Photo by Benjamin Smith. This article includes AI‑generated content. It does not constitute investment advice, nor does it imply any forecast or recommendation. All decisions should be based on independently verified data and the reader’s own judgment and professional expertise.

Markets keep a running tally of fear, and they keep it in prices. Eiji Kinouchi, the chief technical analyst at Daiwa Securities and a perennial chart-topper in Japan’s analyst rankings, has for some time treated one instrument in particular as a clean read on that tally: the iShares U.S. Aerospace & Defense ETF, ticker ITA.FN1 The logic is almost embarrassingly direct. Equity indices fold together earnings, liquidity, sentiment, and the price of every conceivable input; a basket of prime contractors and missile-makers does something narrower. It rises when the world expects to buy more weapons, and it sinks when the world expects to buy fewer. ITA is, in effect, the market’s option on disorder.

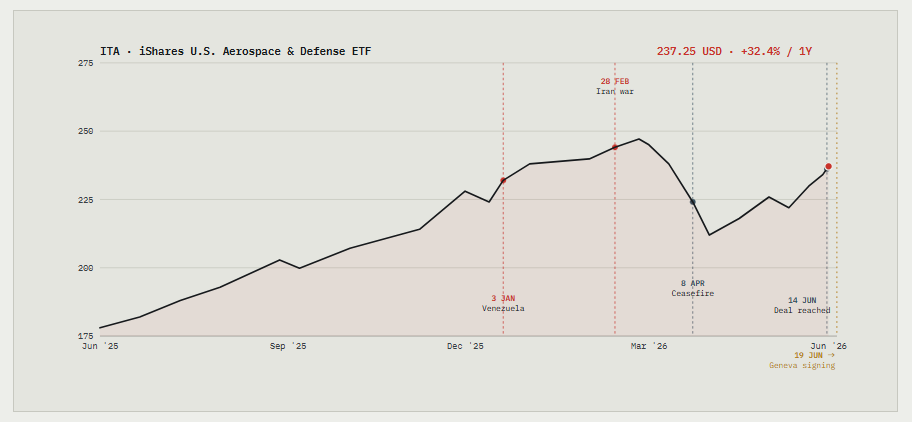

That option is currently expensive — and stubbornly so. ITA’s trailing-year gain of better than thirty percent is unremarkable for a defense complex in a year of war.FN2 What is remarkable is the shape of the curve after the fighting was supposed to stop. On 14 June the United States and Iran declared an immediate and permanent end to hostilities, with a formal signing set for 19 June in Geneva; Brent and WTI both fell roughly four percent on the news as the Strait of Hormuz prepared to reopen.FN8FN9 Oil believed the peace. Defense did not. ITA held within touching distance of its highs, declining to surrender the premium that four months of war had built into it.

A ceasefire that does not lower the price of insurance is not, to the market, a ceasefire at all.

ITA: The Defense Barometer Through a Year of Escalation

Notes: Price data are indicative and for illustrative purposes only. This chart is schematic and not intended as investment advice; verify figures against primary sources before use. A defense-sector ETF has become Wall Street’s quietest seismograph. Six months into the most violent year of the post-Cold-War order, it is refusing to point back toward calm — and that refusal is the signal. This chart includes AI‑generated elements and schematic redrawing for illustrative purposes. The chart was created as of June 16, 2026. All quantitative references should be verified against the original source data. ITA closed at 237.25 on 15 June 2026, near its cycle high and up roughly a third over the trailing year. The trace climbs through every escalation of 2026 and — critically — has not retraced the geopolitical risk premium following the 14 June ceasefire announcement, days ahead of the 19 June Geneva signing. FN1 FN2

There are two readings of that divergence. The benign one is mechanical: defense order books are multi-year, governments are re-arming on structural rather than episodic grounds, and a single Middle Eastern truce does not unwind a rearmament cycle. The less comfortable reading is forward-looking. If ITA is a barometer and the barometer will not fall after the storm passes, the instrument is telling you another storm is already forming on the glass. This essay takes the second reading seriously and asks what the chart may be pricing. The answer, theater by theater, is that 2026 has been a year organized around geopolitics — and the second half offers little reason to expect that organizing principle to relax.

