Photo by Jeremy Thomas on Unsplash

SpaceX’s IPO story pivots on a single, audacious idea: that the most efficient place to build the next generation of AI infrastructure is not on the desert floor of Arizona but in orbit, where sunlight is continuous, heat can be radiated into the void, and data can move across a laser-linked mesh that never touches a congested terrestrial grid. In the company’s own filings, it has already sought approval for up to one million orbital data‑center satellites, each a self‑contained stack of solar arrays, shielded accelerators, kilometer‑scale radiators, and optical crosslinks — a “data center that falls around the Earth,” as the report puts it.

The climate ledger is counterintuitive: while rockets inject black carbon into the stratosphere, the document notes that “a solar orbital facility could in principle emit roughly ten times less carbon than a gas-powered terrestrial one,” though scientists warn that launch and re‑entry effects could erode that advantage. The strategic bet is that if AI’s binding constraint is power rather than physics, then orbit — with its uninterrupted solar flux and freedom from land, water, and permitting battles — could become not just a technological frontier but a decarbonization one, shifting a slice of the world’s most energy‑hungry computation off the grid and into the sky.

This article is a SIDR research note. It is analytical and educational in nature and does not constitute investment, legal, or tax advice. Figures 1–4 are schematic and illustrative, not reported data — SpaceX publishes no audited Scope 1/2/3 inventory, and the emissions ranking in Figure 3 is a directional estimate only. IPO terms, dates, and index‑rule mechanics reflect press reporting as of 5 June 2026 and may change before or after pricing. Readers should conduct their own diligence and verify all assumptions independently. This note includes AI‑generated content. While every effort has been made to ensure accuracy, completeness, and clarity, AI‑assisted analysis may contain errors, omissions, or outdated information. Use with care and do not rely on this document as a sole source for financial or technical decision‑making.

SpaceX is scheduled to list on the Nasdaq on 12 June 2026 under the ticker SPCX, targeting a valuation near $1.75 trillion and a raise of roughly $75 billion — a debut that would dwarf Saudi Aramco’s 2019 record by more than 2.5×, making it the largest IPO ever attempted.FN1 The prospectus was filed confidentially on 1 April, refreshed publicly on 20 May, with a roadshow in early June and pricing the night of 11 June.FN2 The entity going public is no longer a launch company: following the February 2026 absorption of xAI, the group now spans rockets, the Starlink network, and the Grok AI franchise under the working “SpaceXAI” umbrella.FN3 For full-year 2025 it reported $18.7 billion of revenue (up 33%) and $6.6 billion of adjusted EBITDA, yet a $4.94 billion GAAP net loss — the gap driven by constellation depreciation, stock compensation, and an AI unit bleeding more than $6 billion in 2025 and another $2.5 billion in Q1 2026.FN4 The thesis of this note is that the company is best understood not as a transport business but as a vertically integrated utility for moving bits and electrons — and that the cleanest way to grasp both its history and its risks is to follow the institutional logic that built it.

