Photo by Sergio Kian on Unsplash. This article contains AI‑generated content. Please exercise caution and verify all critical information with primary sources before using it for analysis or decision‑making.

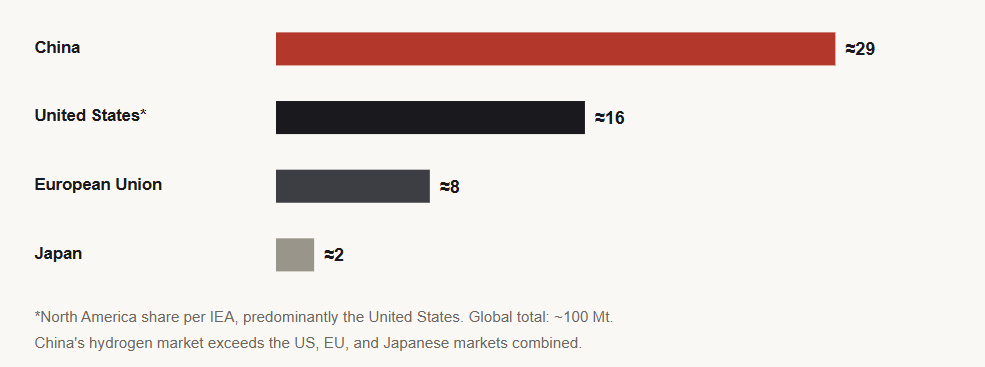

Every conversation about the global hydrogen economy must now begin in China, because that is where most of it physically exists. By the end of 2024, China was producing and consuming more than 36.5 million tonnes of hydrogen annually, the largest volumes of any nation.FN1 Against global demand of roughly 100 million tonnes recorded by the International Energy Agency for 2024, China alone accounts for approximately one third of world production and 29 percent of world consumption.FN2 The next largest demand centers, North America at 16 percent and the Middle East at 15 percent, are not peers but distant followers.FN3 Installed production capacity in China has reached 50 million tonnes per year, leaving substantial headroom above current output.FN4

The comparison with the other major hydrogen jurisdictions makes the asymmetry vivid. The European Union consumes roughly 8 million tonnes of hydrogen and ammonia feedstock annually across industry and refining, while Japan, the country that coined the phrase “hydrogen society,” consumes approximately 2 million tonnes, a figure its own strategy expects to multiply tenfold only by mid-century.FN5 China’s market is thus larger than the American, European, and Japanese markets combined, and the gap is structural: hydrogen demand follows heavy industry, and heavy industry followed globalization to China decades ago.

HYDROGEN DEMAND BY REGION, 2024 (Mt per year)

Notes: This figure includes AI‑generated content and may contain inaccuracies, omissions, or interpretive elements. All quantitative values and analytical conclusions should be verified against primary sources before use in technical, financial, or policy decision‑making. Hydrogen demand by major jurisdiction, 2024. Hydrogen consumption tracks heavy industry, refining, and chemicals, which is why the map of hydrogen is, to a first approximation, a map of industrial production. Source: SIDR analysis of IEA Global Hydrogen Review and Hydrogen Europe data.

The honest caveat is that this is not yet a clean hydrogen empire. Of the roughly 37 million tonnes China actually produced in 2024, about 21 million tonnes came from coal gasification, 8 million tonnes from natural gas reforming, most of the remainder from industrial byproduct streams, and only about 0.5 million tonnes from electrolysis.FN6 Grey and brown molecules still constitute roughly 85 percent of the market by value.FN7 What distinguishes China is not the present color of its hydrogen but the speed at which the palette is changing, and the fact that the machinery of that change is overwhelmingly manufactured at home.

