Photo by Scot Webb. This article contains AI‑generated content. Please exercise your own judgment and independently verify any important points.

A vertically integrated electrolyzer manufacturer is betting that integration, pressure, and scale, rather than a single laboratory efficiency record, are what reduce the levelized cost of clean hydrogen on American soil.

Electric Hydrogen, known as EH2, builds the machine that makes hydrogen rather than the fuel cell that burns it. Founded in 2020 in Devens, Massachusetts by a team that ran technology at First Solar, it became green hydrogen’s first unicorn in 2023 on a 380 million dollar round at a one billion dollar valuation, and has raised roughly 776 million dollars in total.FN1FN2 Its product is a turnkey hundred-megawatt plant called the HYPRPlant, with the critical parts designed and built in-house at a 1.2-gigawatt factory, a manufacturing-first approach lifted straight from solar.FN3

How it makes hydrogen

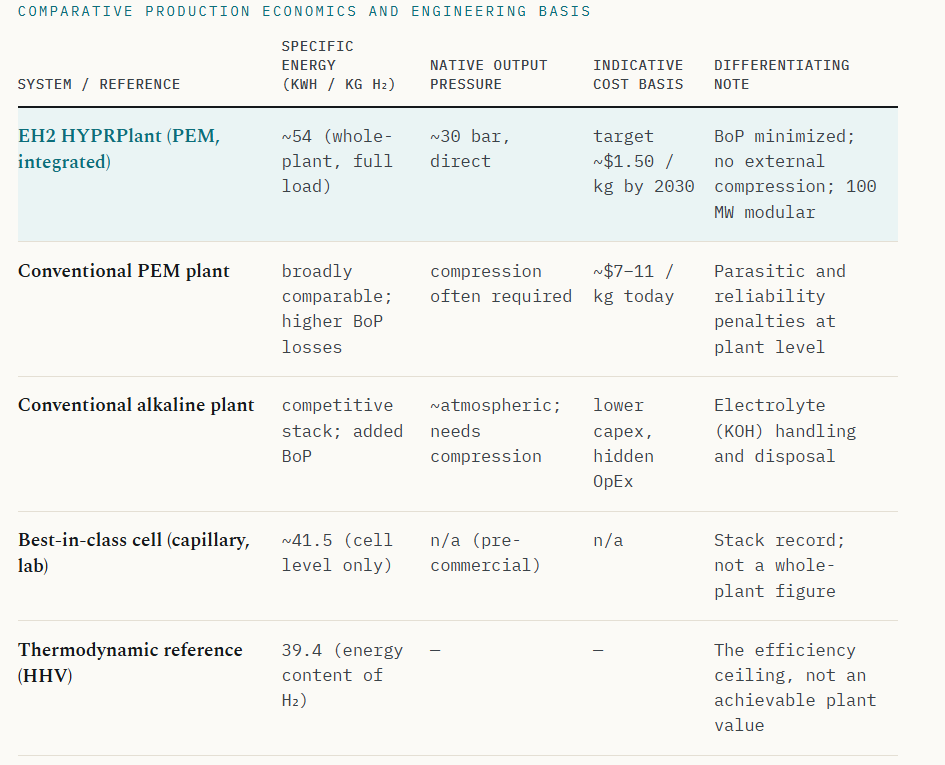

Renewable power splits purified water into hydrogen and oxygen inside stacks of PEM cells. The clever part is the engineering around the stack: the hydrogen comes out already at about thirty bar, so no separate compressor is needed, and the plant is built to keep parasitic losses low, landing at roughly 54 kilowatt-hours per kilogram across the whole plant. The design is validated by DNV, which matters for getting projects financed.FN4 One plant runs at 100 MW and makes about 50 tonnes of hydrogen a day; a pilot called Pioneer proved the whole thing at one-tenth scale first.FN5

Renewable‑Powered Hydrogen Production Flow

This illustration contains AI‑generated content and may include inaccuracies or omissions. Users should independently verify all assumptions. The production path. The two design bets are direct ~30 bar output (skips a compressor) and a repeatable 100 MW module.FN4FN5