The Anchor-Tenant Flywheel

Demand-pull procurement, not development subsidy

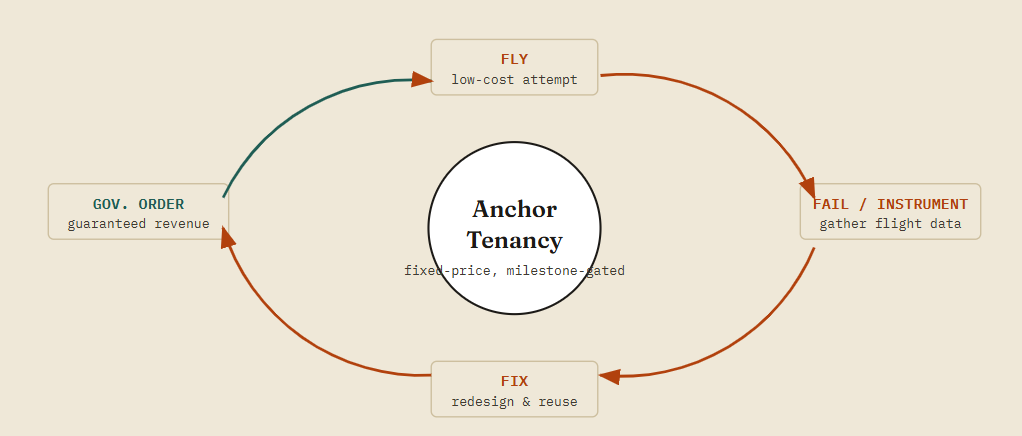

SpaceX did not grow because Washington paid it to invent rockets; it grew because Washington agreed to buy the ride once the rocket worked. This is the essence of anchor tenancy: under the COTS and Commercial Resupply Services framework, NASA committed to becoming a paying customer at fixed, milestone-gated prices, while leaving design risk, cost overruns, and intellectual property with the contractor.FN5 The contrast with cost-plus defense procurement is structural. Traditional acquisition reimburses effort and therefore quietly rewards delay; anchor tenancy pays only for delivered performance and therefore rewards iteration. A guaranteed future order book let SpaceX treat each Falcon as a data point rather than a catastrophe — fly, fail, instrument, fix, fly again — collapsing the feedback loop that legacy primes stretch across decades. The result is the cadence and reusability that turned a $60 million launch into a marginal-cost service. The same demand-pull pattern now recurs one layer up: the government is again the anchor tenant, this time for resilient bandwidth and sovereign compute rather than for tonnage to orbit.AnchorTenancyfixed-price, milestone-gatedFLYlow-cost attemptFAIL / INSTRUMENTgather flight dataFIXredesign & reuseGOV. ORDERguaranteed revenueFigure 1. The anchor-tenancy flywheel. Government revenue is contingent on delivered performance, which finances cheap, frequent attempts; each failure becomes instrumentation rather than ruin, compressing the engineering feedback loop that cost-plus contracting elongates.

Figure 1. The anchor-tenancy flywheel

Illustrative purpose only. Illustrations and explanatory schematics in this note are prepared by AI and SIDR, based on SIDR’s understanding of the underlying technologies. They are for illustrative and educational purposes only and do not represent reported data or engineering specifications. Government revenue is contingent on delivered performance, which finances cheap, frequent attempts; each failure becomes instrumentation rather than ruin, compressing the engineering feedback loop that cost-plus contracting elongates. This note includes AI‑generated content. While every effort has been made to ensure accuracy, completeness, and clarity, AI‑assisted analysis may contain errors, omissions, or outdated information. Use with care and do not rely on this document as a sole source for financial or technical decision‑making. Readers should conduct their own diligence and verify all assumptions independently.

Four Segments, One Cash Engine

Launch, Connectivity, Defense, and the loss-making AI option

The group decomposes into four businesses of very different maturity. Launch Services is the legacy cash cow and the enabling moat — owning the cheapest road to orbit lets every other segment underprice rivals who must buy rides. Starlink / Connectivity is now the revenue engine: a proliferated low-Earth-orbit mesh that, crucially, sells not only consumer broadband but its own optical hardware — SpaceX has begun marketing its “mini laser” inter-satellite terminals to competitors, offering up to 25 Gbps across 4,000 km, turning a cost center into an arms supplier for the entire LEO economy.FN6 Defense and Intelligence monetizes the same constellation as sovereign infrastructure. The fourth segment — AI / compute, inherited from xAI — is deeply unprofitable today yet is the reason the equity carries a software multiple rather than an aerospace one. The strategic wager is that artificial intelligence and orbit are complements: in the right sun-synchronous orbit a solar panel is up to eight times more productive than on the ground and generates power almost continuously, the vacuum offers a near-infinite radiative heat sink, and co-locating inference with Earth-observation sensors removes the downlink bottleneck.FN7 The catch is latency and serviceability — orbital compute suits training, batch inference, and sensor-adjacent edge work, not latency-critical transactional loads — which is why the segment is an option on the next decade rather than a 2026 earner.

