Photo by Daivik Goel on Unsplash

From NVIDIA’s historic $82 billion quarter to Kawasaki’s Physical AI partnership, Hitachi’s Anthropic deal, and Kioxia’s NAND revolution — a complete DOE ARL analysis of the global semiconductor ecosystem, told in the order it happened.

NVIDIA Reports $81.6 Billion Quarter. Jensen Huang Just Rewrote the Rules.

In the history of the semiconductor industry, no company has ever reported a quarter like this. NVIDIA posted revenue of $81.62 billion — up 85% year-over-year, nearly double what analysts expected just eighteen months ago. Data center revenue hit $75 billion (+92% YoY). Free cash flow reached a record $49 billion at a 74.9% gross margin. Earnings per share came in at $1.87, beating the $1.76 Street estimate. The company announced an $80 billion share buyback and raised its dividend.[FN1]

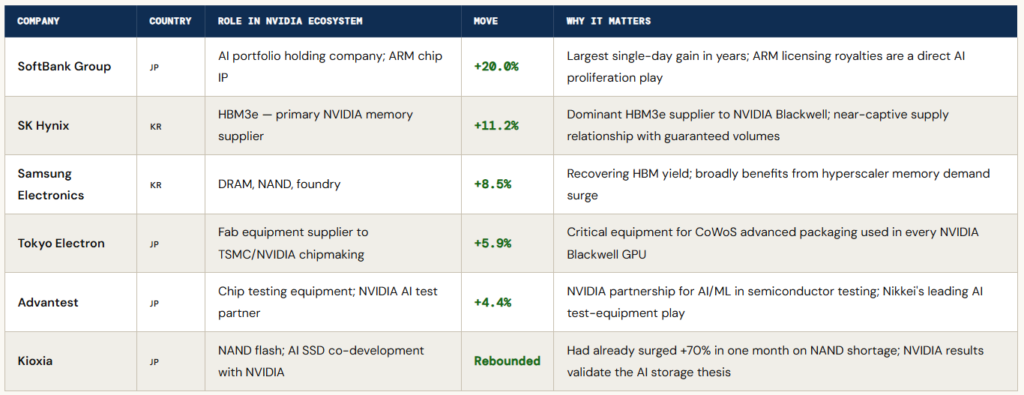

The morning after, Asian semiconductor supply chains lit up like a circuit board. The results were not just a milestone — they were a signal flare for every memory producer, equipment maker, and industrial company that has bet its future on AI. The question now is not whether the AI supercycle is real. It is who is positioned to capture it.

The NVIDIA results cascaded through Asian markets on the morning of May 21. Here is the immediate supply chain scorecard:[FN2]

The SOX’s Historic 18-Day Run — What Came Before

Before NVIDIA’s record-shattering quarter, markets were already in uncharted territory. In April 2026, the Philadelphia Semiconductor Index (SOX) logged eighteen consecutive sessions of gains — something that had never happened in the index’s history. During that run, the SOX surged approximately 45%. The twelve-month return now stands near +143%. The iShares SOXX ETF has delivered year-to-date returns above +65%.[FN3]

What drove the streak? Not sentiment alone. In late 2025, the AI semiconductor trade underwent what analysts called a “great broadening” — where previously only GPU makers like NVIDIA were rewarded by markets, the investment wave had begun lifting the entire silicon ecosystem: memory, storage, analog, testing equipment, and advanced packaging. The SOX’s 18-session run was the prelude. NVIDIA’s Q1 FY2027 report is the crescendo.