II. The Donroe Doctrine

To understand the year, begin with the document that framed it. In its November 2025 National Security Strategy, the Trump administration formally reasserted the Monroe Doctrine, branding the revival the “Trump Corollary.”FN3 Commentators promptly nicknamed it the Donroe Doctrine: a declaration that the Western Hemisphere is an American sphere from which extra-hemispheric competitors — read China and Russia — are to be excluded, by force if necessary.FN3 It read, at the time, as rhetoric. It did not stay rhetoric for long.

On 3 January 2026, in an operation codenamed Absolute Resolve, U.S. forces struck across northern Venezuela, seized President Nicolás Maduro and his wife in the early hours, and flew them to New York to face charges.FN4 It was the most consequential U.S. military intervention in Latin America since the 1989 invasion of Panama, and its second-order effects fanned outward immediately. Venezuelan officials reported dozens killed, among them more than thirty members of the Cuban military and intelligence services — a detail that placed Havana, not merely Caracas, inside the blast radius.FN5 Colombia’s President Petro deployed security forces to the border in anticipation of a refugee surge.FN6 During the subsequent Iran war, talk of Cuba as a next object of pressure resurfaced, and capitals from Bogotá to Brasília recalibrated.

The Donroe Doctrine did not end at Caracas. It began there.

The strategic content of the doctrine is the point. A hemisphere declared off-limits to rivals is a hemisphere in which interventions become not exceptional but doctrinal — the expression of a stated policy rather than a departure from one. For a defense barometer, that is a structural input, not a one-time shock. It is precisely the kind of regime change that keeps a premium from decaying.

III. The Levantine Ledger

The Middle Eastern chapter of 2026 was both the most violent and, on paper, the one now closest to resolution. On 28 February, Israel and the United States launched airstrikes against Iran that killed its supreme leader and a tranche of senior officials, destroyed military and government targets, and drew Iranian missile and drone retaliation against Israel, U.S. bases, and allied states across the region.FN7 Tehran’s most consequential response was economic warfare: it closed the Strait of Hormuz, choking roughly a fifth of seaborne oil and detonating the energy-price shock that has shadowed every S1:DR note since.

The war’s decapitating character — leadership, not merely infrastructure, as the target — is the detail that propagates. When a great power demonstrates both the intent and the capability to remove a head of state by force, every adversarial leader recomputes their own risk. The lesson was not lost on Pyongyang, and it will not be lost on anyone else who governs without a nuclear guarantee. After a two-week truce in April collapsed into a U.S. naval blockade, the framework deal of 14 June and the Geneva signing scheduled for 19 June now promise to reopen Hormuz and lift the blockade.FN7FN8

Yet the ledger does not net to zero. The deal nominally encompasses Lebanon, where Israel has pressed its deepest incursion in over a quarter-century against Hezbollah; the most recent escalation, a week before the announcement, drew Iranian missiles at Haifa and Israeli strikes deep into Iran.FN10 Israel is not a party to the negotiated terms and reserves its own judgment on Iranian enrichment. A signature in Geneva on Friday closes a war; it does not close the question of whether the cessation holds past the first violation. The market’s refusal to discount the risk premium is, in this light, less a contradiction than a probability estimate.

IV. The Pacific Theater

If the Atlantic and the Gulf supplied 2026’s kinetic headlines, the Pacific supplied its structural anxiety. At their Beijing summit on 14–15 May, Presidents Trump and Xi discussed the Korean Peninsula, the status of Taiwan, the Iran war, and trade; the White House fact sheet recorded a reaffirmed “shared goal” of denuclearizing North Korea, and both leaders endorsed an open, toll-free Strait of Hormuz.FN11 The language on Pyongyang was, by most expert assessments, more symbolic than operational: China has quietly stopped emphasizing denuclearization, recognizing that Kim has firmly rejected it.