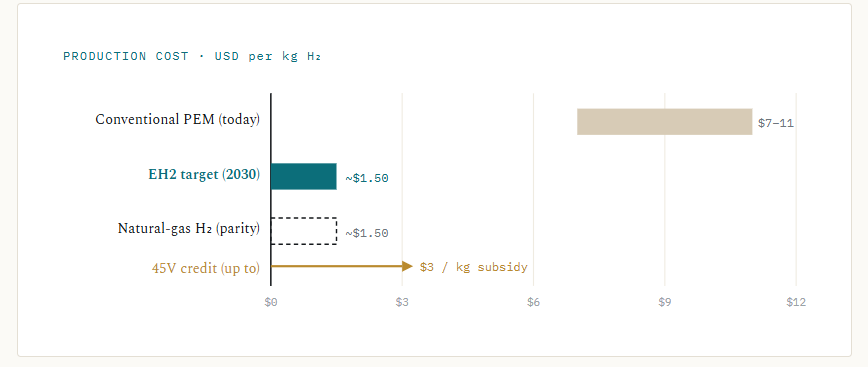

Why it can win on price

EH2 does not make the most efficient cell, and it does not claim to. Its bet is on the cheapest finished plant. By skipping compression, integrating the balance of plant, and driving cost down through manufacturing, it aims to let customers in sunny, windy states make hydrogen for about 1.50 dollars per kilogram by 2030, close to fossil-based hydrogen and far below the 7 to 11 dollars a conventional PEM plant costs today.FN6 The chart below is the whole investment thesis in one picture.PRODUCTION COST · USD per kg H₂$3$6$9$12$0Conventional PEM (today)$7–11EH2 target (2030)~$1.50Natural-gas H₂ (parity)~$1.5045V credit (up to)$3 / kg subsidyFigure 2. Where EH2 wants to be. The gap between today’s conventional PEM cost and the 2030 target is the prize; the 45V tax credit (up to $3/kg) closes much of any remaining gap to fossil parity.FN6FN9

Hydrogen Production Cost Benchmarks and Policy Impacts

This chart contains AI‑generated content and may include inaccuracies or omissions. Users should independently verify all assumptions. Figures are not strictly like-for-like; the EH2 number is a whole-plant value. See FN4, FN6, FN7.

The wager is not that EH2 builds the most efficient cell, but that it builds the lowest-cost plant. In hydrogen, those are different competitions, and only the second one is bankable.

Subsidy: hydrogen got off lightly

The key incentive is the 45V Clean Hydrogen Production Credit, worth up to 3 dollars per kilogram for ten years.FN9 The One Big Beautiful Bill Act, signed in July 2025, did trim it: projects must now start construction before 2028 instead of 2033.FN10 But here is the surprise. The House wanted to kill the credit at the end of 2025; the Senate added a two-year reprieve, and the credit kept its value, its term, and its direct-pay and transfer features. It was even exempted from the new foreign-entity rules, while wind and solar credits were cut off entirely after 2027.FN10FN11 So under a Trump administration rolling back clean energy, hydrogen fared notably better than the rest of the renewable field. The practical effect is a race: whoever breaks ground before 2028 captures the credit, which rewards exactly the fast, pre-built deployment EH2 is built for.

The model and the growth plan

EH2 used to only sell equipment, which left it waiting on slow third-party developers. In May 2025 it fixed that by buying developer Ambient Fuels and adding roughly 400 million dollars of project finance from Generate Capital.FN12 That turns EH2 into a one-stop developer that can also just sell the hydrogen as a service, with project money flowing from 2026.FN12 Growth runs on three tracks: factory volume against a reservation book above 5 gigawatts; self-developed projects that consume its own plants (early customers include eFuels maker Infinium in Texas and New Fortress Energy); and new geography, including a recent push into Latin America.FN8

Does it sell to AI data centers?

Not directly, and this is worth being honest about. Data-center power demand is exploding, roughly 450 terawatt-hours in 2025 heading toward 980 by 2030, and fuel-cell makers have signed billions in deals to supply it.FN13 But those fuel cells (Bloom, FuelCell Energy) mostly run on natural gas, and EH2 makes electrolyzers, not fuel cells. EH2 only benefits if behind-the-meter power shifts toward clean hydrogen, in which case it would be the upstream molecule supplier. That is real option value, helped by the fact that investor Microsoft is already testing hydrogen fuel-cell backup for its data centers, but it is a future possibility, not a signed contract.FN14

The bet is simple: make the cheapest plant, not the best cell, and break ground before the 2028 subsidy clock runs out.

