The Takaichi government is steering Japan’s energy strategy toward geothermal — a resource the country holds in abundance but has barely tapped. Meanwhile, Japanese manufacturers already dominate the global market for the turbines that power it all.

Key Takeaways

- Policy signal is credible but execution uncertain. The coalition agreement and 7th Strategic Energy Plan mark the strongest political commitment to geothermal in Japan’s post-war history — yet permitting timelines, national park rules, and hot-spring opposition remain unresolved.

- Japanese turbine makers hold a durable moat. ~70% global turbine market share, built on bespoke engineering and proprietary metallurgy, is not easily replicated — and generates equipment and O&M revenues independent of domestic policy.

- Near-term growth is overseas. Indonesia, Turkey, Kenya, and the Philippines are growing capacity far faster than Japan. Japanese EPC firms and trading houses are well-positioned to capture those revenues.

- Next-generation bets are diversifying. Closed-loop (Eavor), EGS drilling (Fervo, Quaise), and supercritical R&D investments reflect a technology-hedging strategy across the industry.

- Domestic upside is real but back-loaded. If permitting reforms and NEDO’s subsurface surveys yield results, meaningful domestic acceleration is plausible post-2030 — creating demand for turbines, drilling services, and grid integration.

A New Policy Direction for Geothermal

The Takaichi administration, formed in October 2025, has made a decisive break from Japan’s previous “renewables-first” orthodoxy. The coalition agreement between the Liberal Democratic Party and Nippon Ishin no Kai explicitly commits to advancing geothermal as a home-grown competitive advantage while introducing legal curbs on mega-solar installations.1 Prime Minister Sanae Takaichi has positioned geothermal alongside next-generation nuclear reactors and perovskite solar as a pillar of Japan’s clean energy future,2 and the government’s 7th Strategic Energy Plan (February 2025) formalizes the goal of raising geothermal’s share of the power mix from 0.3% to 1–2% by 2040, with an interim capacity target of 1.5 GW by 2030.3 METI established a public-private council in April 2025 to accelerate next-generation geothermal technologies, targeting commercialization by the 2030s.3