SpaceX is no longer selling rockets; it is selling the two scarcest inputs of the AI era — cheap photons and unobstructed bandwidth — and the rocket is merely the delivery truck.

Dual-Use by Design

Why proliferated LEO became a deterrence asset

A constellation of thousands of cheap, rapidly replaceable satellites is, from a war-planner’s perspective, almost ideal: there is no single node whose destruction collapses the system, and replacement launch capacity is captive and continuous. That makes proliferated LEO the connective tissue of modern ISR (intelligence, surveillance, reconnaissance) and of resilient command-and-control in contested or denied environments, where the alternative — a handful of exquisite, geostationary, jam-prone assets — is a liability. Recent conflict has supplied the empirical proof of concept that battlefield connectivity can be sustained even under sustained electronic attack, and governments have drawn the obvious lesson: redundancy and proliferation are now treated as forms of deterrence in their own right. The same optical-crosslink mesh that routes a consumer’s video call also routes targeting data, which is precisely why the IPO is as much a national-security event as a financial one — and why the state remains the anchor tenant of the next chapter.

The Data Center That Falls Around the Earth

The core question — engineering, economics, and existential risk

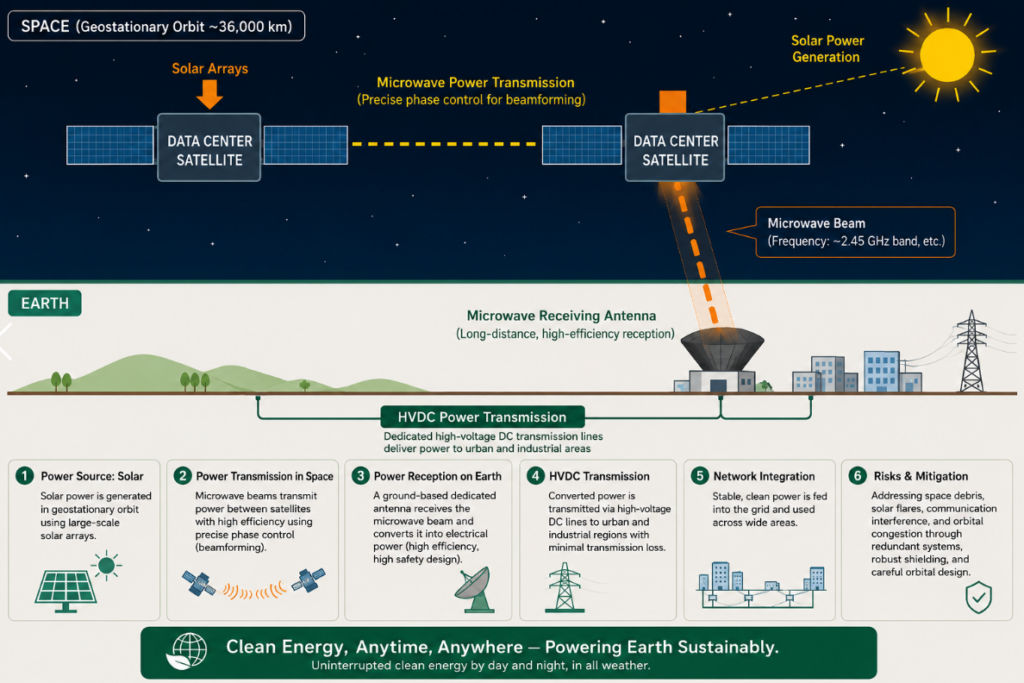

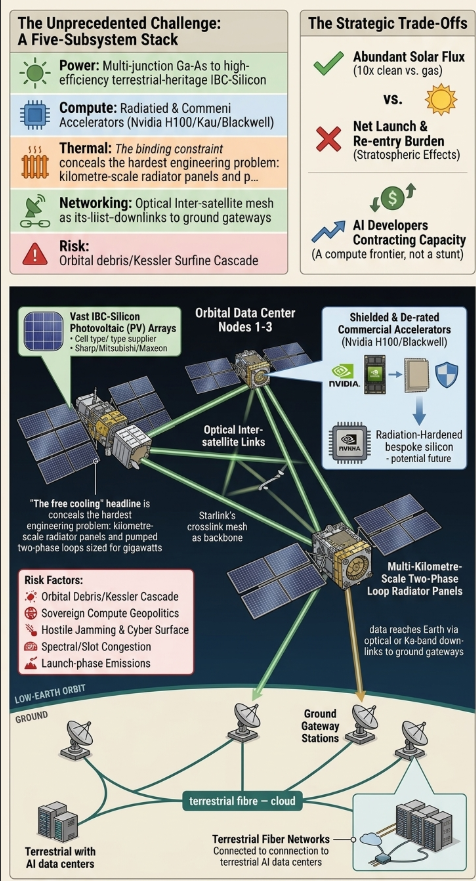

The boldest claim embedded in the valuation is that the most efficient place to build the next generation of AI infrastructure is not Arizona but orbit. The architecture is now concrete rather than speculative. SpaceX has filed with the FCC for authority to deploy up to one million data-center satellites, and Musk has stated plainly that the company “will be doing data centers in space” by scaling the next Starlink bus into a compute platform.FN8 It is not alone: Google’s Project Suncatcher will fly two solar-powered prototypes carrying radiation-tested Trillium TPUs into ~640 km low-Earth orbit by early 2027, having already demonstrated 1.6 Tbps over a single optical link in the lab; the Nvidia-backed startup Starcloud trained the first AI model in orbit in late 2025 and plans a 5-gigawatt orbital “hypercluster” fed by a solar array four kilometres on a side.FN9 A working orbital data center is a stack of five subsystems, each with a distinct supply chain and a distinct failure mode:

- Power. Vast deployable photovoltaic arrays in continuous sunlight. Incumbent space cells are III–V multi-junction (gallium-arsenide) parts from a narrow supplier base — SolAero/Rocket Lab (US), Azur Space (Germany), CESI (Italy) — but at constellation scale the economics push toward high-efficiency terrestrial-heritage silicon and space-qualified Japanese makers such as Sharp and Mitsubishi Electric, with IBC-silicon players like Maxeon as cost-down candidates.FN10

- Compute. Radiation-hardened or radiation-tolerant accelerators with fault-tolerant, checkpoint-heavy software; early flights carry commercial Nvidia H100/Blackwell parts shielded and de-rated rather than bespoke rad-hard silicon.FN9

- Thermal. In vacuum there is no convection — heat leaves only by radiation. The “free cooling” headline conceals the hardest engineering problem: kilometre-scale radiator panels and pumped two-phase loops sized for gigawatts.

- Networking. Optical inter-satellite links knit the cluster into a mesh; data reaches Earth via optical or Ka-band downlinks to ground gateways, then onto terrestrial fibre. Starlink’s own crosslink mesh is positioned as the relay backbone.FN6

- Risk. Orbital debris and the tail risk of Kessler-syndrome cascade; spectrum and orbital-slot congestion; a hostile-jamming and cyber attack surface; launch-phase emissions; and the geopolitics of parking sovereign compute above other nations’ territory.

The opportunity is real — abundant solar flux, a global footprint, and strategic autonomy from terrestrial grids and permitting fights of the kind now dogging gigawatt data centers on the ground. So is the catch. Scientific American’s reporting notes that while a solar orbital facility could in principle emit roughly ten times less carbon than a gas-powered terrestrial one, independent atmospheric scientists warn the launch and re-entry burden could leave the orbital option worse on net once stratospheric effects are counted.FN11 The signal worth watching is demand: AI developers have already begun contracting orbital capacity as a hedge against terrestrial power constraints, an early sign the market is pricing space as a compute frontier rather than a stunt.FN12GPU /TPUradiatorGPU /TPUoptical inter-satellite linkoptical / Ka downlinkground gatewayterrestrial fibre · cloudLOW-EARTH ORBITGROUNDFigure 2. A schematic orbital data center. Continuous-sunlight PV arrays feed shielded accelerators; waste heat is rejected only by radiation (the binding constraint); optical crosslinks form the cluster mesh; data returns to Earth via optical/Ka downlinks to ground gateways and onward to terrestrial fibre. Illustrative, not to scale.