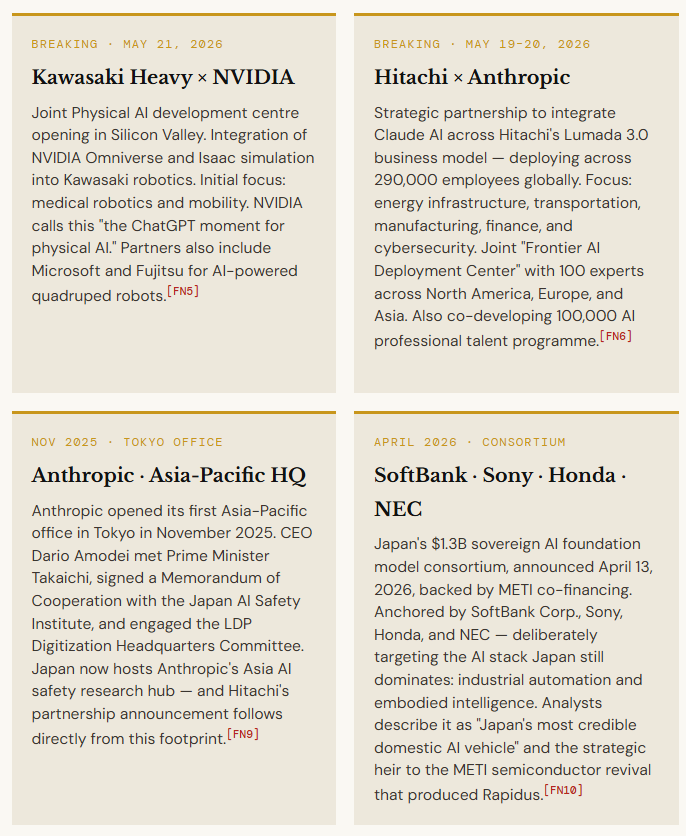

Japan Pivots: Kawasaki × NVIDIA, Hitachi × Anthropic, and the VC Invasion

On the same day NVIDIA published its record quarterly results, Nikkei broke another story that underscores how deeply the AI supercycle has embedded itself into Japan’s industrial fabric: Kawasaki Heavy Industries is partnering with NVIDIA to develop Physical AI, establishing a joint robotics development centre in Silicon Valley. The partnership will integrate NVIDIA’s AI and simulation technologies — including Omniverse and Isaac — into Kawasaki’s robotics platforms, with an initial focus on medical and mobility applications. Kawasaki is also working with Microsoft and Fujitsu on AI-powered four-legged robots.[FN5]

The common thread across all of these announcements is unmistakeable: global AI’s centre of gravity is shifting toward physical intelligence — robots, infrastructure systems, industrial automation, healthcare — and Japan, with its century-deep manufacturing expertise, is uniquely positioned to capture this layer of the AI stack. The Kawasaki–NVIDIA partnership is not an isolated deal. NVIDIA’s GTC 2026 keynote in March listed over 110 Physical AI ecosystem partners including FANUC, Yaskawa, and ABB — Japan’s robotics giants are not bystanders in this transition.[FN5]

“NVIDIA is the world’s largest robotics company that doesn’t build robots.”— Rev Lebaredian, VP of Omniverse and Simulation Technology, NVIDIA · GTC 2026[FN5]

DOE ARL Framework: The Analytical Lens

To move beyond market price action and understand who has structural adoption readiness, this report applies the Adoption Readiness Level (ARL) Framework developed by the U.S. Department of Energy’s Office of Technology Commercialization.[FN11] ARL measures the commercialisation and adoption risks a technology faces across 17 dimensions in four buckets, scored 1 (early-stage, high-risk) to 9 (fully mature, low-risk).

