Photo by Dan Meyers on Unsplash

Our Tennessee–Alabama report tracked a $40 billion bet on small modular reactors inside one US grid. This is the view from everywhere else — the Japanese house leading the Western field, and the Chinese, French and Russian programmes racing it — scored against the Department of Energy’s 17-dimension Adoption Readiness Level framework.

Adecade of slideware is finally turning into rebar and reactor pressure vessels, and the company furthest along in the Western world is Japanese. Through its joint ventures with GE Vernova — the US-domiciled GE Vernova Hitachi Nuclear Energy (GVH) and the Japan-domiciled Hitachi GE Vernova Nuclear Energy — Hitachi co-owns the BWRX-300, a 300-MWe water-cooled boiling-water reactor that uses natural circulation and fully passive safety systems, and that borrows its licensing spine from the US NRC-certified ESBWR design and the already-licensed GNF2 fuel.FN1FN2 That inheritance is the whole strategy: rather than invent a reactor, Hitachi and GE Vernova shrank a certified one, which is why the BWRX-300 is being poured in concrete while most rivals are still drawing.

The lead project sits in Canada, where Ontario Power Generation is building the first of four BWRX-300 units at the Darlington New Nuclear Project — on track to be the first SMR in any G7 country. The Canadian Nuclear Safety Commission cleared the first regulatory hold point, for the reactor-building foundation, on 30 March 2026, and OPG filed for a 20-year operating licence days earlier, with the first unit targeted for service by the end of 2030 inside a roughly CAD 20.9 billion four-unit programme.FN3FN4 The same design is queued across at least four more jurisdictions: the Tennessee Valley Authority’s Clinch River site in Oak Ridge, where the NRC is reviewing a construction-permit application; Poland, where Orlen Synthos Green Energy signed a generic-design agreement in February 2026; Finland and Sweden via Fortum and a Vattenfall-backed consortium weighing five BWRX-300s at Ringhals; and Southeast Asia, where GE Vernova and Hitachi signed an exploratory memorandum in Tokyo in March 2026 that explicitly aims to fold qualified Japanese suppliers into the BWRX-300 supply chain.FN1FN5

Hitachi is not Japan’s only entrant. Mitsubishi Heavy Industries carries a broader, earlier-stage portfolio: a 300-MWe integrated small pressurized-water reactor with passive safety, a 1-MW truck-transportable micro-reactor, and a high-temperature gas-cooled reactor for which Japan’s Agency for Natural Resources and Energy named MHI the core company, targeting a demonstration unit in the 2030s and hydrogen production via the Japan Atomic Energy Agency’s High-Temperature Test Reactor at Oarai.FN6 MHI also leads a demonstration sodium-cooled fast reactor with Mitsubishi FBR Systems and has a cooperation memorandum with TerraPower — but unlike the BWRX-300, none of these has firm utility orders or a construction licence, making them a domestic, policy-driven pipeline rather than a deployment.FN7

China may reach the finish line first on a different track. China National Nuclear Corporation’s 125-MWe ACP100, branded Linglong One, is in final commissioning at the Changjiang site on Hainan and is targeted for grid connection in the first half of 2026 — which, if it holds, makes it the world’s first land-based commercial SMR, ahead of every Western project.FN8 The integral PWR was the first SMR to clear an IAEA generic reactor safety review back in 2016, is co-sited with existing reactors to share grid and cooling infrastructure, and is backed with full domestic intellectual-property rights and Belt-and-Road export ambitions under China’s latest five-year plan.FN8

France is the cautionary tale. EDF’s Nuward programme, launched in 2019 with the CEA, Naval Group and TechnicAtome, abandoned its bespoke integrated design in 2024 after utility customers balked at cost and complexity, withdrew from the UK’s SMR contest, and relaunched around a simpler ~400-MWe plant built from proven PWR building blocks, with a conceptual design due to be finalized by mid-2026 and a first-of-a-kind unit in France aimed at the 2030s.FN9 A six-nation early regulatory review gives Nuward licensing groundwork, but with no construction licence and no firm orders it remains the least mature of the major contenders.