Figure 2. A schematic orbital data center

Illustrative purpose only. Illustrations and explanatory schematics in this note are prepared by AI and SIDR, based on SIDR’s understanding of the underlying technologies. They are for illustrative and educational purposes only and do not represent reported data or engineering specifications. Continuous-sunlight PV arrays feed shielded accelerators; waste heat is rejected only by radiation (the binding constraint); optical crosslinks form the cluster mesh; data returns to Earth via optical/Ka downlinks to ground gateways and onward to terrestrial fibre. Illustrative, not to scale. This note includes AI‑generated content. While every effort has been made to ensure accuracy, completeness, and clarity, AI‑assisted analysis may contain errors, omissions, or outdated information. Use with care and do not rely on this document as a sole source for financial or technical decision‑making. Readers should conduct their own diligence and verify all assumptions independently.

Who Sells the Picks and Shovels

Second-order beneficiaries of the capital build-out

An IPO of this size is a capital-formation event for an entire supply chain, but the linkages must be drawn honestly — the bird flies on free-space optics, so there is no fibre in orbit, and several “obvious” names are really terrestrial-network plays. Corning benefits less from the satellites than from the ground: gateway backhaul and the explosion of intra-data-center optical fibre and specialty glass that the AI compute build-out demands. Fujikura sits adjacent as a photonic-component, connector, and fusion-splicing supplier to the ground and data-center layer, with optional exposure to laser-terminal optics. NTT is the most interesting Japanese case: through its Space Compass joint venture with Sky Perfect JSAT it is itself pursuing optical data-relay and space-based computing, so it is part-competitor, part-beneficiary, and a natural backbone partner for downlinked traffic.FN13 Beyond the named three, the cleaner exposures are the laser-terminal specialists (Mynaric, Tesat-Spacecom), optical ground-station makers (Cailabs), the space-PV bench (SolAero/Rocket Lab, Azur Space, CESI, plus Sharp and Mitsubishi Electric), Nvidia as the orbital silicon of record, KDDI as Japan’s Starlink retail partner, and — not least — the five lead underwriters (Morgan Stanley, Goldman Sachs, JPMorgan, Bank of America, Citigroup) splitting the richest fee pool in the history of equity capital markets.FN14 The investment logic is uniform: own the inputs that are scarce and standardised — photons, optics, and qualified silicon — rather than the constellation that commoditises everything downstream of them.