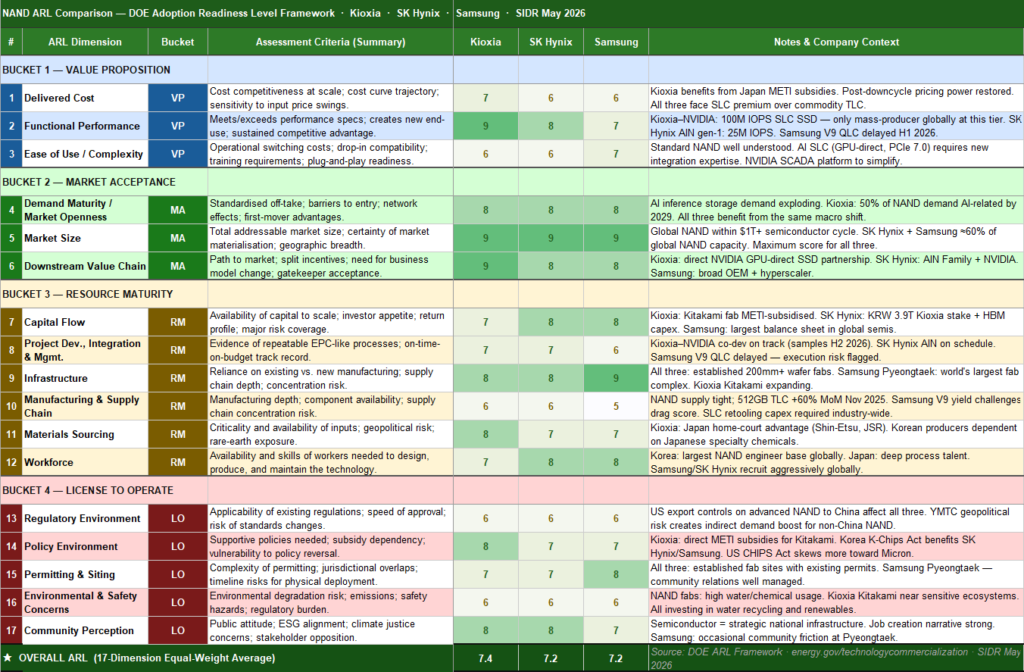

NAND ARL: Kioxia vs SK Hynix vs Samsung

NAND flash is the long-term memory of AI — retaining model weights, datasets, and outputs across power cycles. Kioxia’s NVIDIA partnership for 100M IOPS AI SSDs gives it the highest Functional Performance score of any NAND producer globally. The Physical AI era — robots that need to store vast environment maps and model states — will dramatically accelerate NAND’s AI transition.[FN12]

Data and analysis prepared by SIDR Research Desk and AI. This document incorporates AI-assisted analysis. While the content has been reviewed for accuracy and consistency, AI-generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification. ARL framework: U.S. Department of Energy Office of Technology Commercialization, 2024.

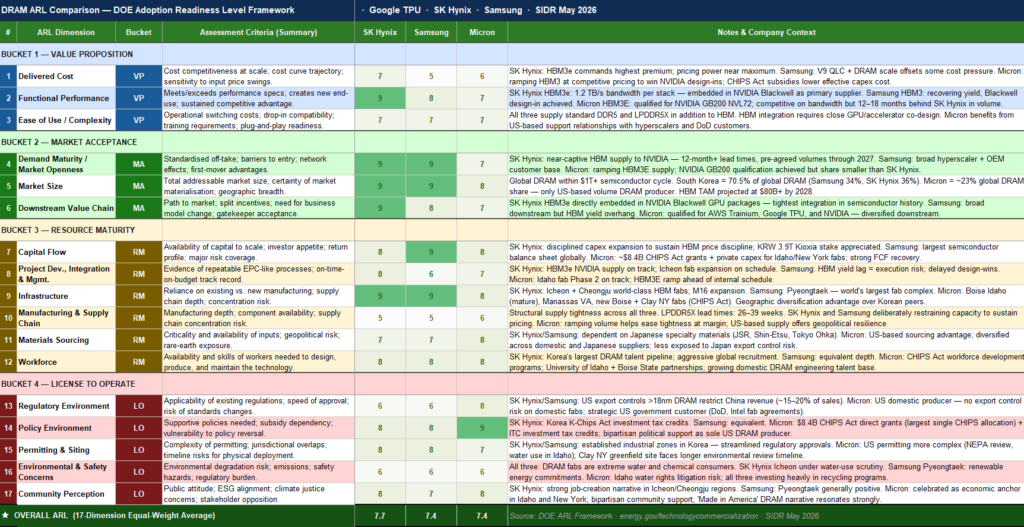

DRAM ARL: Google TSU vs SK Hynix vs Samsung

DRAM is the inference engine of AI — its speed enables real-time neural network predictions. SK Hynix’s HBM3e is directly embedded in NVIDIA Blackwell packages, creating one of the tightest customer-supplier integrations in the history of the semiconductor industry. OpenAI alone reportedly consumes approximately 40% of global DRAM supply.[FN13]

Data and analysis prepared by SIDR Research Desk and AI. This document incorporates AI-assisted analysis. While the content has been reviewed for accuracy and consistency, AI-generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification. ARL framework: U.S. Department of Energy Office of Technology Commercialization, 2024.

