Photo by Scott Rodgerson on Unspalsh

Our estimates indicate that sixty Nikkei 225 companies generate revenue from battery and EV‑related businesses. As momentum in the EV market slows, Japan’s industrial leaders are redirecting their hard‑won technical capabilities toward meeting the rapidly expanding power demands of the AI economy.

Japan’s battery industry is undergoing a strategic metamorphosis. What began as an EV-driven buildout over the past decade is rapidly evolving into a multi-application energy storage ecosystem — one spanning grid stabilization, AI data centers, and renewable integration. At the heart of this transformation is a cohort of well-capitalized industrial companies that have spent years developing cutting-edge battery technology, and are now redeploying that expertise to capture an entirely new class of demand.

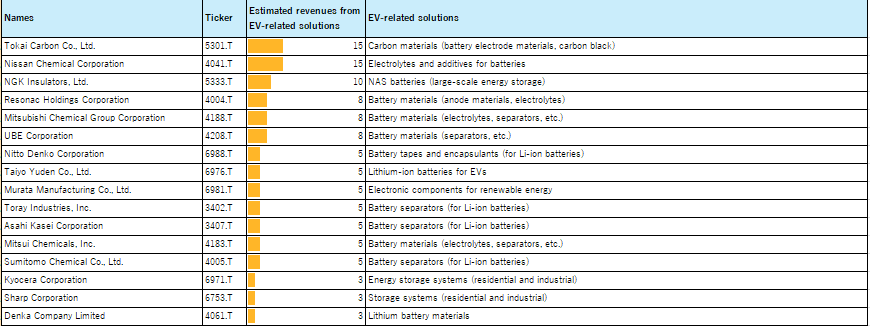

According to analysis by securities analyst Mariko Mabuchi, companies offering battery technologies and EV‑related solutions adaptable to AI data center applications are increasingly well positioned as power demand from AI workloads accelerates. Our assessment indicates that about sixty firms in the Nikkei 225 derive a meaningful share of their revenues from batteries and EV‑related solutions. [FN1] Together, they represent a cross-section of Japan’s industrial economy — from automakers and electronics conglomerates to chemical companies and trading houses. The charts below, which present the estimated revenue contribution from batteries and EV-related solutions for each of these companies, illustrates just how broadly this business has penetrated Japan’s corporate mainstream.

Estimated revenues from batteries

This analysis reflects AI-based estimates prepared by SIDR. The data represents the estimated share of total revenues attributable to batteries, EV systems, and EV-related solutions across Nikkei 225 constituents. Company names are presented in Japanese as originally reported.

