Photo by SLNC on Unsplash

Flexible thin‑film perovskite panels are set to be installed on a Maritime Self‑Defense Force barracks roof in Uruma City from summer 2026. The project will mark the first government‑run pilot of this technology, reflecting Tokyo’s interest in exploring domestic solar options to strengthen energy resilience in the defense sector.

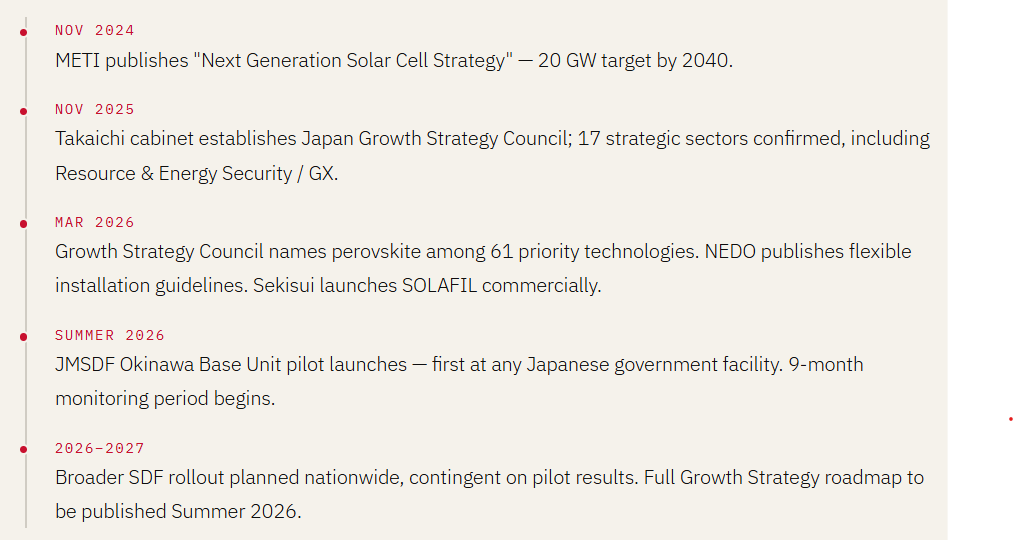

Japan’s government will deploy next-generation perovskite solar cells at Self-Defense Force installations, with the inaugural demonstration launching in Okinawa this summer. METI will place flexible, lightweight panels on the barracks roof of the JMSDF Okinawa Base Unit in Uruma City for a nine-month monitoring period — the first time perovskite technology has been tested at any Japanese national government facility.FN1

The Supplier Question: Most Likely Sekisui Chemical — But Not Confirmed

The Nikkei report does not name the panel manufacturer for the JMSDF pilot. However, context strongly points to Sekisui Chemical as the most probable supplier. The company launched commercial sales of its film-type perovskite product — branded SOLAFIL — in March 2026, making it the only Japanese manufacturer with a commercially available flexible perovskite product at the time of the pilot’s announcement.FN2 Sekisui has also run the most extensive field demonstration program in Japan, conducting pilots at naval-adjacent coastal environments — including a typhoon and salt-exposure study in Miyako Island, Okinawa, in partnership with Okinawa Electric Power — that directly parallel the conditions at the Uruma City site.FN3

Other active Japanese manufacturers include Panasonic (glass-type, BIPV-oriented; trial sales from 2026) and Ricoh (which supplied cells for JAXA’s HTV-X1 spacecraft and has deployed garden-lighting installations at Tokyo Metropolitan Government facilities in March 2026). Neither has announced a flexible rooftop product at the scale or commercial stage required for this pilot.FN4 Until an official announcement names the supplier, the manufacturer should be treated as unconfirmed.

Why Okinawa? Why Now?