The Green Inflection: Technology Deployment

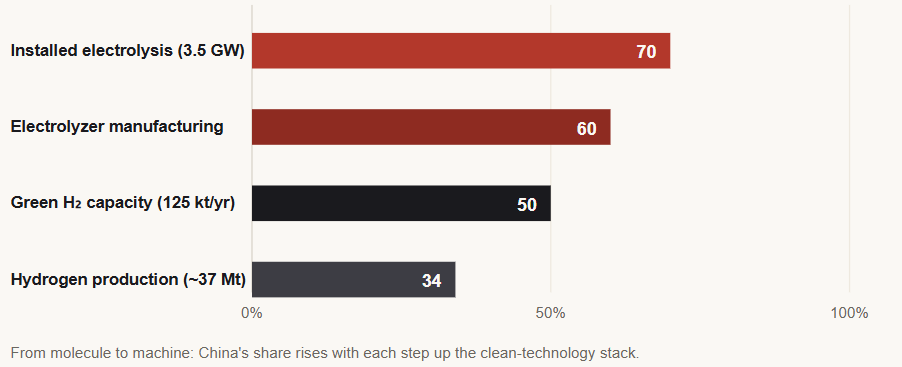

The electrolysis numbers are where the story turns from incumbency to ambition. China had established 125,000 tonnes per year of green hydrogen production capacity by the end of 2024, equal to roughly half of the global total of 250,000 tonnes, after capacity grew 62 percent year over year.FN8 Installed electrolyzer capacity stood at 3.5 gigawatts, approximately 70 percent of the world’s total, with projections pointing toward 50 gigawatts by 2030.FN9 Upstream, the dominance is even more pronounced: Chinese firms’ share of global electrolyzer manufacturing capacity rose from 5 percent to roughly 60 percent in just six years, an industrial replay of the solar photovoltaic playbook, although that share is expected to normalize toward 30 percent by 2030 as Western capacity comes online.FN10

The technological division of labor is instructive. China dominates low-cost alkaline electrolysis but still trails the West in proton exchange membrane systems and in transport, storage, and certain industrial applications, which keeps the race genuinely open in the higher-value segments where Japanese and European engineering retains an edge.FN11 On the utilization side, China’s deployment of fuel cell vehicles, refueling stations, and co-firing retrofits proceeds in parallel, a full-stack approach that contrasts with Europe’s production-first strategy and Japan’s import-and-utilize model. Geography reinforces the production thesis: the northern and western provinces combine some of the world’s cheapest wind and solar resources with vast land and chronic curtailment of renewable generation. Sinopec’s 260 megawatt Kuqa facility in Xinjiang and Envision Energy’s off-grid plant in Chifeng, Inner Mongolia, which opened with 0.32 million tonnes per year of green ammonia capacity and plans to reach 1.5 million tonnes by 2028, convert stranded electrons into transportable molecules.FN12

CHINA’S SHARE OF GLOBAL DEPLOYMENT, END-2024 (%)

Notes: This figure includes AI‑generated content and may contain inaccuracies, omissions, or interpretive elements. All quantitative values and analytical conclusions should be verified against primary sources before use in technical, financial, or policy decision‑making. Production and utilization technology deployment. China’s share of the hydrogen economy increases the closer one moves to the green frontier: a third of all production, half of green capacity, 70 percent of installed electrolysis. Source: SIDR analysis of NEA, IEA, and Pacific Forum data.

The Cost Curve Belongs to Beijing

Hydrogen economics are conventionally taught as a color spectrum. Grey hydrogen from unabated natural gas costs roughly 1 to 3 dollars per kilogram depending on the market; blue hydrogen, which adds carbon capture, runs approximately 1.8 to 4.7 dollars; and green hydrogen from electrolysis has historically ranged from about 3.5 dollars to well above 6 dollars per kilogram, and in high-cost Western configurations as much as 12 dollars.FN13 China rewrites this hierarchy through equipment costs. With domestic alkaline electrolyzers priced near 360 dollars per kilowatt, roughly a quarter of Western equivalents, green hydrogen produced with Chinese technology spans approximately 2.4 to 5.9 dollars per kilogram, and BloombergNEF identified China as the only major market where green hydrogen already undercuts blue.FN14