References

FN1 Founded 2020, Devens MA, ex‑First Solar founders; PitchBook; TechCrunch (2023). Notes: Electric Hydrogen Co., known to its customers and investors as EH2, occupies an unusual position in the clean‑energy capital stack: it is neither a fuel‑cell vendor nor, until recently, a producer of hydrogen at all, but rather the manufacturer of the machine that makes the molecule. Founded in 2020 and headquartered in Devens, Massachusetts, the company was assembled by a founding team drawn from the upper ranks of First Solar, chief executive Raffi Garabedian and co‑founder David Eaglesham having both served as that company’s chief technology officer, and it carries forward a thesis imported wholesale from photovoltaics: that the path to fossil parity runs through manufacturing discipline, power density, and ruthless cost engineering rather than through subsidy alone.

In October 2023 the firm became the green‑hydrogen sector’s first unicorn, completing an oversubscribed Series C of 380 million dollars at a valuation of one billion, and it has since drawn cumulative funding on the order of 776 million dollars across roughly two dozen investors. That register of backers, namely Microsoft’s Climate Innovation Fund, BP Ventures, Fortescue, United Airlines Ventures, and the United States Department of Energy, reads less like a venture syndicate than a roster of prospective offtakers and strategic partners, which is precisely the point.

FN2 First unicorn; $380M Series C at $1B; ~$776M raised in total; TechCrunch; PitchBook.

FN3 Turnkey 100 MW HYPRPlant; in-house build at 1.2 GW Devens factory; Electric Hydrogen; The Silicon Review.

FN4 PEM, ~30 bar direct output, ~54 kWh/kg whole plant, DNV validated; EH2 “PEM vs. Alkaline” whitepaper (Dec 2024).

FN5 100 MW, ~50 t/day; Pioneer pilot at one‑tenth scale; Electric Hydrogen.

FN6 ~$1.50/kg target by 2030; conventional PEM ~$7–11/kg; The Silicon Review; EH2 whitepaper.

FN7 HHV of hydrogen = 39.4 kWh/kg; HOMER Energy.

FN8 >5 GW reserved; Infinium and New Fortress Energy projects; Latin America expansion; Electric Hydrogen / GlobeNewswire.

FN9 45V credit up to $3/kg for 10 years; CFO Services; Taxpayers for Common Sense.

FN10 OBBB (July 2025) moved construction‑start deadline from 2033 to 2028; Senate two‑year reprieve; Gibson Dunn; H2 View. Notes: The federal incentive that animates the entire domestic green‑hydrogen thesis is Section 45V, the Clean Hydrogen Production Credit, which offers up to three dollars per kilogram on a four‑tiered scale keyed to lifecycle emissions intensity, with the maximum reserved for hydrogen produced at or below 0.45 kilograms of carbon‑dioxide equivalent per kilogram, and which runs for ten years once a facility is placed in service. The decisive policy event of the past year was the One Big Beautiful Bill Act, signed into law on the fourth of July 2025, which rewrote the Biden‑era clean‑energy credits wholesale. For hydrogen the headline was a curtailment: the deadline to begin construction was pulled forward from the start of 2033 to the start of 2028, so that only facilities breaking ground before the end of 2027 will qualify.

The more instructive observation, and the one that should temper any reflexive pessimism, is how mild that treatment was relative to the rest of the renewable complex. The House had initially moved to terminate 45V at the end of 2025; the Senate restored a two‑year reprieve that survived into the enacted text, and the credit’s value, its ten‑year term, and its direct‑pay and transferability features all emerged intact. Most consequentially, 45V was exempted from the restrictive foreign‑entity‑of‑concern rules that were newly imposed on the clean‑electricity and advanced‑manufacturing credits, even as the wind and solar investment and production credits were terminated for facilities placed in service after the end of 2027. In other words, under an administration committed to rolling back its predecessor’s energy agenda, hydrogen retained a fuller and less encumbered subsidy than the technologies around it, a relative outcome that several observers characterized as a quiet win for the industry. The strategic implication for EH2 and its customers is unambiguous: the value of the credit now accrues to whoever can break ground before 2028, which rewards exactly the deployment velocity that an integrated, manufactured, pre‑validated plant is designed to deliver.