Russia, by contrast, leans on the most operational heritage of all. Rosatom’s land-based RITM-200N — a 55-MWe unit adapted by OKBM Afrikantov from the marine RITM-200 reactors that already power its nuclear icebreaker fleet, with the floating Akademik Lomonosov plant in service since 2019 — is under construction near Ust-Kuyga in Yakutia, with commissioning targeted for 2028 and a possible expansion to two units, while a 2024 contract commits six RITM-200N reactors (about 330 MWe) to Uzbekistan’s Jizzakh region.FN10 The serial manufacturing base is real; the constraint is geopolitical, with sanctions and export politics walling Rosatom out of most Western markets.

This is where the Adoption Readiness Level framework earns its place. Technology Readiness Levels tell you whether a reactor works; the DOE’s ARL framework, with its 17 risk dimensions across Value Proposition, Market Acceptance, Resource Maturity and License to Operate, tells you whether it can actually be financed, built, supplied, permitted and accepted at scale — the questions that have killed more SMR programmes than physics ever has.FN11 Scored that way, Hitachi’s BWRX-300 and CNNC’s Linglong One lead on adoption, Rosatom trades market reach for manufacturing depth, MHI and EDF Nuward sit further back on the commercialization curve. The full dimension-by-dimension read follows.

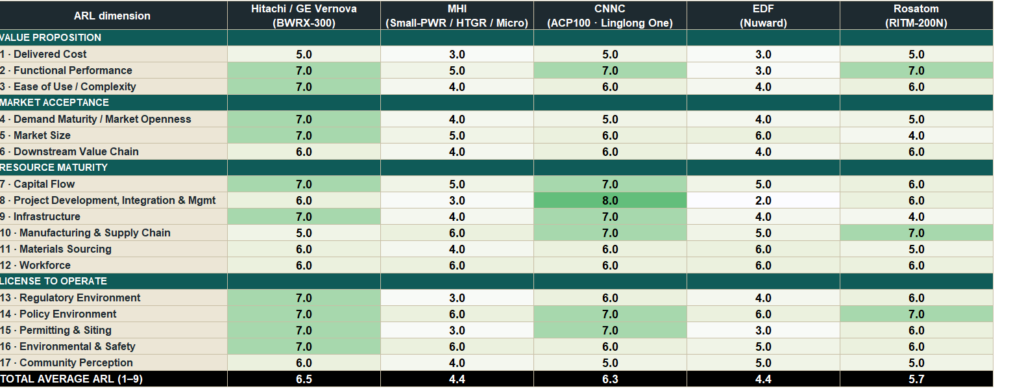

ARL Analysis Across Five SMR Developers

Analysis prepared by AI and SIDR. This comparative ARL assessment summarizes how five SMR developers perform across 17 dimensions spanning value proposition, market acceptance, resource maturity, and license to operate. Scores reflect relative adoption readiness rather than technical merit alone, highlighting which designs are positioned to be financed, licensed, supplied, and built at scale. AI‑generated content may contain inaccuracies and should be reviewed with appropriate expert judgment.