Official data confirm the descent. The National Energy Administration reported that average production costs fell to 28 yuan per kilogram, about 3.85 dollars, by December 2024, down 15.6 percent in a single year, although delivered prices near 48.6 yuan reveal how much value still leaks into compression and trucking.FN15 Bloomberg projects Chinese production costs of roughly 2.5 dollars per kilogram by 2030 and 1.6 dollars by 2050, trajectories at which green hydrogen ceases to be a subsidy artifact and becomes an ordinary industrial input.FN16 Policy has now attached explicit price targets to this curve: Beijing’s March 2026 hydrogen application pilot calls for terminal prices below 25 yuan per kilogram by 2030, with leading regions targeting roughly 15 yuan.FN17

Trucks, Not Cars: Mobility at Continental Scale

China’s fuel cell vehicle program is best understood as freight logistics policy rather than automotive policy. Annual fuel cell vehicle sales have run at roughly 7,000 units in both 2023 and 2024, before climbing toward approximately 10,000 units in 2025 on the strength of renewed subsidies, while cumulative deployment approached 40,000 vehicles supported by 574 hydrogen refueling stations with combined capacity above 360 tonnes per day.FN18 These annual volumes exceed the fuel cell bus and commercial fleet deployments of Japan and South Korea, which Nikkei Automotive has placed in the range of 100 to 150 units per year, by more than an order of magnitude.FN19 The composition is revealing: trucks accounted for roughly 98 percent of 2025 deployments, with heavy trucks alone at 70 percent, while buses, the original demonstration vehicle, fell to a residual 2 percent.FN20

The logic is geographic. Moving goods from Xinjiang to Shanghai or from Heilongjiang to Guangdong means thousands of kilometers, heavy payloads, and in the north, winters that punish battery chemistry. For such corridors, fuel cells offer the diesel-like virtues of fast refueling, long range, and payload preservation, which is precisely why Beijing’s 2026 pilot policy designates medium and heavy trucks, long-haul logistics, and cold-chain transport as the core scenarios, with a national target of 100,000 fuel cell vehicles by 2030.FN21 Intellectual honesty, however, requires acknowledging the competing fact pattern: battery-electric heavy trucks reached a 22 percent sales share in the first half of 2025 and roughly 230,000 full-year units, dwarfing the cumulative hydrogen fleet and confining fuel cells, for now, to the corridors where batteries genuinely fail.FN22 Hydrogen trucking in China is a hedge with state backing, not yet a market verdict.

China is not betting that hydrogen beats batteries. It is betting that owning every link of the hydrogen value chain costs little and forecloses nothing.

The Policy Architecture: From Plan to Law

The institutional scaffolding explains the persistence. The Medium and Long-Term Plan for the Hydrogen Energy Industry, issued by the NDRC and NEA in March 2022, established hydrogen as a component of the future national energy system, set 2025 targets of 50,000 fuel cell vehicles and 100,000 to 200,000 tonnes of renewable hydrogen, and laid out staged objectives through 2035, when renewable hydrogen is to play a meaningful role in terminal energy consumption.FN23 The decisive legal upgrade came with China’s first Energy Law, effective January 1, 2025, which for the first time classified hydrogen as an energy resource on par with fossil fuels and renewables rather than as a hazardous chemical, dissolving a regulatory ambiguity that had constrained siting and pipeline development.FN24

Beneath the national layer sits an unusually dense provincial apparatus: more than 560 hydrogen-specific policies had been issued nationwide by the end of 2024, and 22 provincial-level governments had written hydrogen into their work reports.FN25 Five demonstration city clusters anchored on Beijing-Tianjin-Hebei, Shanghai, Guangdong, Hebei, and Henan organize fuel cell vehicle subsidies, while the December 2024 implementation plan from MIIT, NDRC, and NEA extended the push into industrial decarbonization, and the 15th Five-Year Plan period targets regional self-sufficiency in renewable and low-carbon hydrogen.FN26 The motivations are layered: the dual carbon commitments of peaking before 2030 and neutrality by 2060, energy security in a country that imports most of its oil, an industrial strategy that seeks to repeat in electrolyzers what was achieved in solar modules and lithium batteries, and a grid-management imperative to absorb renewable curtailment in the west.