The location is strategically deliberate. Okinawa anchors Japan’s southwestern island chain and carries a disproportionate military footprint. Its subtropical climate — intense UV, typhoon-season winds, salt air, and high humidity — makes it a demanding durability test and the most operationally relevant environment for evaluating distributed energy generation at forward-deployed bases. Energy supply to these islands has long been identified as a contingency vulnerability; as Japan’s defense posture in the region expands, that vulnerability sharpens.FN5

Why Perovskite?

Unlike silicon panels, perovskite cells are thin, flexible, and light enough for curved or structurally weak surfaces — aged barracks roofs, vehicle canopies, portable shelters. For defense logistics, that means rapid deployment and integration into mobile infrastructure where conventional panels cannot go. The technology also advances Japan’s goal of reducing dependence on Chinese-dominated silicon supply chains, which account for roughly 80% of global solar panel production.FN6 Japan’s domestic iodine reserves — approximately 30% of world supply and a key perovskite feedstock — make a domestically secure supply chain achievable in a way silicon never allowed.FN7

“Energy independence at the facility level is an operational requirement, not an environmental aspiration.”

Context: Japan’s 17 Strategic Growth Sectors

The JMSDF Okinawa pilot is not an isolated initiative — it sits at the intersection of two of Japan’s highest-priority policy frameworks. Under Prime Minister Sanae Takaichi’s growth strategy, established in November 2025, the Japan Growth Strategy Council designated 17 strategic sectors for concentrated official and private investment, pairing “crisis management investment” with long-term “growth investment.”FN8 Perovskite solar cells fall under Sector ⑨: Resource & Energy Security / GX (Green Transformation), and were formally included in the Council’s roster of 61 priority products and technologies decided at its March 10, 2026 session.FN9

The perovskite pilot thus serves double duty: it generates demand-side data for METI’s industrial roadmap while simultaneously supplying defense infrastructure with on-site renewable generation. Crucially, the initiative also links Sector ⑨ to Sector ⑮ (Defense Industry), with the Cabinet Office explicitly designating “defense procurement including government agency purchases” as a mechanism for stimulating early-phase demand across all 17 sectors.FN10

Policy and Industrial Backdrop

METI’s “Next Generation Solar Cell Strategy” (November 2024) targets 20 GW of perovskite capacity by 2040.FN11 The ¥2 trillion Green Innovation Fund backs leading manufacturers: Sekisui Chemical targets 100 MW of roll-to-roll production capacity by April 2027; Panasonic is preparing a 2026 trial commercial release. The Ministry of Environment launched dedicated subsidy programs in September 2025, and NEDO published updated installation guidelines in March 2026.FN12

Risks

Durability is the central unknown. Laboratory single-junction cells have exceeded 26.7% efficiency and perovskite/silicon tandem cells have reached 34.6%, but sustained performance under Okinawa’s harsh field conditions — UV, salt, humidity, typhoon winds — is unproven at this scale.FN13 Critics at IEEFA have questioned whether Japan’s commercial timeline is realistic, noting that current generation efficiency per unit of investment still trails conventional panels.FN14 Nine months is also a short baseline for drawing conclusions about long-term degradation in military-grade applications.