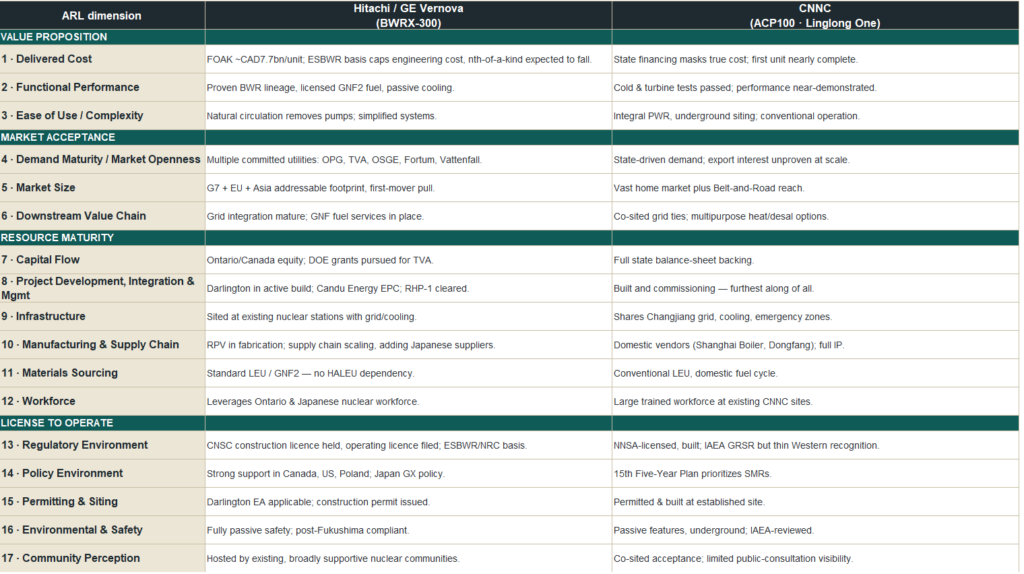

Analysis of BWRX‑300 and Linglong One Across ARL Dimensions

Analysis prepared by AI and SIDR. This comparison summarizes how the BWRX‑300 and Linglong One perform across 17 Adoption Readiness Level dimensions, covering value proposition, market acceptance, resource maturity, and license to operate. The assessment highlights differences in cost structure, regulatory inheritance, supply‑chain depth, and project execution, illustrating why each design occupies a distinct position on the commercialization curve. AI‑generated content may contain inaccuracies and should be reviewed with appropriate expert judgment.

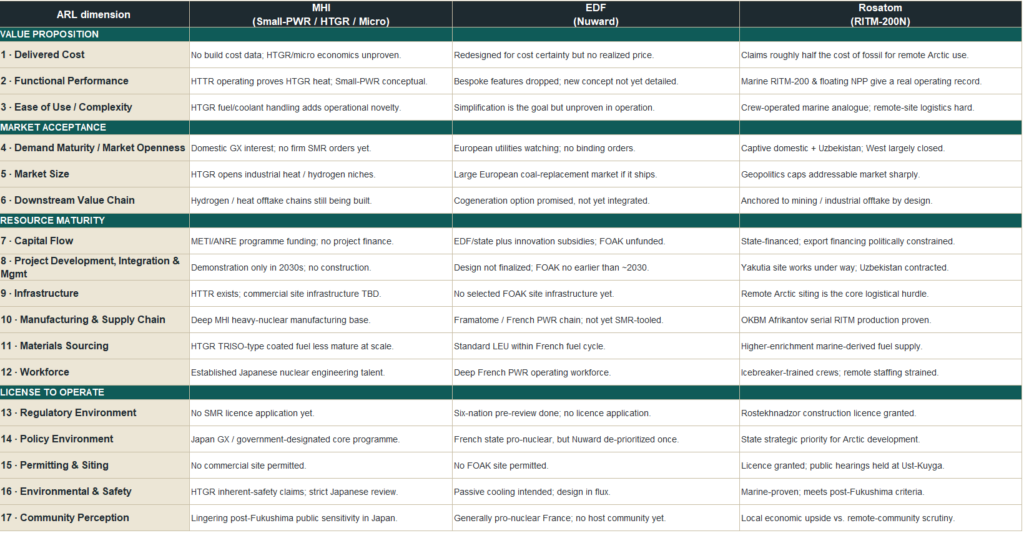

Analysis of MHI, EDF, and Rosatom Across ARL Dimensions

Analysis prepared by AI and SIDR. This comparative assessment examines how MHI, EDF, and Rosatom perform across 17 Adoption Readiness Level dimensions, spanning value proposition, market acceptance, resource maturity, and license to operate. The analysis highlights contrasting trajectories — from Japan’s policy‑driven prototypes and France’s redesign phase to Russia’s operational heritage constrained by geopolitics — illustrating how industrial depth and regulatory momentum shape readiness more than reactor physics. AI‑generated content may contain inaccuracies and should be reviewed with appropriate expert judgment.

