Photo by Aryo Yarahmadi on Unsplash

A 141-year-old cable maker posted the best numbers in its history and was promptly cut in two. The reason it was punished is, paradoxically, the best evidence that the demand is real — and it has a name: hydrogen. Here is how Fujikura intends to win it back.

On 14 May 2026, Fujikura reported a year that ought to have been a coronation: revenue past ¥1 trillion for the first time in its history, up roughly a fifth, with net profit up about 72% — every line at a record, the information-and-telecommunications segment alone supplying more than four-fifths of operating profit on the back of an explosion in North American AI data-centre demand.FN1 The market’s response was to sell it limit-down and keep selling: in a single week some ¥6 trillion of market value evaporated and the shares nearly halved from the all-time high they had set the day before — an episode now christened the “Fujikura Shock.” The paradox dissolves once one accepts that Fujikura is no longer a wire-and-cable company in the market’s mind but an AI-infrastructure growth stock priced near sixty times earnings, and at that altitude the only number that matters is next year’s guidance against a stratospheric bar. Management guided revenue up a mere 5% and, after the roll-off of one-off securities gains that had flattered the prior year, net profit fractionally down — and the algorithms, reading “growth has stalled,” did the rest.FN1

To see why this was a misreading, one has to understand what Fujikura actually sells and why the AI build-out cannot proceed without it. Generative AI triggered a global rush to build hyperscale data centres; the first winners were the makers of GPUs, but capital quickly flowed downstream to the unglamorous systems that let a data centre run — power, cooling, and above all the optical fibre that is the aorta of the entire apparatus, moving vast volumes of data between servers and between buildings at low latency. Fujikura’s edge rests on two products. The first is its proprietary high-density cable architecture — Spider Web Ribbon (SWR®) intermittently-bonded fibre wrapped into its Wrapping Tube Cable (WTC®) — which threads an extraordinary count of fibres, as many as 13,000, into a fraction of the usual diameter; the second is its near-dominant global position in the fusion splicers that join those fibres in the field.FN2 This is decisive because the ducts beneath data centres are already saturated, so the operative question for hyperscalers is no longer cost but how many fibres can be forced through a fixed cross-section — a contest Fujikura wins so consistently that its cable is bought by name as the de facto standard. The demand behind it is concrete and structural, not a sentiment trade: the telecom segment grew about 45%, the U.S. government selected Fujikura in late 2025 to supply up to $20 billion of fibre for American AI infrastructure, and the new medium-term plan stakes roughly 90% of its 2028 operating-profit target on this single business — a bet so total the company calls the coming era its “Fourth Founding.”FN2

You do not run short of hydrogen unless you are straining to ship every metre of cable the world will buy.

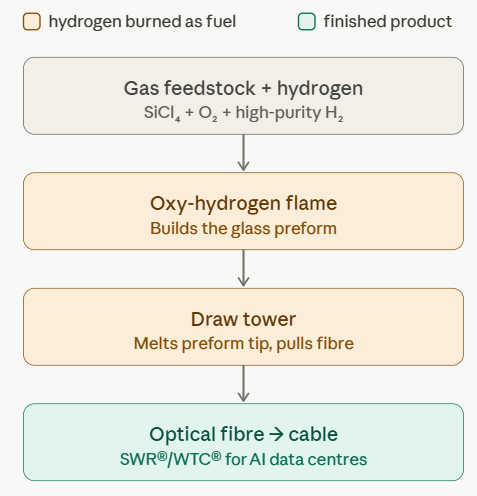

Illustration of Hydrogen’s Role in Optical Fiber Manufacturing

Illustration prepared by AI and SIDR. AI‑generated content may contain inaccuracies; please review with appropriate expert judgment. High‑purity hydrogen (≥99.999%) is used as a flame fuel in preform synthesis and fiber drawing, and is fully consumed during combustion rather than incorporated into the optical fiber itself. Precise flame‑temperature control is essential to prevent optical loss, making certified high‑purity hydrogen a critical input. Demand from semiconductor fabrication and the broader energy transition competes for the same grade of hydrogen, contributing to structural tightness in supply.