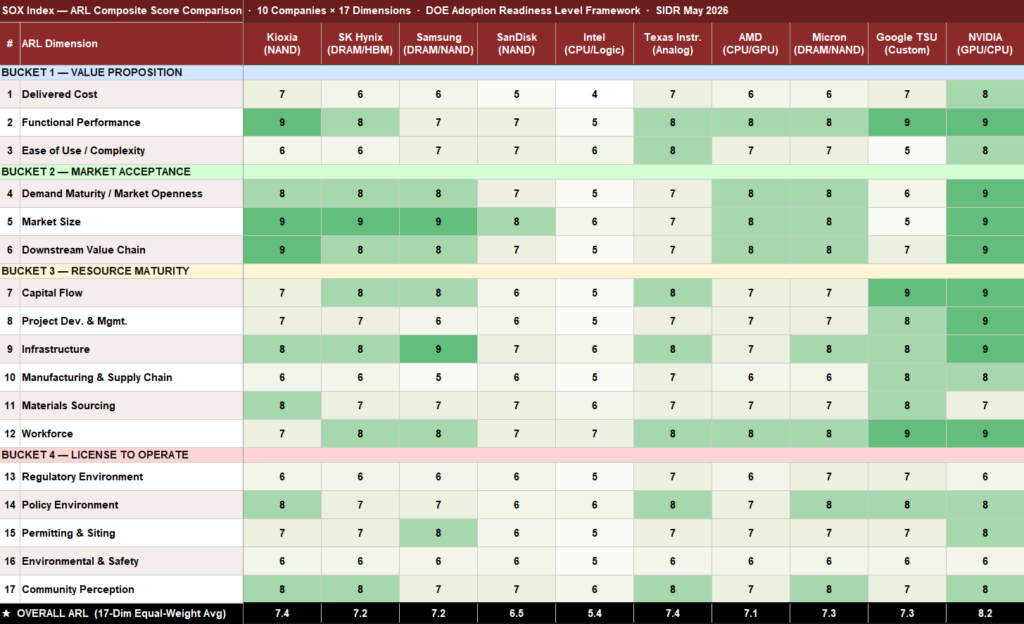

SOX 10-Company ARL Composite

The matrix below extends the ARL analysis across ten SOX-listed companies — from pure-play NAND to HBM-dominant DRAM, analog, AI compute, and captive custom silicon. Reading across the rows reveals which dimensions are universally strong (Market Size, Policy Environment) and which remain contested (Delivered Cost, Manufacturing).[FN14]

Data and analysis prepared by SIDR Research Desk and AI. This document incorporates AI-assisted analysis. While the content has been reviewed for accuracy and consistency, AI-generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification. ARL framework: U.S. Department of Energy Office of Technology Commercialization, 2024.

NVIDIA’s CUDA Fortress — and the Cerebras Siege

NVIDIA controls approximately 80% of the AI chip market — and the moat is not primarily hardware. It is CUDA: a 20-year-old software ecosystem with millions of developer-hours of optimisation, debugging, and institutional knowledge baked in. Once a team begins training on NVIDIA’s GPU stack, the switching cost is organisational, not just technical: retraining engineers, porting hand-optimised CUDA kernels, rebuilding profiling workflows.[FN15] NVIDIA reinforces this deliberately — its annual GPU cadence (Blackwell → Rubin 2026 → Rubin Ultra 2027) maintains strict backward compatibility, ensuring every new generation is the natural upgrade path for existing CUDA users.

“We position NVIDIA as the core of our training and inference architecture while deliberately expanding the ecosystem beyond the core through partnerships with Cerebras, AMD, and Broadcom.”— OpenAI spokesperson, February 2026[FN16]

Cerebras Systems is the most credible challenger — but specifically in inference, not training. Its wafer-scale WSE-3 architecture delivers up to 15× lower latency than GPU-based solutions for certain workloads. OpenAI signed a $20B+ agreement with Cerebras in January 2026 for 750MW of low-latency inference capacity, expandable to 2GW by 2030. Cerebras filed for a Nasdaq IPO at a $35 billion valuation in April 2026.[FN17]

OpenAI’s multi-vendor compute strategy (NVIDIA 10GW + AMD 6GW + Broadcom 10GW + Cerebras 750MW) is supply diversification, not an exit from CUDA. NVIDIA spent $18B on R&D in FY2026, acquired Groq for $20B in December 2025, and is shipping Blackwell + Groq LPX specifically to close the inference latency gap. AMD’s MI400 “Helios” with HBM4 and 19.6 TB/s bandwidth, and Google TPU v7 “Ironwood” at 4,614 TFLOPS (+67% efficiency vs H100) are real competitors — but displacing NVIDIA’s training dominance remains a decade-level project. The CUDA moat is widest exactly where it matters most.[FN17]

Why CPUs Are the AI Era’s Surprise Winner

NVIDIA’s Q1 FY2027 guidance contained a figure that deserves more attention: the company expects $20 billion in CPU revenue for 2026 — which would make it the world’s largest CPU supplier by revenue, displacing Intel.[FN18] This reflects a structural truth: production AI pipelines are not purely GPU workloads. Every inference pipeline requires CPUs for pre-processing, orchestration, memory management, edge inference, and post-processing. Agentic AI systems require fast, deterministic CPU decision loops. Physical AI — robots, autonomous vehicles, industrial automation — is especially CPU-intensive.