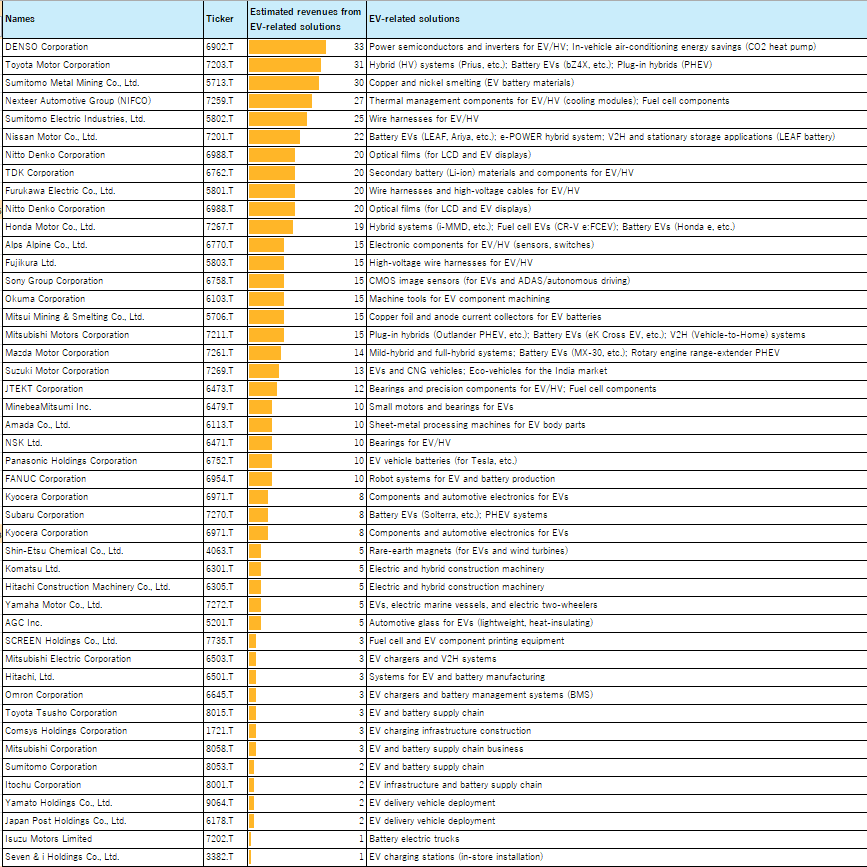

Estimated revenues from EV-related solutions

This analysis reflects AI-based estimates prepared by SIDR. The data represents the estimated share of total revenues attributable to batteries, EV systems, and EV-related solutions across Nikkei 225 constituents. Company names are presented in Japanese as originally reported.

A Market Built on Three Structural Pillars

As S1:DR has previously documented, Japan’s grid-scale battery storage market is propelled by three durable forces: the need to integrate an expanding base of intermittent renewable energy, the imperative to enhance energy security following the Fukushima-driven shift away from nuclear power, and the rapidly escalating electricity demands of AI-driven data center infrastructure.[FN2] Together, these forces are converting battery storage from a niche cleantech subsector into a mainstream industrial priority.

The market’s scale reflects this urgency. Japan’s battery energy storage systems (BESS) market generated revenues of approximately USD 343.6 million in 2024, and is projected to reach nearly USD 2 billion by 2030 — implying a compound annual growth rate of 34.9%.[FN3] Annual deployment of stationary storage is estimated at 2.5 to 3.5 GWh in 2026 alone, with cumulative installed capacity potentially reaching 30 to 45 GWh by 2035.

Panasonic: From Tesla’s Supplier to AI’s Powerhouse

No company better illustrates the EV-to-data-centre pivot than Panasonic. For years, its energy unit was best known as the primary battery supplier to Tesla, building cells at the Nevada Gigafactory and banking on the continued rise of the global EV market. That story has become more complicated: North American EV battery demand fell 16% year-on-year in the first quarter of fiscal year 2026, driven by the phase-out of EV tax incentives and rising competition from Chinese manufacturers.

Yet Panasonic’s energy division did not merely weather this downturn — it thrived. The unit reported a 47% surge in operating profit, reaching ¥31.9 billion (approximately USD 215 million) in Q1 FY2026, fuelled by a doubling of demand for energy storage systems at AI-powered data centres.[FN1] The pivot was not accidental. Panasonic had already spent more than a decade building relationships with hyperscale data centre operators and developing rack-mounted battery backup units (BBUs) for distributed power supply systems.

“The evolution of GPUs mounted in AI servers has led to increased power demand and sudden fluctuations in power load. Panasonic Energy is offering energy storage systems that can be installed in server racks — with a peak shaving function that supplies stored energy during periods of peak demand, realising highly energy-efficient operations and improved power management.” — Panasonic Energy, CES 2026

At CES 2026, Panasonic showcased its latest rack-mounted energy storage systems, engineered specifically for AI server environments where power loads can fluctuate between 10% idle and 150% overload in moments.[FN1] The company holds an estimated 80% share of the distributed power supply market for data centers globally, a dominant position it is now leveraging as hyperscalers accelerate their infrastructure buildout. Its data center battery products are, by the company’s own account, selling out.

This dual capability — serving both stationary energy storage and data center backup — exemplifies the strategic optionality that Japan’s battery manufacturers are now exploiting. The technical demands differ in important ways: data center batteries must handle extreme power density and thermal stress, while grid-scale storage prioritizes cycle life and capacity. Japanese firms, with their deep expertise in cell chemistry and system integration, are well-positioned to compete in both arenas.