The Plumbing Problem

Why a 100% primary deal still distorts the whole market

Here the popular narrative is wrong in an instructive way. The offering is structured as essentially all primary — the company raises roughly $74–75 billion of fresh capital — and Musk is bound by a 366-day lockup.FN15 So this is not “Musk dumps Tesla to fund SpaceX.” The real mechanism is two-fold. First, active rotation: to free cash for a marquee allocation, institutions trim their most crowded, most correlated “Musk-premium” position — Tesla — and, more broadly, sell slices of whatever they hold, which for most portfolios means the mega-cap leadership of the S&P 500 and Nasdaq-100. Your hypothesis is correct: large IPOs do reliably pull liquidity out of the broad indices as managers raise dry powder, producing a transient, mechanical drag on exactly the names that dominate those benchmarks. Second, and larger, is passive forced buying into a tiny float. SpaceX will float only an estimated 3–5% of shares, yet index providers have rewritten their rulebooks to admit it fast: Nasdaq’s “Fast Entry” adds it after ~15 trading days and scrapped its low-float minimum, FTSE Russell cut its window to five days, MSCI to ten, and S&P Dow Jones was set to rule on accelerated entry on 8 June.FN16 When trillions of benchmarked dollars must buy a 3% float on a fixed date, every existing constituent — Apple, Microsoft, Nvidia, and yes, Tesla — is sold pro-rata to fund the purchase. Bloomberg Intelligence pegs Nasdaq-100 tracker demand alone near $5 billion, with cross-index estimates of $15–30 billion of conservative forced buying, and far more under float-multiplier weighting.FN17 The Nikkei 225 is not a direct channel — SPCX is a US listing and cannot enter a Japanese-equity index — but the second-order effect is real: Japanese institutions rebalancing toward a must-own US mega-cap, and global funds rotating into the offering, can drain marginal bids from Tokyo just as they do from New York. The clean takeaway: a low-float, all-primary mega-IPO meeting a wall of rule-accelerated passive demand is a textbook supply-demand distortion, and the staggered insider-lockup releases that begin after the first earnings report are what will quietly resolve it — with retail as the exit liquidity.FN18

The Carbon Ledger, Counter-Intuitively Read

Scope 1, 2, 3 — and why the rocket is not the villain

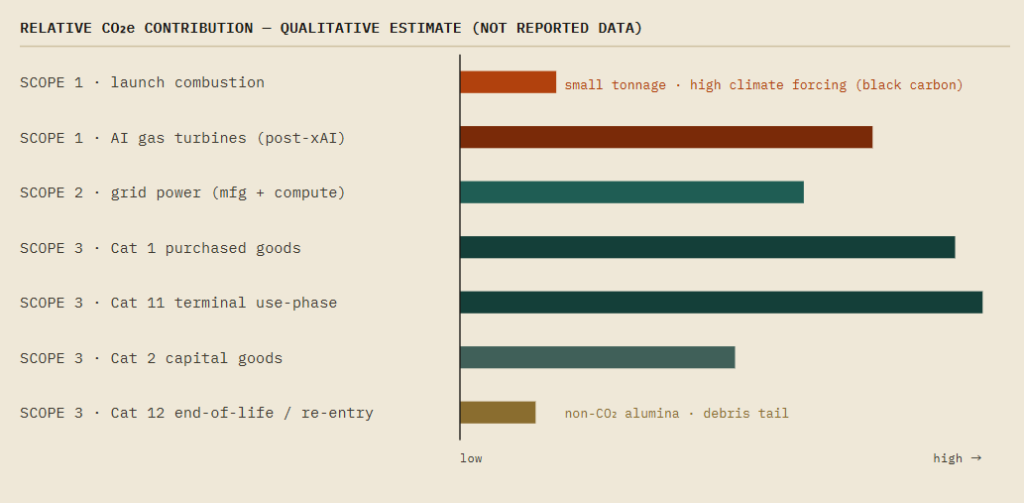

SpaceX publishes no audited greenhouse-gas inventory, so what follows is a reasoned forward estimate, not reported data. The intuition that Scope 1 rocketry dominates is half right and half misleading. The propellants first: Falcon 9 and Heavy burn RP-1, a refined kerosene, with liquid oxygen — roughly 50,000 gallons of kerosene and on the order of ~387 tonnes CO₂e per Falcon flight, plus at least several tonnes of black carbon; Starship burns liquid methane (“methalox”), not hydrogen, at roughly 3,491 tonnes CO₂e per launch.FN19 (For the record, SpaceX uses no hydrogen; the LH₂/LOX engines belong to vehicles like NASA’s SLS and Japan’s H3 — the latter a JAXA/Mitsubishi rocket, not a SpaceX fuel.FN20) In raw tonnage these launch emissions are tiny next to commercial aviation. Their danger is qualitative: black carbon injected directly into the stratosphere has roughly 500× the radiative forcing per unit mass of surface soot, lingers for years, and erodes the ozone layer — so the rocket punches far above its weight on climate even as it under-weighs in the CO₂e ledger.FN21 The genuinely large buckets lie elsewhere. Post-merger, the single biggest combustion source may not be a rocket at all but the on-site natural-gas turbines powering the xAI “Colossus” supercomplex in Memphis — a fleet that drew a Clean Air Act suit and is scaling past a gigawatt — a terrestrial Scope 1 line that can dwarf the launch manifest.FN22

