ペロブスカイト関連の国際特許出願(件数/年)

出典:Clarivate Analytics Japan.4 「関連特許」=2カ国以上で出願されたもの(単一国出願は除外)。

Technology Analysis(技術分析)

日本の技術的リードは現実だが、その差は急速に縮小している。国内企業は複数の方向性で開発を進めている。

Panasonic HD(6752 JP)はガラスタイプBIPVの2026年度試験販売を目指し、Kaneka(4118 JP)は32.5%のタンデム効率を達成し、NEDO GX採択を受けて2028年量産を計画している。Enecoat Technologies(非上場、トヨタ/Woven CapitalおよびINPEX出資)はトヨタと共同で30.4%のタンデム効率を達成し、2027年の生産ライン構築を目指す。5

材料エコシステムも広い。AGC(5201 JP)と日本電気硝子(5214 JP)はガラス基板、Toray(3402 JP)は封止材、Nissan Chemical(4021 JP)はホール輸送材料、Canon(7751 JP)はコーティング、Fujifilm(4901 JP)とRicoh(7752 JP)は機能性材料を担当している。6

一方、中国はすでにGWスケールの量産に入っている。GCL Optoelectronics(3800 HK)は2025年6月に昆山で700百万ドル規模の1GW工場を稼働し、29.51%のモジュール効率を達成。UtmoLight(非上場)は2025年2月に1GWラインを立ち上げ、25年保証を付与。LONGi(601012 CH)は34.85%のNREL認証世界記録を保持している。7 韓国のHanwha Solutions(009830 KS)は約16億ドルをタンデム量産に投じている。8

中国は研究室から量産まで2年、日本は5年。さらに積水の100MW工場は約6億ドル規模だが、GCLは同額で10倍の1GWを建設している。

日本企業が直面している課題は以下の3点である。

- 製造コストギャップの解消

- 耐候性の延長(現状SOLAFILは10年、商用基準は25年)

- サプライチェーン全体の知財保護(シリコン太陽電池の技術流出の再現を避ける)9

最も重要な近接事実は商業化ギャップである。現時点でペロブスカイト売上を計上している上場企業は積水化学のみで、他はすべて投資段階またはプレ収益段階にある。

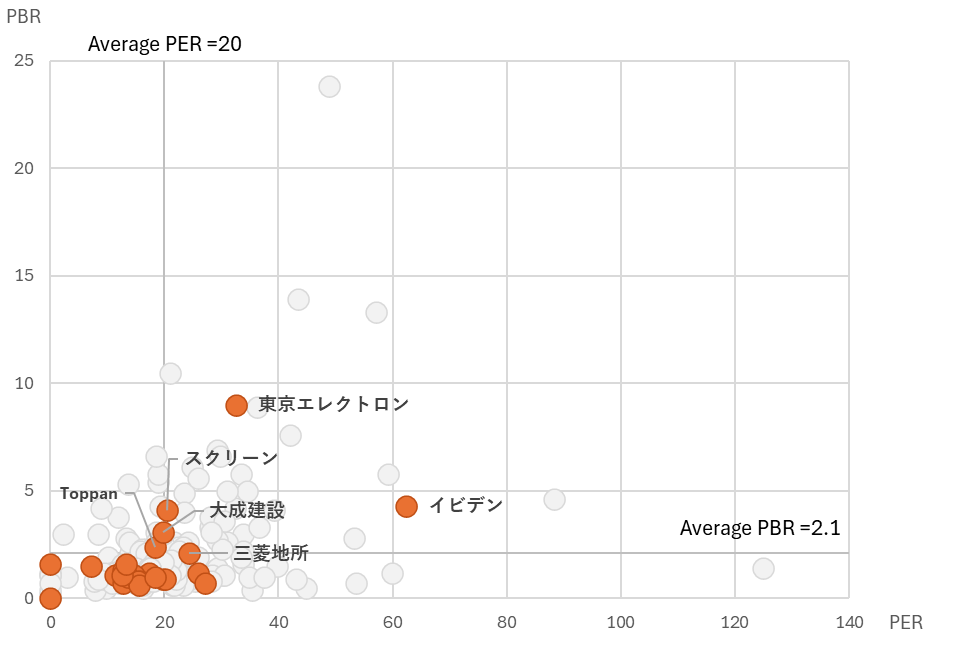

Valuation Analysis(バリュエーション分析)