The Iodine Supply Chain: Two Companies Worth Watching

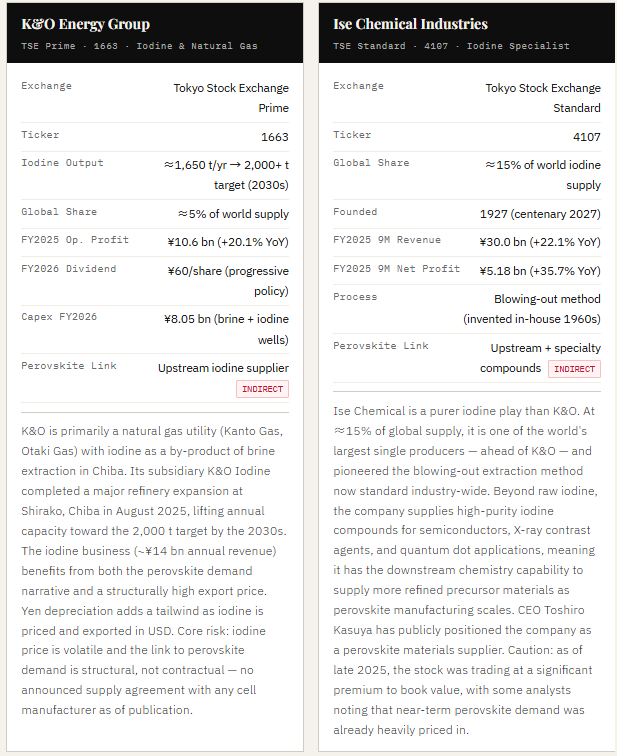

Any discussion of Japan’s perovskite ambitions eventually arrives at the same chokepoint: iodine. The element is the principal feedstock distinguishing perovskite cells from silicon ones — and Japan’s dominance of global iodine supply is the structural reason this technology gives Tokyo a genuine shot at supply-chain independence. Two listed companies sit at the center of that advantage, both rooted in the same geology: the brine-bearing natural gas fields beneath Chiba Prefecture.

Both companies extract iodine from the same geological formation: ancient seawater locked in brine deposits beneath the South Kanto gas fields, concentrated in Chiba Prefecture, which alone accounts for roughly 80% of Japan’s domestic iodine output.FN15 Neither has announced a direct supply contract with a perovskite cell manufacturer, and both should be understood as upstream commodity suppliers whose fortunes are tied to iodine price, yen/dollar dynamics, and the long-run trajectory of perovskite adoption — not to any specific program or pilot.FN16 The JMSDF pilot does not directly affect either company’s near-term earnings. What it does do is validate, in a high-visibility defense context, the strategic importance of the feedstock both companies produce.

Conclusions

The JMSDF Okinawa pilot is the opening move in a longer strategic play. Nine months of data from a single barracks roof will not transform Japan’s defense energy posture — but it sets a precedent: perovskite technology is now inside the defense procurement ecosystem, with a clear pathway to broader deployment across the island chain running southwest toward Taiwan.

What makes this moment significant is the policy architecture behind it. The pilot is not a standalone experiment — it is a deliberate instrument of the 17-sector growth strategy, designed to create government-anchored demand that de-risks private investment in a technology where Japan holds genuine material and scientific advantages. The linkage of Sector ⑨ (Energy/GX) and Sector ⑮ (Defense Industry) through a single procurement action is precisely the kind of cross-sector leverage the Takaichi government designed the Growth Strategy Council to generate.

If Sekisui’s SOLAFIL — or whichever supplier is ultimately named — survives Okinawa’s climate, the case for full-scale SDF rollout becomes compelling. Watch the pilot results and the Summer 2026 roadmap publication: together, they will determine whether this is an industrial turning point or a well-intentioned footnote.

References & Sources

FN1 Nikkei Shimbun, 「自衛隊基地にペロブスカイト太陽電池 需要創出へ政府施設の活用拡大」, May 19, 2026. METIによると、日本の国の行政機関施設として初のペロブスカイト実証。期間は9カ月。

FN2 Sekisui Chemical, 「フィルム型ペロブスカイト太陽電池『SOLAFIL』事業開始のお知らせ」, March 27, 2026. 日本初の商用フレキシブル型ペロブスカイト製品。発売当初は企業・自治体向け。FY2027に100 MWラインを目標。

FN3 Sekisui Chemical / Okinawa Electric Power / Unitika 共同発表, April 16, 2025。Nikkei Shimbun 同日報道。 宮古市での台風・塩害環境下の実証は2026年3月まで継続。静岡(清水港)での沿岸塩害実証も2025年4月から実施。