The point was underlined three weeks later. On 8–9 June, Xi made his first overseas trip of 2026 to Pyongyang — his first in seven years — and called for deepened strategic coordination, conspicuously declining to mention denuclearization at all.FN12 The choreography matters. A North Korea courted simultaneously by Beijing and Moscow, watching Iran’s leadership decapitated by foreign airpower, has every incentive to harden rather than bargain. Taiwan, meanwhile, sits where it has long sat — under a strait whose temperature the Venezuela precedent did not cool. Analysts noted that a successful U.S. operation against a sovereign state sets a precedent that other powers may read in their own favor.

The decapitation lessonA regime that watches a rival leader removed by airpower does not disarm. It digs in.

V. The Eurasian Endgame

The oldest war on the board may be approaching its most dangerous phase — not because Russia is winning, but because it is exhausting itself. In June, the Kiel Institute for the World Economy and Stockholm’s Institute of Transition Economics published a report whose title supplies its thesis: Endgame: The State of the Russian Economy.FN13 Four years into the full-scale invasion of Ukraine, the report finds Russia’s fiscal buffers largely depleted: the liquid assets of its sovereign wealth fund have shrunk from roughly 6.5 percent of GDP at the war’s outset to about 1.8 percent by April 2026, growth has stalled, and dependence on China has deepened into structural reliance.FN14 Compounding the arithmetic is demography — a war that has thinned the ranks of Russia’s young and accelerated exile and aging.FN16

Here the analysis turns counterintuitive, and the most provocative version of it has circulated among strategists such as Yu Koizumi and Emin Yurmaz: a Russia that weakens too far becomes a destabilizing vacuum rather than a contained threat.FN15 A state spanning eleven time zones, rich in resources and ringed by neighbors with longer memories than borders, does not collapse quietly. The uncomfortable corollary is that the advanced economies might one day find it in their interest to keep a defeated Russia solvent — to prevent its disintegration from inviting the very land-border incursions that a strong Russia once deterred.

To prop up a rival you have spent four years bleeding is the oldest and least sentimental act of statecraft.

Whether that scenario arrives or not, the report’s operative line is its claim that “the window for consequential Western action is open.” A window that is open is a window through which something passes. For a defense barometer, an endgame is not an off-ramp; it is the most uncertain stretch of the road.

VI. The Map of a Year

Collected on a single map, the flashpoints of 2026 do not cluster. They span every inhabited continent, and several burn at once — a simultaneity that is itself the story. The market is not pricing one conflict; it is pricing a world in which conflicts have stopped queuing.

Global Flashpoints 2026: A Concurrent Map of Conflict and Risk

Notes: This chart includes AI‑generated elements and schematic redrawing for illustrative purposes only. The chart was created as of June 16, 2026. All quantitative and qualitative references should be verified against the original source data. FIG. 2 A schematic ledger of 2026’s principal flashpoints. Three are active (Venezuela’s aftermath, the Iran–Israel–Lebanon complex, the Russia–Ukraine front); five are elevated (Cuba, Colombia, Hormuz, Taiwan, North Korea); one — the South China Sea — sits on watch. The diagnostic feature is not any single marker but their concurrency. FN3–FN16

Beyond the marked theaters, the periphery is busy. The Sahel and the Horn remain volatile; the Caucasus is unsettled; cyber and maritime grey-zone friction runs continuously beneath the threshold of declared war. None of these alone moves a global barometer. Together, and layered atop the principal theaters, they describe an environment in which the demand curve for deterrence shifts out and stays out.

VII. Conclusion

The first half of 2026 was, unambiguously, a geopolitically organized year. A hemispheric doctrine was operationalized in Caracas in January; a war that targeted a head of state and closed Hormuz erupted in February; a great-power summit and a Pyongyang pilgrimage rearranged the Pacific in May and June; and a four-year European war entered its endgame. Through all of it, the cleanest market read on disorder climbed and then refused to descend. Our base case for the second half is continuity, not relief: the Geneva signing closes one file while the doctrine, the precedent, and the endgame keep three others open.