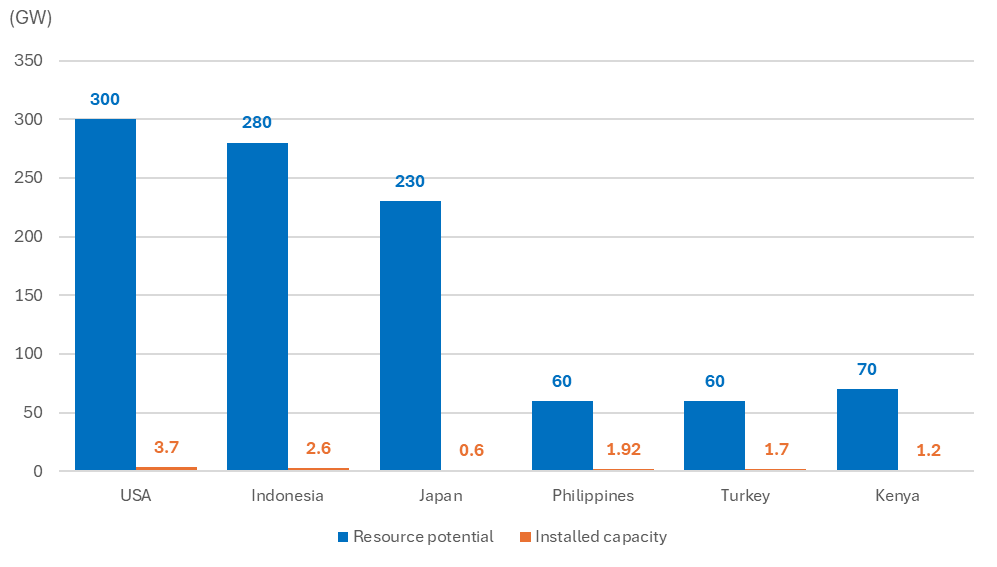

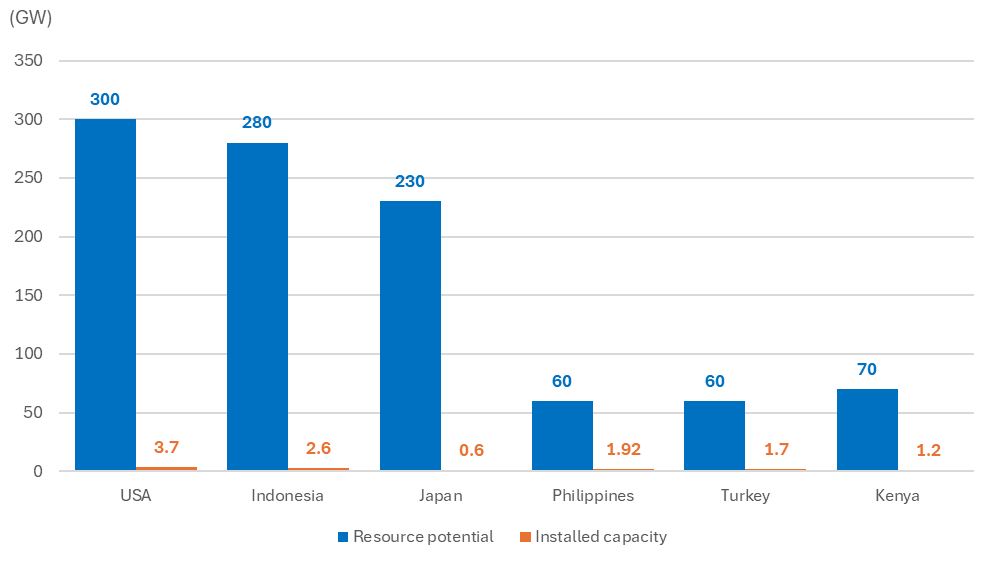

Geothermal resource potential vs. installed capacity — selected countries

Sources: JOGMEC, EIA

Japan’s Geothermal Paradox

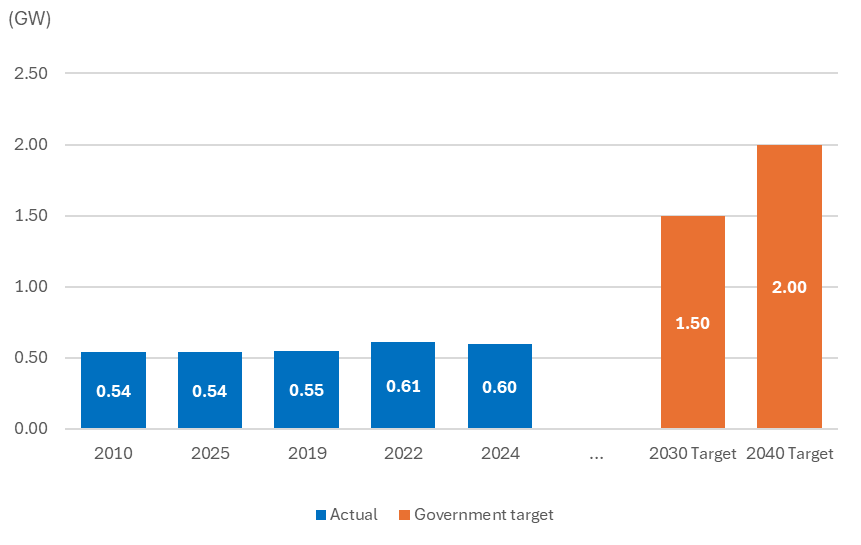

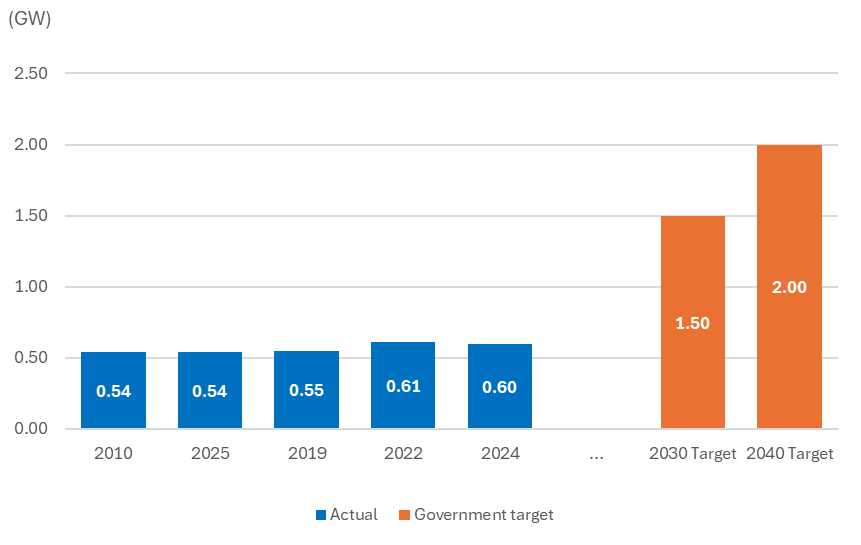

Japan ranks third globally in geothermal resource potential at 23.4 GW, yet its installed capacity of roughly 0.6 GW places it only tenth worldwide — a utilization rate of just 2.6%.4 The structural barriers are well known: project timelines exceeding a decade, high upfront drilling costs, regulatory constraints around national parks (where much of the resource sits), and opposition from hot-spring operators.5 The current 0.6 GW of installed capacity sits well below the government’s own 2030 target of 1.5 GW, and the Agency for Natural Resources and Energy has acknowledged the pace of deployment lags behind plan.3 NEDO is conducting subsurface surveys for supercritical geothermal potential in Iwate, Akita, and Oita prefectures, though full commercial deployment of that technology remains roughly 25 years away.6

Japan geothermal installed capacity: actual vs. government targets