Scope 2 (purchased grid power for satellite and terminal manufacturing, test stands, and the compute that is not self-generated) is large and compounding. But the centre of gravity is Scope 3: Category 1 (purchased goods — satellites, GPUs and HBM, aluminium-lithium, batteries, propellant feedstock) and Category 11 (use of sold products — millions of Starlink user terminals each drawing tens of watts continuously, an aggregate of multiple terawatt-hours a year) are the most plausible largest categories, with Category 2 (capital goods: gigafactories, pads, data halls) close behind and Category 12 (end-of-life: satellite re-entry depositing alumina in the upper atmosphere) a distinctive, non-CO₂ tail. The investable conclusion for an ESG-screened reader is contrarian: the launch flame is the most photogenic emission and the most climate-potent per kilogram, but the company’s true footprint is an electronics-and-electrons footprint — manufacturing and use-phase power — and it grows with subscribers and GPUs, not with rocket cadence.

Figure 3. Estimated Relative CO₂e Contributions Across SpaceX’s Value Chain

SIDR’s qualitative ranking of the combined entity’s emissions. The launch flame (top, rust) is climate-potent but small in tonnage; the dominant CO₂e likely sits in Scope 3 manufacturing (Cat 1) and terminal use-phase (Cat 11), with terrestrial AI power (gas turbines + grid) now a major line. Directional analysis only; no audited figures exist.

Read together, the seven threads tell one story. A government willing to be a customer rather than a paymaster built a launch monopoly; the launch monopoly built a bandwidth utility; the bandwidth utility is metastasising into a compute utility that wants to migrate to orbit; and the financial event that funds the next leg will, through the unglamorous mechanics of index inclusion and a 3% float, briefly reorder the world’s largest stock indices. The valuation asks investors to underwrite all of it at once. Whether $1.75 trillion is visionary or vertiginous depends on a single question the prospectus cannot answer: in the AI decade, is the binding constraint power, or is it physics? SpaceX is betting it is power — and that the cheapest power is in the sky.

Figure 4. Comprehensive Global Orbital Data Center Ecosystem.

Illustrative purpose only. Illustrations and explanatory schematics in this note are prepared by AI and SIDR, based on SIDR’s understanding of the underlying technologies. They are for illustrative and educational purposes only and do not represent reported data or engineering specifications. A breakdown of the five critical subsystems (Power, Compute, Thermal, Networking, Risk) and the broader strategic context, detailing the transition from rad-hard to shielded silicon and the multi-kilometre-scale radiator challenge. Illustrative and not to scale. Use with care and do not rely on this document as a sole source for financial or technical decision‑making. Readers should conduct their own diligence and verify all assumptions independently.

References

- Bloomberg, “What to Know About the SpaceX IPO” (3 Jun 2026); CryptoBriefing, “SpaceX targets mid-June 2026 IPO at $1.75 trillion valuation” (Jun 2026). — IPO date, ticker, valuation, raise.

- Trending Topics, “SpaceX Sets June 12 Date for Largest IPO in History” (May 2026); InvestmentNews (May 2026). — S-1 filing 1 Apr, prospectus 20 May, roadshow, pricing 11 Jun.

- Trending Topics (May 2026); Tom’s Hardware, “SpaceX acquires xAI…” (2026). — Feb 2026 xAI merger; Grok / “SpaceXAI.”

- BitMEX, “SpaceX IPO Guide: S-1 Breakdown” (May 2026); SpotGamma (May 2026). — 2025 revenue $18.7B, adj. EBITDA $6.6B, GAAP loss $4.94B; AI losses; Q1-26 GAAP loss.