Which returns us to the guidance, and to the genuinely interesting disclosure buried inside it. Fujikura did not warn that orders were thinning; it warned of the opposite problem. In racing to expand output to meet the flood of demand, management said, it risks outrunning its own supply of inputs — naming hydrogen explicitly, alongside tight naphtha and shipping disruption it attributed to a Strait of Hormuz blockade — and it chose to bake that physical-procurement risk into the forecast conservatively rather than promise volumes it might not be able to source.FN1 Hydrogen belongs at the centre of the story because it is consumed in the making of fibre, not in the fibre itself: oxy-hydrogen flames synthesise the ultra-pure glass preform and then draw it into strand, and only high-purity hydrogen will do — the very same scarce, electronics-grade molecule that semiconductor fabs and the energy transition are simultaneously bidding away.FN3 Hence the elegant irony for an investor: the constraint that halved the stock is the strongest confirmation that the underlying demand is real. A company only frets about securing enough hydrogen when it is trying to make more cable than its supply chain can feed.

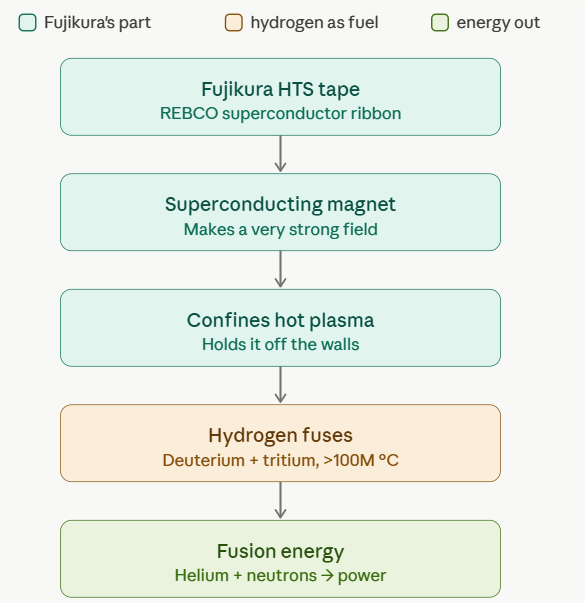

So how does Fujikura mean to win the hydrogen back? Its answer is threefold, and deliberately unglamorous. First, it is treating gas as a strategic line item rather than a procurement afterthought — moving to lock in and diversify hydrogen supply through longer-term agreements instead of leaning on a spot market that semiconductors and clean-energy projects are already draining.FN4 Second, it is relocating the problem closer to its solution: of the up-to-¥300 billion capacity programme, roughly ¥260 billion is being steered into the United States — a dedicated Delaware subsidiary, output aimed at quadrupling the 2022 baseline — so that new fibre lines sit inside American energy and industrial-gas infrastructure and beside the very hyperscalers buying the cable, while a fresh ≈¥40 billion line at the Sakura works in Japan introduces next-generation processes that lower the hydrogen drawn per kilometre of fibre. The candid catch, which is exactly why guidance was cautious, is that none of this is instant: meaningful new capacity arrives only gradually from about 2030, with the U.S. plant at full tilt only by fiscal 2035, so the squeeze eases rather than vanishes.FN4 And here the hydrogen theme runs deeper than the furnace, in a way a reader who cares about the molecule will enjoy: the same materials science that wins Fujikura the fibre market also makes it a three-decade world leader in REBCO high-temperature superconducting tape, the ribbon now being wound into the magnets that cage fusion plasma — Fujikura already ships these tapes in volume to Commonwealth Fusion Systems, has a framework with Britain’s fusion programme, and lists superconducting wire for fusion among its “Fourth Founding” businesses.FN4 The fuel of those reactors is, of course, hydrogen itself — its heavy isotopes, deuterium and tritium — so Fujikura ends up on both sides of the same element: burning high-purity hydrogen to draw the fibre that wires today’s AI boom, and building the magnets meant to one day confine hydrogen hot enough to power it. The fusion business is still small; the symmetry is not.