References

- Daiwa Securities, profile of Eiji Kinouchi (Chief Technical Analyst), and televised commentary using ITA as a geopolitical-risk proxy. See “Reaching ¥68,000: Asking Kinouchi about the outlook for Japanese equities” (16 June 2026). youtube.com/watch?v=qM2EgfNnWwU; analyst profile, daiwa.jp/market.

- iShares U.S. Aerospace & Defense ETF (Cboe BZX: ITA). Price 237.25 USD, +32.4% trailing 12 months, as of close 15 June 2026 (per quoted screen). Fund data: ishares.com (ITA).

- The White House, National Security Strategy of the United States of America, November 2025 — “Trump Corollary to the Monroe Doctrine,” Western Hemisphere section: whitehouse.gov. “Donroe Doctrine” framing: ABC News (6 Jan 2026); Atlantic Council, “The Trump Corollary is officially in effect” (8 Jan 2026): atlanticcouncil.org.

- “2026 United States intervention in Venezuela” (Operation Absolute Resolve, 3 Jan 2026); Brookings, “Making sense of the US military operation in Venezuela” (15 Jan 2026). brookings.edu.

- Reported casualties including Cuban military and intelligence personnel: New York Times reporting summarized in Wikipedia, “2026 United States intervention in Venezuela.” en.wikipedia.org.

- NPR, “U.S. strikes in Venezuela trigger regional and global alarm” — Colombia border deployment under President Petro (4 Jan 2026). npr.org.

- “2026 Iran war” / “2026 Iran war ceasefire”: 28 Feb 2026 U.S.–Israeli airstrikes killing Iran’s supreme leader and senior officials; Iranian retaliation; closure of the Strait of Hormuz; April two-week truce and subsequent U.S. naval blockade. en.wikipedia.org.

- CNBC, “US, Iran agree to peace deal” (14 Jun 2026); Al Jazeera, “US, Iran to sign a ‘peace deal’ on Friday” (15 Jun 2026) — signing set for 19 June in Switzerland (Geneva). cnbc.com; aljazeera.com.

- Oil reaction to the ceasefire: Brent ≈ −4% to ~$83.82; WTI ≈ −4.6% to ~$80.95, on the prospect of an open Strait of Hormuz. business-standard.com.

- Lebanon dimension and Israel–Hezbollah fighting; Israel as non-signatory: NewsNation, “US, Iran agree to peace deal” (Jun 2026). newsnationnow.com.

- Trump–Xi Beijing summit, 14–15 May 2026 — North Korea, Taiwan, Iran war, Hormuz; White House fact sheet on a “shared goal” of denuclearization. Korea Herald (18 May 2026); UPI (18 May 2026). koreaherald.com.

- Xi Jinping’s visit to North Korea, 8–9 June 2026 (first in seven years; no public mention of denuclearization): CNN (7 Jun 2026); Brookings, “China, North Korea, and the Xi–Kim summit.” brookings.edu.

- Kiel Institute for the World Economy & Stockholm Institute of Transition Economics (SITE), Endgame: The State of the Russian Economy (Kiel Report, June 2026). kielinstitut.de.

- Russian sovereign wealth fund liquid assets ≈ 6.5% of GDP at war’s start → ≈ 1.8% by April 2026; stalled growth and deepening China dependence (Schularick). Reporting via Reuters/Yahoo Finance, 11 Jun 2026. finance.yahoo.com.

- On a weakened Russia as a destabilizing vacuum and the “rescue” thesis — strategic discussion featuring Yu Koizumi and Emin Yurmaz, “2050 super-forecast: decline of great powers and Japan’s survival strategy.” youtube.com/watch?v=QaNrFfegXHE.

- Russian demographic decline and exile accelerated by the war; European balance-of-power context: Ifri, “Europe–Russia: Balance of Power Review” (Nov 2025). ifri.org.

Notes: Prepared for research and discussion. Nothing herein constitutes investment advice or a solicitation. Figures are schematic and illustrative; verify against primary sources before use.