Conclusions

What the ARL results reveal is deceptively simple: success in small modular reactors no longer hinges on physics but on execution. The leaders are those that can be financed, licensed, supplied, and built at scale — not those with the most sophisticated neutronics. Hitachi and GE Vernova’s BWRX‑300 and CNNC’s Linglong One stand out because they combine proven technology with credible delivery systems, while others remain trapped in design or policy cycles. In this light, the first deployable SMRs are already visible, shaped less by scientific novelty than by regulatory inheritance, manufacturing depth, and the ability to turn paperwork into power plants.

References

- GE Vernova & Hitachi, “GE Vernova and Hitachi to explore deployment of BWRX‑300 small modular reactor in Southeast Asia” (MoU signed in Tokyo, 14 Mar 2026).

- GE Vernova Hitachi Nuclear Energy, “BWRX‑300 Small Modular Reactor” product & milestones page (AFRY Main Services Agreement, 7 Apr 2026; Orlen Synthos Green Energy generic‑design agreement, 24 Feb 2026; Fortum early‑works agreement, 1 Jul 2025).

- Canadian Nuclear Safety Commission, “Darlington New Nuclear Project” (operating‑licence application 25 Mar 2026; RHP‑1 removed 30 Mar 2026); World Nuclear News, “OPG applies for operating licence for BWRX‑300 SMR” (2 Apr 2026).

- Ontario Power Generation, Darlington SMR programme (four‑unit, ~CAD20.9bn; first unit by end‑2030); World Nuclear News, “Canada’s first SMR project: how is CAD20.9 billion cost calculated?” (23 May 2025).

- World Nuclear News, “GE Vernova Hitachi, AFRY to collaborate on SMR deployment” (8 Apr 2026), including Vattenfall/Industrikraft Ringhals (Värö) state‑aid application for five BWRX‑300s.

- World Nuclear News, “MHI to lead development of Japanese HTGR” (ANRE core‑company selection; demo unit in the 2030s; HTTR hydrogen with JAEA at Oarai).

- World Nuclear News, “Nuclear power remains key sector for MHI” (300‑MWe integrated Small‑PWR, HTGR for hydrogen, 1‑MW micro‑reactor, sodium‑cooled fast reactor with Mitsubishi FBR Systems, TerraPower MoU).

- World Nuclear Association, “Nuclear Power in China” (ACP100/Linglong One status, updated 24 Apr 2026); World Nuclear News, “Chinese SMR completes non‑nuclear steam start‑up test” (8 Jan 2026); CNNC targeting grid connection H1 2026; IAEA Generic Reactor Safety Review, 2016.

- World Nuclear News, “EDF simplifies Nuward SMR design” (7 Jan 2025) and “Second phase of Nuward review completed” (9 Dec 2025): redesigned ~400‑MWe plant, conceptual design due mid‑2026, FOAK in France in the 2030s.

- World Nuclear News, “Licence issued for Russia’s first land‑based SMR” (Apr 2023) and “SMR planned for Yakutia may become two‑unit project”; Nuclear Engineering International, “Russia progresses with first land‑based SMR” (30 Mar 2025); Uzbekistan Jizzakh contract for six RITM‑200N units (~330 MWe), 27 May 2024.

- U.S. Department of Energy, Office of Technology Commercialization, “Adoption Readiness Levels (ARL) Framework” and “Core Risk Areas” (17 dimensions across Value Proposition, Market Acceptance, Resource Maturity, License to Operate; 1–9 score).