Hydrogen Into the Power Plant

The most consequential and least appreciated frontier is power generation, where hydrogen arrives mostly disguised as ammonia. The NDRC’s 2024 to 2027 action plan directs coal-fired plants to cut carbon intensity roughly 20 percent by 2025 and 50 percent by 2027 relative to 2023 industry averages, naming three retrofit pathways: biomass co-firing, green ammonia co-firing, and carbon capture, with retrofitted units required to achieve at least 10 percent co-firing capability by 2027.FN27 Flagship projects include the conversion of a 300 megawatt unit in Anhui province to fire entirely on ammonia, coupled to dedicated solar-based fuel production.FN28 Academic modelling suggests the prize is material: geospatially optimized green ammonia co-firing across China’s young coal fleet could abate a cumulative 7.8 to 15.2 gigatonnes of CO₂ through 2060, mitigating the carbon lock-in of 600 gigawatts of post-2010 coal capacity.FN29

The economics remain the obstacle. At a hydrogen price of 5 dollars per kilogram, Rystad Energy estimates a 10 percent ammonia blend raises the levelised cost of electricity by roughly half relative to coal-only generation, which is why critics view co-firing as life support for coal rather than a bridge away from it.FN30 Yet this is exactly where China’s cost curve matters: if domestic green hydrogen approaches 1.5 to 2 dollars per kilogram in the 2030s, the arithmetic of co-firing, and eventually of dedicated hydrogen turbines, changes category. Hydrogen power generation in China should therefore be read as an option being purchased cheaply today, exercisable if and when the molecule’s price intersects the carbon constraint.

2030: Four Strategies, One Race

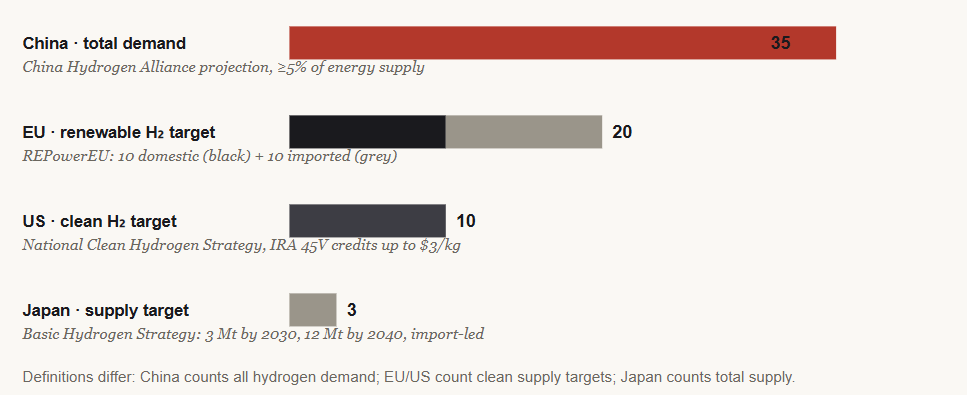

How large does this become, and how does it compare with the rest of the world’s ambitions? The China Hydrogen Alliance projects national hydrogen demand of 35 million tonnes by 2030, representing at least 5 percent of energy supply, rising to 60 million tonnes and 10 percent by 2050 and 100 million tonnes and 20 percent by 2060, with the renewable share of supply reaching roughly 15 percent by 2030 and approaching 80 percent by 2060.FN31 The European Union’s REPowerEU strategy targets 20 million tonnes of renewable hydrogen by 2030, split evenly between 10 million tonnes of domestic production and 10 million tonnes of imports, although industry trackers see firm 2030 demand closer to 8 to 10 million tonnes.FN32 The United States, armed with production tax credits of up to 3 dollars per kilogram under the Inflation Reduction Act, has set a national target of 10 million tonnes of clean hydrogen by 2030, while Japan’s revised Basic Hydrogen Strategy aims for a supply of 3 million tonnes by 2030 and 12 million tonnes by 2040, much of it imported.FN33 The IEA, for its part, expects low-emission hydrogen to grow from under 1 percent of global supply today to around 4 percent by 2030, a sober reminder that every jurisdiction’s targets exceed the project pipeline.FN34

2030 HYDROGEN AMBITIONS BY REGION (Mt per year)

Notes: This figure includes AI‑generated content and may contain inaccuracies, omissions, or interpretive elements. All quantitative values and analytical conclusions should be verified against primary sources before use in technical, financial, or policy decision‑making. Regional hydrogen market outlook to 2030. China’s projected demand alone approaches the combined ambitions of the EU, US, and Japan, and unlike the Western targets it is anchored to an existing 36.5 Mt industrial base rather than a greenfield buildout. Source: SIDR analysis of China Hydrogen Alliance, European Commission, US DOE, and METI targets.