For DRAM: CPU-adjacent memory (DDR5, LPDDR5X) is experiencing growth independent of the HBM story. For NAND: CPU-orchestrated AI pipelines access model weights on high-speed NVMe SSDs — exactly the workload Kioxia and SK Hynix’s next-generation SLC SSDs target. The hyperscalers plan a combined 36% YoY increase in infrastructure capex for 2026 — driving demand across every layer of the compute stack.[FN4]

Kioxia’s Bet: NAND That Thinks Like DRAM

Conventional NAND operates approximately 1,000× slower than DRAM — wide enough to render it irrelevant for latency-sensitive AI inference. Kioxia’s next-generation AI SSD, developed in partnership with NVIDIA, targets 100 million IOPS — a roughly 100× improvement over today’s standard SSDs. The GPU-direct architecture bypasses CPU and system memory bottlenecks; PCIe 7.0 connectivity further reduces latency. Sample shipments: H2 2026. Full commercial production: 2027.[FN12]

“Kioxia’s new NAND achieves 100× the speed of conventional NAND, making it viable for AI inference co-location. NVIDIA, Meta, and other hyperscalers have received this technology with significant enthusiasm. Kioxia is currently the only producer in the world capable of mass-producing NAND at this performance tier.”— Satoshi Oyama, semiconductor analyst, 大川智宏×大山聡 commentary, YouTube 2026[FN19]

Kioxia projects that by 2029, nearly 50% of all global NAND demand will be AI-related. SK Hynix is pursuing the same target via its AIN Family SLC NAND (25M IOPS today; 100M IOPS by end 2027). NVIDIA’s SCADA (SCaled Accelerated Data Access) software platform will manage the AI storage layer, eliminating the CPU as a data movement intermediary. If this succeeds, the traditional boundary between storage memory and working memory in AI systems will dissolve — one of the most consequential architectural shifts in 40 years of computing.[FN12,FN13]

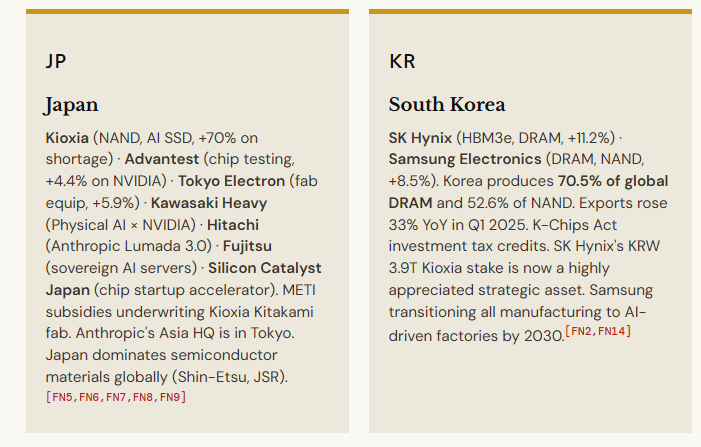

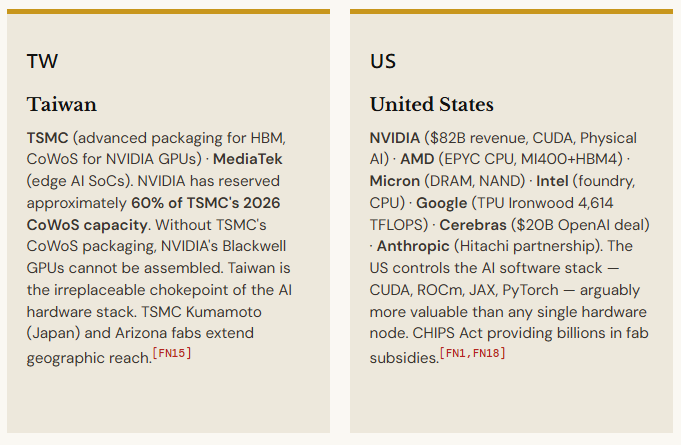

Four Nations, One Stack: Japan · Korea · Taiwan · USA

Conclusions: Who Controls the AI Stack?

The DOE ARL framework cuts through the noise. DRAM is the most mature AI technology by adoption metrics: demand is near-infinite, downstream integration is total, and Market Size is at maximum. Its vulnerabilities are Delivered Cost (prices at multi-year highs) and Manufacturing supply discipline (producers restraining capacity to sustain pricing). The oversupply risk window opens around 2027–2028, when major capacity additions are scheduled.