Illustration of Hydrogen as Nuclear Fuel in Fusion and Fujikura’s HTS Role

Illustration prepared by AI and SIDR. AI‑generated content may contain inaccuracies; please review with appropriate expert judgment. In nuclear fusion, hydrogen isotopes (deuterium and tritium) act as the fuel, forming a >100 million °C plasma that must be magnetically confined to prevent contact with the reactor walls. Fujikura’s REBCO high‑temperature superconducting (HTS) tape enables the powerful superconducting magnets that create this magnetic “cage,” allowing stable plasma confinement. When fusion occurs, hydrogen nuclei combine to produce helium and high‑energy neutrons, releasing usable fusion energy—highlighting a fundamentally different mode of hydrogen utilization compared with its role as a combustion fuel in optical‑fiber manufacturing.

References

- The “Fujikura Shock.” Record FY2026 results (revenue ¥1.18 tn, +20.7%; operating profit ¥188.7 bn, +39.2%; net profit ¥157.2 bn, +72.5%), the limit-down reaction and ~¥6 tn one-week loss of market capitalization, the FY2027 guidance (revenue +5.1%, net profit −0.7%), and the two stated causes — a conservatively modelled supply-chain/geopolitical risk citing hydrogen and other raw-material procurement, tight naphtha and Strait-of-Hormuz logistics, plus the non-recurrence of prior-year one-off securities gains (≈¥8.6 bn). Bloomberg (Japanese), 25 May 2026 · Money Post WEB / Yahoo Finance, 20 May 2026 · Nikkei, 14 May 2026

- The product franchise and the real demand. SWR® / WTC® high-density cable (up to 13,000 fibres per cable) and Fujikura’s commanding fusion-splicer share; saturated data-centre ducts driving “designated-buy” status; ~45% telecom-segment growth; the up-to-$20 billion U.S. AI-infrastructure selection (Oct 2025); and the 2026–2028 medium-term plan (revenue ¥1.6 tn, operating profit ¥315 bn, ~19.7% margin) concentrating ~90% of 2028 operating profit in information & telecommunications. Money Post WEB / Yahoo Finance, 20 May 2026 · Invest Leaders analysis (mid-term plan), May 2026 · Datacenter Dynamics, 19 Mar 2026

- Hydrogen’s role in fibre manufacture and why it is tight. Oxy-hydrogen burners/torches control flame temperature in VAD/OVD/MCVD preform synthesis and fibre drawing; high-purity (≥99.999%) hydrogen is structurally scarce as semiconductor fabrication and the energy transition compete for the same certified gas. US Patent 6,834,516 (oxy-hydrogen preform process) · High-purity hydrogen market analysis, 2026

- Fujikura’s response, and the fusion adjacency. The drive to bolster and diversify hydrogen procurement; the up-to-¥300 billion programme with ≈¥260 billion directed to the U.S. (Delaware subsidiary; output targeted at ~4× the 2022 baseline), the ≈¥40 billion next-generation Sakura line, and capacity arriving gradually from ~2030 with the U.S. plant at full output by FY2035. Separately, Fujikura’s 30-plus-year leadership in REBCO 2G high-temperature superconducting (HTS) tape for fusion magnets, volume supply to Commonwealth Fusion Systems, its UK fusion framework, and superconducting wire for fusion as a named “Fourth Founding” business. Nikkei Asia, 2 Jun 2026 · ad-hoc-news, May 2026 · Fujikura — “Technology is the key to fusion energy” · BigGo Finance (medium-term plan), May 2026

Prepared as an SIDR research note. Figures and characterizations are drawn from the cited public reporting as of June 2026 and may change. Informational only; not investment advice and not a recommendation to buy or sell any security.