Decarbonization and the Coal Question

Can hydrogen decarbonize China? Not alone, and the data are refreshingly clear about the actual hierarchy of drivers. In 2025, coal-fired generation fell 1.9 percent even as electricity demand rose 5 percent, the first time in a decade that clean sources covered all incremental demand, suggesting power-sector emissions may have peaked in 2024.FN35 That achievement belongs overwhelmingly to wind and solar, whose combined capacity has grown more than tenfold in a decade to 1,842 gigawatts, with nuclear as the firm-power second pillar: 62 gigawatts operating at the end of 2025 and a 15th Five-Year Plan target of 110 gigawatts by 2030, the world’s largest construction program.FN36 Hydrogen’s direct contribution to emissions reduction remains modest in absolute terms; the 2021 to 2035 plan itself claimed only 1 to 2 million tonnes of annual CO₂ savings from its 2025 green hydrogen target.FN37

Nor is coal exiting the stage. China commissioned 78 gigawatts of new coal capacity in 2025, the most in a decade, and proposals surged to 161 gigawatts, even as the existing fleet’s utilization slid to 48 percent and its function migrated from baseload supply toward grid balancing.FN38 The correct synthesis is that renewables are the engine of Chinese decarbonization, nuclear is the firm foundation, and hydrogen is the connective tissue: the storage medium for curtailed wind, the feedstock that decarbonizes steel, chemicals, and ammonia, the fuel for freight corridors batteries cannot serve, and the optionality embedded in a coal fleet that Beijing refuses to strand. Coal will remain the system’s shock absorber well into the 2030s, but its role is being hollowed out from three directions at once, and hydrogen is the direction Western analysis most consistently underweights.

Conclusions

The investment-relevant conclusion is that China has converted hydrogen from an energy debate into a manufacturing fact. It holds roughly a third of global production, half of global green capacity, 70 percent of installed electrolyzers, and the only cost structure in which green hydrogen already beats blue. The demand side, 40,000 fuel cell vehicles against millions of battery-electric ones, remains embryonic and may disappoint romantics. But the supply side is being built with the same patient overcapacity that previously crushed the global price of solar modules and lithium cells, and history suggests that whoever owns the cost curve eventually owns the market. For investors in electrolyzer components, ammonia logistics, fuel cell materials, and the Japanese and Korean equipment makers now competing on quality against Chinese scale, the question is no longer whether the hydrogen economy arrives, but the extent to which it arrives speaking Mandarin.

References

FN1 China Daily, “Nation takes global lead in hydrogen energy output,” May 2025.

FN2 IEA, Global Hydrogen Review 2025; IEA, Hydrogen energy system overview.

FN3 IEA, Global Hydrogen Review 2025, regional demand shares, as reported by Databoks.

FN4 German Energy Partnership, “China’s Hydrogen Sector 2025: Balancing Growth and Challenges,” 2025.

FN5 Hydrogen Europe, Clean Hydrogen Monitor (EU demand pipeline); International Chamber of Shipping, “Turning Hydrogen Demand Into Reality” (Japan demand trajectory).

FN6 German Energy Partnership, “China’s Hydrogen Sector 2025,” production breakdown by feedstock, end‑2024.

FN7 MarketsandMarkets, China Hydrogen Generation Market Report 2025–2030.

FN8 S&P Global Commodity Insights, “China has established 125,000 mt/year of green hydrogen production capacity: NEA,” April 2025.

FN9 German Energy Partnership, “China’s Hydrogen Sector 2025,” electrolysis capacity statistics.