Sources: Agency for Natural Resources and Energy; 7th Strategic Energy Plan

Global Market: Emerging Nations Lead

While Japan stagnates domestically, global geothermal is expanding. IRENA’s 2025 Renewable Capacity Statistics show geothermal added 0.4 GW of new capacity in 2024, led by New Zealand, Indonesia, Turkey, and the United States.7 Turkey grew from 397 MW in 2015 to over 1,500 MW by 2020 through a dedicated geothermal law and feed-in tariff; Indonesia targets 22 GW by 2060 and continues to attract international capital; Kenya has built capacity rapidly with the support of Japanese equipment suppliers and concessional finance.8 Next-generation technologies — Enhanced Geothermal Systems (EGS), closed-loop extraction, and supercritical drilling — are drawing venture capital globally, with U.S. startup activity especially notable following DOE’s “Enhanced Geothermal Shot” target of a 90% cost reduction by 2035.6

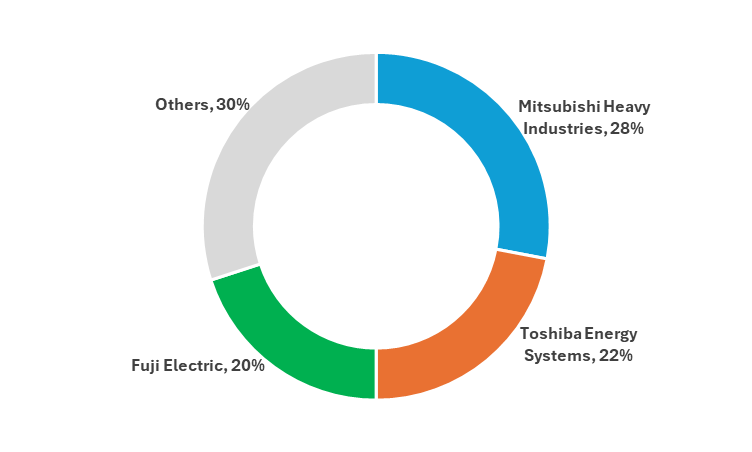

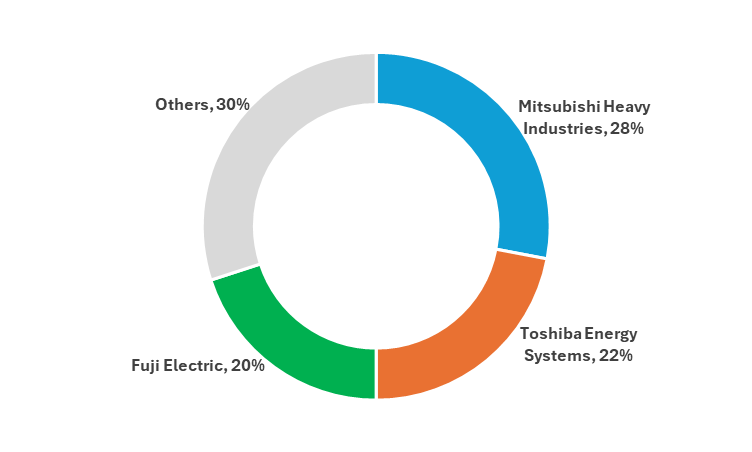

Global geothermal turbine market share — Japanese firms hold ~70%

Sources: Japan Geothermal Association (JGA); Energy White Paper 2025 (METI)