- NASA, Commercial Orbital Transportation Services (COTS) & Commercial Resupply Services program documentation. — Anchor-tenancy / milestone-based procurement.

- Reuters/AOL, “SpaceX to sell satellite laser links…” (2024); SpaceNews, “Starlink mini lasers to link Muon Space satellites” (Oct 2025); satsearch ISL terminal catalogue (2025). — 25 Gbps / 4,000 km optical terminals.

- Fierce Network, “Space data centers: Starcloud, SpaceX and Project Suncatcher explained” (Mar 2026). — ~8× solar productivity; near-continuous power; orbital-compute rationale.

- GeekWire (Apr 2026); The Conversation / Yahoo, “Data centers in space” (2026). — SpaceX FCC filing for up to 1M data-center satellites; Musk statement.

- Introl, “Orbital Data Center Race 2026” (Feb 2026); CNBC, “Nvidia-backed Starcloud trains first AI model in space” (Dec 2025); Scientific American (Dec 2025). — Suncatcher TPUs / 1.6 Tbps / 2027 prototypes; Starcloud H100/Blackwell, 5 GW array, 88k-sat filing.

- Industry supply-base analysis: space III–V multi-junction PV (SolAero/Rocket Lab, Azur Space, CESI); Japanese space-cell heritage (Sharp, Mitsubishi Electric); IBC silicon (Maxeon). — SIDR synthesis.

- Scientific American, “Space-Based Data Centers Could Power AI with Solar Energy — At a Cost” (Dec 2025). — ~10× lower carbon vs. gas DC, but possible net-worse with launch/re-entry.

- DataCenterDynamics (May 2026). — AI developers contracting SpaceX/Colossus compute; stated interest in multi-GW orbital AI capacity.

- Space Compass (NTT × Sky Perfect JSAT) corporate disclosures on optical data relay and space-based computing. — NTT competitor/beneficiary positioning.

- MEXC/crypto.news, “Project Apex” (Apr 2026). — Lead underwriters (Morgan Stanley, Goldman Sachs, JPMorgan, BofA, Citi); 21-bank syndicate.

- InvestmentNews (May 2026); Motley Fool, “You Are the Exit Liquidity for the SpaceX IPO” (4 Jun 2026). — All-primary ≈$74–75B; staggered lockup; Musk 366-day restriction.

- InvestmentNews; ETF Stream, “Investors and ETF issuers react to index impact” (5 Jun 2026); SpotGamma (May 2026). — Float 3–5%; Nasdaq Fast Entry (15 days), FTSE Russell (5), MSCI (10), S&P consultation (8 Jun).

- ETF Stream (Jun 2026); Yahoo Finance / Motley Fool (May–Jun 2026). — Bloomberg Intelligence ~$5B Nasdaq-100 demand; $15–30B cross-index forced buying.

- SpotGamma, “SpaceX IPO Index Inclusion” (May 2026); Motley Fool (Jun 2026). — Pro-rata constituent selling to fund inclusion; insider exit liquidity.

- Undark (Apr 2026); GreenLaunch emissions comparison (Apr 2026); FAA launch estimates. — Falcon 9 ~387 t CO₂e & black carbon; Starship methalox ~3,491 t CO₂e.

- Payload, “The Space Industry’s Climate Impact” (2023/24). — Propellant taxonomy; LH₂ confined to SLS-class & H3 (JAXA/Mitsubishi).

- Ryan et al., “Impact of Rocket Launch and Space Debris…,”Earth’s Future(2022); Yale E360, “Scientists Warn of Emissions Risks from the Surge in Satellites.” — Black-carbon ~500× radiative forcing; stratospheric persistence; ozone effects.

- TechCrunch (Jun & Nov 2025); Global Energy Monitor, “Colossus 1 power station” (Jan 2026); SemiAnalysis (Oct 2025). — xAI Memphis gas-turbine fleet; Clean Air Act suit; >1 GW scaling.