FN10 Asia Times / Pacific Forum, “China’s hydrogen electrolyzer dominance and global risks,” November 2025; German Energy Partnership 2030 share outlook.

FN11 German Energy Partnership, “China’s Hydrogen Sector 2025,” technology assessment (ALK vs PEM, transport and storage).

FN12 Hydrogen Insight (Kuqa project context); CarbonCredits / Ammonia Energy Association, Envision Chifeng plant, 2025.

FN13 BloombergNEF cost survey via Hydrogen Insight, July 2023; ScienceDirect, “Techno‑economic analysis of hydrogen production,” 2025.

FN14 Hydrogen Insight, “Blue hydrogen cheaper than green H₂ in all markets except China: BNEF,” July 2023.

FN15 S&P Global Commodity Insights, NEA China Hydrogen Industry Development Report (2025), cost data.

FN16 Lexology / Bloomberg forecast cited in “China: New Policies Boost Low‑Carbon Hydrogen in Industrial Sector,” January 2025.

FN17 Gasgoo, “China Targets 100,000 Fuel Cell Vehicles in Operation by 2030,” March 2026 MIIT pilot notice.

FN18 ChinaEVHome, “China’s Hydrogen Fleet Hits 10k Milestone, Surging 47% in 2025,” March 2026; Gasgoo, cumulative sales and refueling station data.

FN19 Nikkei Automotive, “水素の灯を消すな” (Do Not Extinguish the Hydrogen Flame), deployment comparison for Japan and South Korea.

FN20 ChinaEVHome / Cui Dongshu (CPCA), 2025 fuel cell vehicle market structure.

FN21 Gasgoo, March 2026 pilot notice, core application scenarios and 2030 fleet target.

FN22 CleanTechnica / ICCT, “Hydrogen Trucks in China Are a Policy Side Bet, Not a Market Winner,” March 2026.

FN23 NDRC / NEA, Medium and Long‑Term Plan for the Development of the Hydrogen Energy Industry (2021–2035); IEA Policies Database.

FN24 Lexology, Energy Law of the PRC effective 1 January 2025, hydrogen reclassification.

FN25 China Daily / NEA, national and provincial hydrogen policy counts, end‑2024.

FN26 Chinabuses.org, five demonstration city clusters; Fuel Cells Works, “China Targets Industrial Green Hydrogen Growth in 15th Five‑Year Plan,” November 2025.

FN27 S&P Global Commodity Insights, “China to test run biomass, ammonia and carbon capture in coal‑fired plants,” July 2024; Ammonia Energy Association, NDRC 2024–2027 action plan.

FN28 Ammonia Energy Association, Wanneng Tongling 300 MW full‑ammonia retrofit, Anhui province.

FN29 Nature Communications, “Geospatial green ammonia co‑firing in China’s coal power fleets to avoid CO₂ emissions lock‑in,” 2026.

FN30 Rystad Energy, “Asia turns to ammonia co‑firing despite supply and cost pressures,” August 2025.

FN31 China Hydrogen Alliance projections via China Briefing; Institut Montaigne, renewable hydrogen share projections.

FN32 European Commission, REPowerEU hydrogen targets; Hydrogen Europe, Clean Hydrogen Monitor demand pipeline.

FN33 US DOE, National Clean Hydrogen Strategy and IRA Section 45V credits, via Kings Research hydrogen economy review; METI, Basic Hydrogen Strategy (revised 2023).

FN34 IEA, hydrogen energy system overview: low‑emission hydrogen share to 2030.

FN35 Wood Mackenzie via GreentechLead, “China Coal Power Generation Falls 1.9% in 2025,” February 2026.

FN36 World Nuclear Association, “Nuclear Power in China,” 15th Five‑Year Plan nuclear targets; CSIS, “China’s Nuclear Energy Priorities,” 2026.

FN37 NDRC, 2021–2035 hydrogen plan, stated CO₂ reduction from 2025 renewable hydrogen target.

FN38 CREA / Global Energy Monitor via OilPrice, coal capacity additions and proposals, 2025–2026.