Japanese & Multinational Corporate Activity

Japan’s most durable competitive advantage in geothermal is its manufacturing and engineering capability. Mitsubishi Heavy Industries 7011 JP, Toshiba Energy Systems (Toshiba 6502 JP), and Fuji Electric 6504 JP collectively supply approximately 70% of the world’s geothermal steam turbines — a position built on decades of custom project engineering and proprietary metallurgy.4 MHI has delivered full EPC contracts in Mexico and layered remote monitoring via its TOMONI IoT platform, while also taking a minority stake in U.S. startup Fervo Energy, which applies horizontal shale-drilling techniques to geothermal.9,10 Toshiba Energy Systems has secured equipment contracts across Indonesia and the Philippines and entered an O&M cooperation agreement with Kenya Power.11 On next-generation bets, Mitsubishi Corporation 8058 JP invested in MIT-spin-off Quaise Energy (millimeter-wave deep drilling) in February 2024,12 while Chubu Electric Power 9502 JP and Kajima Corporation 1812 JP have both taken equity stakes in Canadian closed-loop pioneer Eavor Technologies, whose first commercial site in Geretsried, Germany was approaching start-up in late 2025.12 Daido Steel 5471 JP is developing corrosion-resistant alloys for EGS environments, with reported links to Chevron’s geothermal research programme.10

Conclusions

Japan’s geothermal story is one of vast potential constrained by structural friction, now with a credible political tailwind for the first time in years. The Takaichi government’s explicit commitment — backed by the 7th Strategic Energy Plan and the METI public-private council — sets a clearer direction than any previous administration. The hardware moat held by MHI, Toshiba, and Fuji Electric ensures that Japanese industry captures value regardless of where global geothermal expands, while equity investments in Fervo, Quaise, and Eavor signal that leading players are hedging across all next-generation technology pathways. The most investable near-term opportunity lies in offshore project execution across Indonesia, Kenya, and the Philippines; the domestic story is real but requires sustained regulatory reform to close the gap between the 2030 target of 1.5 GW and today’s 0.6 GW.

Japanese translations

日本政府は、これまで十分に活用されてこなかった豊富な地熱資源を軸にエネルギー戦略を転換しつつある。一方で、日本企業は地熱発電を支えるタービン市場で既に世界を支配している。

主要ポイント

政策シグナルは明確だが、実行には不確実性が残る。連立合意と第7次エネルギー基本計画は、戦後で最も強い地熱推進の政治的コミットメントを示している。しかし、許認可の長期化、国立公園規制、温泉事業者の反対といった課題は依然として未解決である。

日本のタービンメーカーは強固な競争優位を持つ。世界の地熱タービン市場の約70%を占めるシェアは、特注設計や独自の金属材料技術に支えられており、容易には模倣できない。これは国内政策に左右されず、設備販売やO&M収益を生み出す。

短期的な成長は海外にある。インドネシア、トルコ、ケニア、フィリピンは日本よりはるかに速いペースで地熱容量を拡大しており、日本のEPC企業や商社はその需要を取り込む好位置にある。

次世代技術への投資は多様化している。クローズドループ(Eavor)、EGS掘削(Fervo、Quaise)、超臨界地熱の研究開発など、業界全体が技術リスクを分散する戦略を取っている。

国内の成長余地は大きいが、実現は先送りされる可能性が高い。許認可改革やNEDOの地下構造調査が成果を出せば、2030年以降に国内の加速が現実味を帯び、タービン、掘削サービス、系統統合への需要が生まれる。

地熱政策の新たな方向性

2025年10月に発足した高市政権は、従来の「再エネ優先」路線から大きく舵を切った。自民党と日本維新の会の連立合意は、地熱を「国産の競争力ある資源」として明確に位置づけ、メガソーラーへの法的規制を導入する方針を示した。高市早苗首相は、地熱を次世代原子炉やペロブスカイト太陽電池と並ぶクリーンエネルギーの柱として位置づけており、2025年2月の第7次エネルギー基本計画では、地熱の電源構成比を0.3%から2040年に1〜2%へ引き上げ、2030年までに1.5 GWの導入を目指す目標が正式化された。経産省は2025年4月に官民協議会を設置し、次世代地熱技術の2030年代の商用化を目指している。

地熱資源量と導入容量の国別比較

出典:JOGMEC、EIA

日本の地熱パラドックス

日本は23.4 GWの地熱資源量で世界3位だが、導入容量は約0.6 GWにとどまり、世界10位に過ぎない。利用率はわずか2.6%である。プロジェクト期間が10年以上に及ぶこと、高額な掘削コスト、国立公園規制、温泉事業者の反対など、構造的な障壁はよく知られている。現在の0.6 GWは政府の2030年目標である1.5 GWを大きく下回っており、経済産業省資源エネルギー庁も導入ペースが計画に遅れていると認めている。NEDOは岩手・秋田・大分で超臨界地熱の地下調査を進めているが、商用化は約25年先と見込まれている。