NAND is the dynamic story. Functional Performance — historically its weakest ARL dimension — is being transformed by Kioxia’s AI SSD programme. If 100M IOPS is achieved at commercial scale, NAND will begin substituting for HBM in AI inference, dissolving a boundary fixed for 40 years. The Physical AI era — robots and autonomous systems that need vast local storage for environment models and sensor data — will accelerate this transition further.

Japan is the story within the story. On a single day — May 21, 2026 — NVIDIA announced a Physical AI partnership with Kawasaki Heavy Industries, Hitachi announced a strategic AI partnership with Anthropic, and Kioxia’s NVIDIA-linked AI NAND thesis was validated by the most consequential semiconductor earnings report in history. This is not coincidence. Japan’s century-deep manufacturing expertise, its dominance in semiconductor materials and equipment, and its cultural alignment with Physical AI (robotics, precision manufacturing) positions it uniquely for the next phase of the supercycle.

The SOX’s eighteen-session winning streak was the setup. NVIDIA’s $82 billion quarter is the main event. But the real story — the one that will define the semiconductor industry through the rest of this decade — is the race to own the Physical AI stack: who makes the robots think, who supplies their memory, and who builds the fabs that produce the chips that make it all possible.

References & Footnotes

[FN1] Investing.com / Fortune 「NVIDIA Q1 FY2027: Revenue $82B (+85% YoY), EPS $1.87 vs $1.76, Data Center $75B (+92%).」 2026年5月20日

[FN2] CNBC 「SoftBank Group Shares Soar 20% as Nvidia Earnings Signal Strong AI Momentum。」 2026年5月21日

[FN3] GuruFocus 「Semiconductor Surge: SOX Index Hits Record 18-Day Climb。」2026年4月25日 iShares SOXX YTD +65%(iShares)

[FN4] Financial Content 「The Trillion-Dollar Pivot: Semiconductor Sector Surges for 2026 AI Supercycle。」 2025年12月22日

[FN5] Nikkei Asia / Seeking Alpha 「Kawasaki Heavy to Partner with Nvidia on Physical AI, Open US Robot Center。」2026年5月21日 NVIDIA Newsroom 「NVIDIA and Global Robotics Leaders Take Physical AI to the Real World。」2026年3月16日

[FN6] Japan Industry News / Webnewswire 「Hitachi Announces Strategic Partnership with Anthropic to Strengthen Lumada 3.0。」 2026年5月19–20日 Investing.com(同件報道)

[FN7] AI Business Review 「Sovereign AI Surge: Fujitsu Begins Made-in-Japan AI Server Production。」 2026年2月15日

[FN8] Silicon Catalyst / SemiWiki 「Silicon Catalyst Announces the Launch of Silicon Catalyst Japan。」 2025年11月3日

[FN9] MEXC / BitcoinEthereumNews 「Anthropic Expands to Asia with Tokyo Office and Japan AI Safety Partnership。」 2025年11月4日

[FN10] Tech-Insider 「Japan AI Foundation Model: $1.3B SoftBank-Sony-Honda Bet。」 2026年4月

[FN11] U.S. DOE Office of Technology Commercialization 「Adoption Readiness Levels (ARL) Framework」 「Core Risk Areas」

[FN12] TrendForce 「Kioxia Eyes 2027 Launch for NVIDIA-Partnered AI SSDs with 100x Speed Boost。」 2025年9月11日 Kioxia Holdings(同件情報)

[FN13] TrendForce 「SLC-Based AI SSDs: SK Hynix and Kioxia Accelerate Development with NVIDIA。」 2025年12月29日 Wikipedia 「2024–present Global Memory Supply Shortage」

[FN14] Industry Research Biz 「NAND Flash Memory and DRAM Market Size。」2026年4月 TrendForce 「Kioxia Stock Jumps 70% on NAND Shortage。」2025年9月

[FN15] xpert.digital 「OpenAI, Cerebras, and the NVIDIA Compute Shift — CUDA Lock-In Analysis。」 2026年1月

[FN16] Futunn / OpenAI 「OpenAI Positions NVIDIA as Core Architecture; Cerebras as Ecosystem Expansion。」 2026年2月

[FN17] Tech-Insider 「Cerebras IPO: $510M Revenue, OpenAI $20B Deal。」 2026年 buildmvpfast.com(同件情報)

[FN18] Fortune 「Nvidia Expects $20B in CPU Revenue in 2026 — Would Become World’s Largest CPU Supplier。」 2026年5月20日

[FN19] 大川智宏 × 大山聡(半導体アナリスト) YouTube対談「NVIDIA決算、キオクシア急騰」 2026年