FN11 45V exempt from foreign‑entity rules; wind and solar credits ended after 2027; Taxpayers for Common Sense; RSM US.

FN12 Ambient Fuels acquired May 2025; ~$400M Generate Capital finance; hydrogen‑as‑a‑service from 2026; Latitude Media; ESG Today. Notes: For most of its life EH2 was an equipment company, selling plants and declining to own molecules, a posture that kept its balance sheet asset‑light but left it hostage to the maturation of third‑party developers whose projects were slow to reach final investment decision. In May 2025 the company resolved that tension by acquiring Ambient Fuels, a New York hydrogen project developer, and pairing the acquisition with a strategic financing relationship with Generate Capital that brought roughly four hundred million dollars of project capital to the platform. The combination converts EH2 from a pure manufacturer into a full‑service developer and financier capable of offering hydrogen as a service, that is, selling the molecule as a process input to customers who would rather buy renewable hydrogen than build and operate their own plants, with project‑capital deployment targeted to begin in 2026. The strategic logic is the one First Solar’s alumni would recognize from photovoltaics: when a technology is still being proven at scale, the manufacturer must occasionally develop its own demand rather than wait for an arm’s‑length market that does not yet exist.

Growth from here therefore runs along three reinforcing tracks. The first is volume through the Devens gigafactory, monetizing the multi‑gigawatt reservation book across electrofuels, ammonia, refining, and steel. The second is the captive‑development track, in which EH2 and Ambient originate and finance projects that consume EH2 plants, capturing development and equity upside rather than a one‑time equipment margin. The third is geographic, with a recently announced expansion into Latin America aimed at green fertilizer and industrial decarbonization complementing the established United States base. Each track is calibrated to the same policy clock: the imperative to commence construction before the 2028 cliff turns deployment speed into the central commercial variable.

FN13 Data‑center demand ~450 to ~980 TWh; ~$7.65B of fuel‑cell deals; SOFCs mostly on natural gas; Data Center Knowledge; Boss Energy.

FN14 Microsoft testing hydrogen fuel‑cell backup; carbon‑negative by 2030; Introl. Notes: It is natural, given the energy hunger of artificial‑intelligence infrastructure, to ask whether EH2 sits in the path of the data‑center power boom, and here intellectual honesty is more valuable than enthusiasm. The demand backdrop is real: global data‑center electricity consumption, estimated near 450 terawatt‑hours in 2025, is projected to approach 980 by 2030, with United States data centers potentially reaching a double‑digit share of national demand and grid interconnection queues stretching from three to ten years. That speed gap has driven a remarkable wave of behind‑the‑meter fuel‑cell procurement, including a five‑billion‑dollar Bloom Energy and Brookfield framework, a Bloom and Oracle arrangement of up to 2.8 gigawatts, and gigawatt‑scale orders elsewhere, with one tally placing such commitments at 7.65 billion dollars between October 2025 and January 2026.

The critical qualifier is that EH2 does not make fuel cells, and the fuel cells presently winning data‑center contracts are predominantly solid‑oxide units running on natural gas rather than on green hydrogen. EH2’s exposure to the theme is therefore indirect and optional rather than contracted: it is the potential upstream supplier of the carbon‑free molecule that a hydrogen‑fueled fuel cell or turbine would consume, and its relevance scales only if and when behind‑the‑meter generation shifts from natural gas toward clean hydrogen. The thread is not purely speculative, since Microsoft, an EH2 investor, has publicly pursued hydrogen fuel‑cell backup for its facilities in service of a carbon‑negative‑by‑2030 commitment, which sketches a plausible, if still nascent, demand channel. The defensible conclusion for an investor is that the AI build‑out enlarges the long‑run addressable market for clean hydrogen and confers genuine option value on a low‑cost producer, but that it does not yet constitute a contracted revenue line for EH2, and the piece should be valued as optionality rather than as pipeline.