FN4 Panasonic Holdings プレスリリース, March 2, 2026(ガラスタイプBIPV実証)。 Ricoh プレスリリース, October 2025(HTV‑X1軌道上実証)および March 2026(東京都庁・お台場でのガーデンライト41基設置)。 いずれもJMSDFの屋根要件に合致するフレキシブル型ではない。JMSDF実証の供給企業は公表前。

FN5 Japan Cabinet Secretariat, National Security Strategy, December 2022。 南西諸島の自衛隊施設におけるエネルギー・レジリエンスが脆弱性として明記。

FN6 METI, Next Generation Solar Cell Strategy, November 2024。 シリコン太陽電池製造の中国依存(世界シェア約80%)を戦略的課題として指摘。

FN7 Energy Tracker Asia, 「Perovskite Solar Cells Race: Japan’s Plan to Lead」, 2025。 日本のヨウ素生産は世界の約30%(チリ約60%、日本は第2位)。中国依存を避けうる主要原料。

FN8 Japan Growth Strategy Headquarters, Cabinet Decision, November 4, 2025。 2025年11月10日の成長戦略会議で17の戦略分野を決定。分野リストは内閣官房資料および民間分析(note.com / 第一生命経済研)で確認。

FN9 Smart Grid Forum / Impress, 「ペロブスカイトに政府が重点投資、成長戦略会議で決定」, March 23, 2026。 2026年3月10日の成長戦略会議で、次世代太陽電池(ペロブスカイト中心)が61の重点製品群の一つとして明記。環境省資料(March 30, 2026)も同旨を確認。

FN10 Cabinet Office, Japan Growth Strategy Council Explanatory Material, April 2026。 「防衛調達を含む官公庁調達」が17分野共通の供給側支援策として位置付け。

FN11 METI, Next Generation Solar Cell Strategy, November 2024。 2040年に20 GW(原発20基相当)を目標。補助金はFY2025開始。2030年度のコスト目標は14円/kWh以下。

FN12 PV Magazine International, 「Japan Reopens NEDO Perovskite Solar Call with Single-Junction Focus」, May 4, 2026。 NEDOのフレキシブル設置ガイドラインは2026年3月公表。環境省補助金は2025年9月開始。グリーンイノベーション基金総額2兆円。

FN13 NREL Efficiency Chart, October 2024。 単接合ペロブスカイトの記録効率26.7%、タンデム34.6%。 Sekisui SOLAFIL仕様:効率15.0%(ロール・ツー・ロール、30 cm幅)、耐候性10年相当(大規模独立検証は未実施)。

FN14 IEEFA, 「Japan Needs a More Nuanced Perovskite Strategy」, November 2025。

日本の2040年ロードマップのコスト前提への批判。建設業界からの投資効率に関する指摘はMETIのWG議事録にも反映。

FN15 Nikkei Shimbun, “K&OエナジーグループK&Oヨウ素、ヨウ素精製設備を増強,” August 1, 2025. Japan is the world’s No. 2 iodine producer (≈30% global share; Chile No. 1 ≈60%). Chiba Prefecture accounts for ≈80% of Japan’s domestic output. K&O iodine capacity: ≈1,650 t/yr (2025), targeting 2,000+ t by the 2030s. Ise Chemical global share: ≈15% (Jigyo Koso Online, September 2025; Nikkei CNBC interview, November 2025).

FN16 Neither K&O Energy Group (1663) nor Ise Chemical Industries (4107) has announced a direct supply agreement with Sekisui Chemical, Panasonic, or any other perovskite cell manufacturer as of May 2026. The perovskite demand thesis for both stocks is structural and speculative — dependent on the pace of commercialization — not contractual. Ise Chemical FY2025 Q1–Q3 results: Nikkei Shimbun, October 31, 2025. K&O FY2025 results and FY2026 guidance: earnings call transcript, February 2026. Valuation caution on Ise Chemical: AI Buffett Research Institute analysis, December 2025.