Daiwa Securities Enters the Battery Business

Perhaps the most striking signal of battery storage’s maturation as an asset class is the entry of one of Japan’s largest investment banks. Daiwa Securities Group — through its infrastructure investment arm, Daiwa Energy & Infrastructure (DEI) — has committed to investing ¥100 billion (approximately USD 630 million) in battery storage facilities across Japan through 2030, targeting growing electricity demand from semiconductor fabs and data centres.[FN3]

DEI’s battery storage activity spans multiple fronts. In October 2025, it broke ground on a 38 MW / 160 MWh grid-scale BESS facility in Chitose, Hokkaido — a project designed to stack revenues across the wholesale electricity market, the balancing market, and the capacity market, with commercial operations targeted for 2027. In parallel, DEI established DAX, LLC, a joint venture with Fuyo General Lease and ASTMAX, which brought a 50 MW / 100 MWh BESS into operation on November 1, 2025, trading on AI-driven price forecasts. The firm has also invested in Exergy Power Systems, a battery storage startup spun out of the University of Tokyo, and is partnering with NGK Insulators and Ricoh through NR-Power Lab to develop a hybrid battery hub with leasing functionality for third-party users.[FN3]

DEI’s international footprint has expanded in parallel. The firm acquired a 49% equity stake in large-scale BESS projects in Texas (250 MW) and Veneto, Italy (130 MW), developed by Enfinity Global — positioning itself as a global battery storage investor rather than a purely domestic one. Since 2018, DEI has deployed more than USD 1 billion into renewables and infrastructure across Japan and Europe. This trajectory represents a notable diversification for a financial services group more traditionally associated with equity underwriting and bond trading — and reflects the degree to which battery storage has moved from a specialist cleantech investment into mainstream infrastructure.

The Broader Nikkei 225 Picture

The Mabuchi analysis, which underpins the chart in this article, maps estimated EV and battery revenue exposure across the entire Nikkei 225 universe. The spread is striking in its breadth. Denso leads with an estimated 33% of revenues attributable to EV and battery-related solutions, followed by Toyota at roughly 31% and Sumitomo Mining at approximately 30%. These are the companies that built the original EV supply chain — suppliers of motors, battery materials, and drivetrains.

Yet further down the distribution, the list encompasses chemical companies (Shin-Etsu Chemical, Tokai Carbon, Mitsui Chemicals), materials firms (Toray, AGC, Denka), heavy machinery manufacturers (Amada, Minebea Mitsumi), and trading houses (Mitsubishi Corporation, Itochu, Sumitomo Corporation). Each has found its own angle into the battery economy — whether supplying cathode precursors, separator films, precision components, or financing and offtake structures for storage projects.

This diversity suggests that Japan’s battery storage boom is not a narrow sectoral story but a structural transformation of the country’s industrial economy — one in which the skills and supply chains built for EVs are now being repurposed for a broader array of energy storage applications.

Policy as Catalyst

The Japanese government has been deliberate in creating conditions for this buildout. METI’s Green Transformation (GX) strategy sets a target of 36–38% renewables in Japan’s electricity mix by 2030, with carbon neutrality by 2050 as the long-term goal. Energy storage is recognized as an indispensable enabling technology for meeting these targets, and regulators have formally defined BESS as a grid-connected generation resource — a classification that unlocks access to wholesale, balancing, and capacity market revenues.

The subsidy environment has followed. A national capex support scheme covers up to one-third of project costs, while the Tokyo Metropolitan Government offers supplementary support of up to 50%. The Battery Industry Strategy, revised in 2025, mandates 30% domestic cell production for EVs by 2030 and commits JPY 150 billion in funding for pilot and demonstration lines through 2027. The Next Generation Battery Technology Research Association (NGBRA), comprising more than 20 Japanese firms, is coordinating pre-competitive R&D on sulfide solid electrolytes and sodium-ion cathode materials, with pooled funding of JPY 50 billion over 2025–2030.

Challenges on the Horizon

The market’s growth trajectory is compelling, but not without friction. Japan remains structurally import-dependent for battery cells and critical minerals: roughly 55–65% of lithium-ion imports arrive from China, and system-level prices for utility-scale BESS in Japan range from ¥40,000 to ¥60,000 per kWh — meaningfully higher than in more mature markets. Grid connection wait times are long, land suitable for large-scale storage is scarce, and Japan’s regulatory environment for energy storage has historically been characterized by rapid and sometimes unpredictable rule changes.