日本の地熱導入容量:実績と政府目標

出典:資源エネルギー庁、第7次エネルギー基本計画

世界市場:新興国が主導

日本が停滞する一方、世界の地熱市場は拡大している。IRENAの2025年統計によれば、2024年には0.4 GWの新規地熱容量が追加され、ニュージーランド、インドネシア、トルコ、米国が牽引した。トルコは2015年の397 MWから2020年には1,500 MW超へと急成長し、インドネシアは2060年までに22 GWを目指し国際資本を呼び込んでいる。ケニアは日本の設備メーカーと円借款の支援を受けて急速に容量を拡大した。EGS、クローズドループ、超臨界掘削などの次世代技術には世界的にベンチャー投資が集まり、特に米国ではDOEの「Enhanced Geothermal Shot」による2035年までの90%コスト削減目標が後押ししている。

地熱タービンの世界市場シェア:日本企業が約70%を占有

出典:日本地熱協会、エネルギー白書2025(経産省)

日本企業と多国籍企業の動向

日本の最も強固な競争優位は製造・エンジニアリング能力にある。三菱重工、東芝エネルギーシステムズ、富士電機は世界の地熱タービンの約70%を供給しており、特注設計と独自の金属材料技術に基づく地位は揺るがない。三菱重工はメキシコでEPCを提供し、TOMONI IoTプラットフォームによる遠隔監視も展開しているほか、米国のFervo Energyに出資している。東芝はインドネシアとフィリピンで設備契約を獲得し、ケニア電力とはO&M協力を結んでいる。三菱商事は2024年にMIT発のQuaise Energy(ミリ波深部掘削)に出資し、中部電力と鹿島建設はカナダのクローズドループ企業Eavor Technologiesに出資している。大同特殊鋼はEGS環境向けの耐腐食合金を開発しており、Chevronの地熱研究との関連も報じられている。

結論

日本の地熱は巨大な潜在力を持ちながら構造的な摩擦に阻まれてきたが、久しぶりに明確な政治的追い風が生まれている。第7次エネルギー基本計画と経産省の官民協議会に裏付けられた高市政権の明確なコミットメントは、これまでにない方向性を示している。三菱重工、東芝、富士電機が持つ強固なハードウェアの競争優位は、世界のどこで地熱が拡大しても日本企業が価値を獲得できることを意味し、Fervo、Quaise、Eavorへの出資は次世代技術への分散投資を示している。短期的に最も投資可能性が高いのはインドネシア、ケニア、フィリピンなど海外のプロジェクト実行であり、国内市場は実在するものの、2030年の1.5 GW目標と現在の0.6 GWのギャップを埋めるには継続的な規制改革が必要となる。

References

1. Sankei News, “Geothermal development promoted, written into LDP–Ishin coalition agreement” (Oct. 23, 2025).

2. IEEI, “Reading the Takaichi government’s energy and environmental policy” (Nov. 5, 2025).

3. Agency for Natural Resources and Energy, “1st FY2025 Geothermal Promotion Study Group Summary” (Sep. 25, 2025).

4. Japan Geothermal Association (JGA), “Characteristics of geothermal power” and “Geothermal power worldwide.” Notes: 0.52 GW refers only to large flash geothermal plants, whereas 0.6 GW represents the total installed capacity including binary units used in recent statistics from Japan’s Agency for Natural Resources and Energy.

5. ScopeX, “Geothermal power generation: latest trends and corporate case studies” (Nov. 6, 2025).

6. Shizen Hatch, “Supercritical geothermal power generation: developments and challenges” (Sep. 11, 2025).

7. IRENA, “Record-Breaking Annual Growth in Renewable Power Capacity” (Mar. 2025).

8. Eleminist, “Geothermal power — global and Japan country comparison.”

9. Mitsubishi Heavy Industries, “TOMONI real-time monitoring at Domo de San Pedro geothermal plant, Mexico.”

10. Mitsubishi UFJ eSmart Securities, “Geothermal power: a look at key stocks” (Mar. 26, 2025).

11. Toshiba Energy Systems & Solutions, “Geothermal power: products and technical services.”

12. IEEI / Takeuchi, “Next-generation geothermal technology developments” (Jan. 15, 2026).