PER/PBR散布図は、この商業化ギャップをそのまま市場価格に反映している。

Tokyo Electron(8035 JP)はPER約35倍、PBR約9〜10倍で、主因はAI半導体装置であり、ペロブスカイトは付随的な存在である。Screen HD(7735 JP)も市場平均を上回るが、主因は半導体ウェーハ洗浄(世界1位)である。ただし、同社のロール・ツー・ロール直接塗工技術は、水素向けCCM(触媒塗工膜)で商用化されており、東京ガスは2025年12月に受注を開始し、2030年に100億円のPEM電解装置売上を目標としている。11 このプロセスIPはペロブスカイト層形成にも直接応用でき、Screenは水素と太陽光の両方を支えるクロステーマの装置銘柄と位置づけられる。

一方、Toppan HD(7911 JP)、Taisei Construction(1801 JP)、Mitsubishi Estate(8802 JP)、材料系企業など、オレンジ色クラスターの多くは市場平均以下で、ペロブスカイトの価値はゼロとして扱われている。これはタイムラインリスクを考えれば合理的だが、2040年20GW目標に実行可能性があると考える投資家にとっては、現在収益を持ちながら国家政策テーマへの無価格のコールオプションを保有する構造となり、非対称性が生まれる。12

| セルメーカー・開発企業 | 機能材料・コーティング |

| 積水化学工業 / 積水ソーラーフィルム4204 JP | 日産化学4021 JP |

| パナソニックHD6752 JP | 住友化学4005 JP |

| カネカ4118 JP | 三菱ケミカルG4188 JP |

| 東芝6502 JP | 旭化成3407 JP |

| アイシン7259 JP | 富士フイルムHD4901 JP |

| リコー7752 JP | キヤノン7751 JP |

| ガラス基板・封止材 | 出資・導入・不動産 |

| AGC5201 JP | トヨタ自動車7203 JP |

| 日本電気硝子5214 JP | INPEX1605 JP |

| 東レ3402 JP | 三菱地所8802 JP |

| 日東電工6988 JP | 第一生命HD8750 JP |

| TOPPAN HD7911 JP | 大成建設1801 JP |

| 大日本印刷7912 JP | シャープ6753 JP |

| 製造装置・プロセス技術 | 東京電力HD9501 JP |

| SCREENホールディングス7735 JP | 東京ガス9531 JP |

| 東京エレクトロン8035 JP | 日本政策投資銀行非上場 |

| 京セラ 06971 JP |

日本はペロブスカイト太陽電池を開発した国であり、その将来は発明そのものよりも、どれだけ早く量産体制を築けるかに左右されつつある。積水化学による初の商業販売や政策支援、そして他国が短期間では再現しにくい材料エコシステムなど、前向きな要素は揃っている。一方で、中国のギガワット級工場や韓国の大規模投資がすでに世界のペースを決めており、日本がコスト競争力や耐久性、知財保護を確立するための時間は限られている。それでも、日本には依然として実現可能な道筋があり、今後数年の着実かつ迅速な動きが、その技術が国内産業として根付くのか、それとも他国に先行されるのかを決めていく。

References

1. Sekisui Chemical / Sekisui Solar Film, “フィルム型ペロブスカイト太陽電池『SOLAFIL』事業開始のお知らせ,” 27 March 2026.

2. Ministry of Economy, Trade and Industry (資源エネルギー庁), “平地面積あたりの太陽光発電導入容量,” cited in Sekisui Chemical investor presentation, January 2025.

3. METI, GX Supply Chain Construction Support Programme (GXサプライチェーン構築支援事業 第二回公募結果), December 2024; 第7次エネルギー基本計画, 18 February 2025.

4. Clarivate Analytics Japan, perovskite-related international patent filing data, as reproduced in Japanese broadcast media, 2026. “Related patents” = filed in 2+ countries; single-country filings excluded.

5. Enecoat Technologies press releases, 2025; Toyota Motor / Woven Capital investment disclosure, 2024–2025.

6. METI, 次世代型太陽電池に関する国内外の動向等 (資料4), May 2024; company IR disclosures, 2025–2026.

7. GCL Optoelectronics investor presentations, June 2025; UtmoLight company disclosures, February 2025; LONGi Green Energy, NREL-certified cell efficiency record (34.85%), April 2025.

8. Hanwha Solutions investor briefing, rights offering announcement, 2025–2026 (2.4 trillion KRW ≈ $1.6bn).

9. Sekisui Chemical, ペロブスカイト太陽電池事業説明会, 7 January 2025; Nikkei, “積水化学工業系、ペロブスカイト太陽電池の販売を開始,” 27 March 2026; METI, 次世代型太陽電池に関わる動向について, May 2025.

10. PER/PBR data read from chart image (source not disclosed; approximate values, circa early 2026). Market averages PER 20x and PBR 2.1x as labelled in source chart. Not investment advice.

11. Nikkei, “東京ガスとSCREEN、水素製造の電解質膜の受注開始,” 9 December 2025; METI Journal, “脱炭素のカギ握る『水素』,” August 2025.

12. All valuation commentary is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security.