The EV market headwinds that accelerated Panasonic’s data centre pivot also present a structural uncertainty for the broader battery supply chain. If the global EV recovery proves slower than anticipated, some of the supply chain capacity built in anticipation of EV demand may need to be repurposed — a transition that is technically feasible but operationally complex.

Nevertheless, the convergence of AI infrastructure demand, renewable integration needs, and energy security imperatives appears robust enough to sustain a multi-year growth cycle for Japan’s battery sector. The 60 Nikkei 225 companies charted above are not passive observers of this trend — they are active builders of the infrastructure that will define Japan’s energy economy for the next two decades.

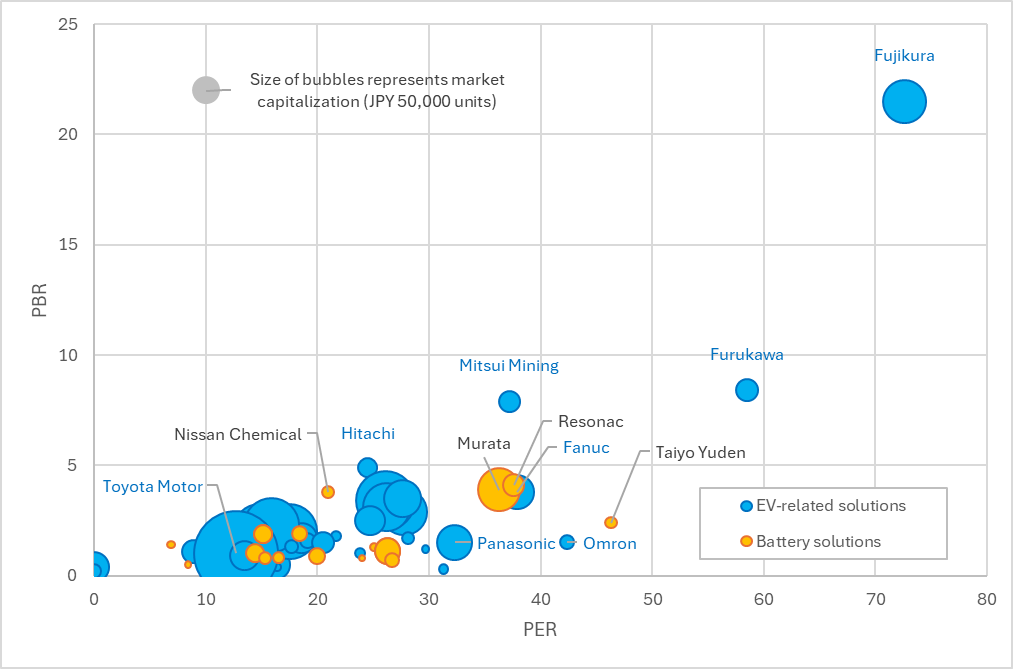

Valuation Map: PER vs. PBR with Market Capitalization

Data as of May 15, 2026. PER (Price Earnings Ratio) indicates how many times a company’s earnings are reflected in its share price. PBR (Price Book-value Ratio) represents how many times a company’s net assets are reflected in its share price. Bubble size represents market capitalization.

References

[FN1] Panasonic Q1 FY2026 earnings data and CES 2026 product disclosures: Panasonic Newsroom Global, “Empowering AI Stability at Scale: Energy Storage Systems for Data Centers,” March 2026; OilPrice.com, “AI Drives Surge in Panasonic’s Battery Unit Profit,” July 2025. ↩

[FN2] S1:DR, “Grid-Scale Battery Storage: Japan’s Emerging Energy Business,” April 26, 2026; Energy-Storage.News, “Japan: Electric Utilities Progress in Emerging Battery Storage Market,” May 2025. ↩

[FN3] Nikkei Asia, “Daiwa to Invest $630m in Japan Battery Storage for Chip, Data Center Power,” May 2026; Daiwa Energy & Infrastructure portfolio disclosures; Grand View Research, “Japan Battery Energy Storage Systems Market Size & Outlook, 2030,” 2026; Energy-Storage.News, “Daiwa Energy & Infrastructure Builds 160MWh BESS in Hokkaido, Japan,” October 2025. ↩