Photo by David Emrich on Unsplash

Three districts account for more than 60% of residential CO₂ output — and the utilities serving them will determine whether Japan meets its 2030 climate targets.

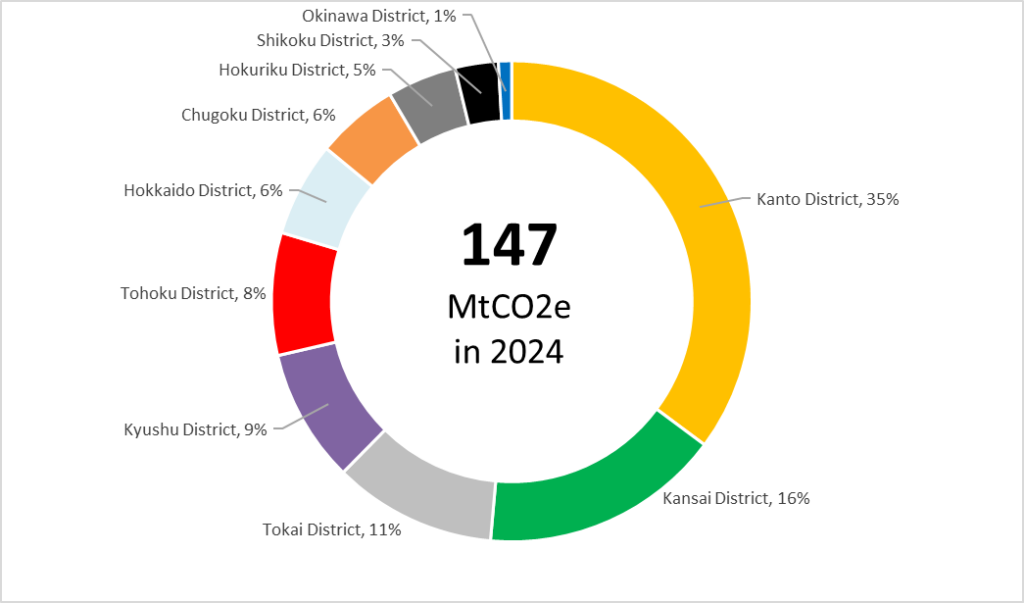

Japan’s residential sector emits approximately 147 million tonnes of CO₂ annually, representing roughly 15% of the country’s total emissions of around one billion tonnes.FN1 This figure is not evenly distributed across Japan’s ten geographic districts: the Kanto, Kansai, and Tokai districts together account for more than 60% of all residential emissions, reflecting the dense concentration of households in the greater Tokyo, Osaka–Kobe–Kyoto, and Nagoya metropolitan corridors.FN2

Concentration of Residential CO₂ Emissions Across Japan’s Districts (2024)

Sources: National Institute of Environmental Studies as of April 20th 2026.

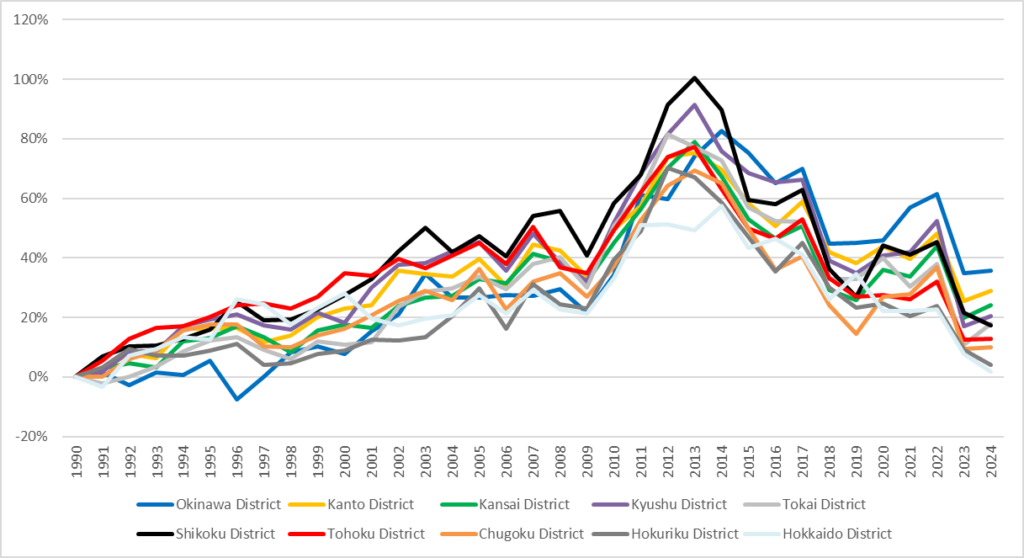

While Okinawa District has recorded the fastest proportional growth in residential emissions over the period examined, the three major districts above have also sustained significant upward trajectories, underscoring that sheer population mass continues to drive absolute emission volumes.FN3 The utilities operating in these high-concentration regions — most notably JERA, which dominates power generation in the Kanto and Tokai areas, and Kansai Electric Power (KEPCO), which serves the Kansai region — therefore sit at the strategic centre of any credible residential decarbonisation pathway.FN4 Their fleet transition plans, renewable energy procurement commitments, and pace of thermal asset retirement will be the primary determinants of whether electricity-driven residential emissions — from heating, cooling, and the growing penetration of heat pumps — fall at the rate the government requires.FN5

Residential CO₂ Trends by District, 1990–2024

Sources: National Institute of Environmental Studies as of April 20th 2026.

“The utilities serving Japan’s three most emissions-intensive districts are not peripheral actors — they are the critical path.”

The Japanese government has set a target of halving residential sector emissions by 2030 relative to 2013 levels.FN6 Given that emissions in the major districts showed sustained growth through to around 2013–2014 before beginning a gradual decline — a pattern visible across nearly all ten districts — the remaining reduction required is steep.FN7 Passive measures and incremental efficiency improvements will be insufficient. Accelerated decarbonization of the electricity supply serving Kanto, Kansai, and Tokai, combined with active policies to accelerate household electrification and energy efficiency retrofits, represents the most direct lever available to policymakers and investors.FN8

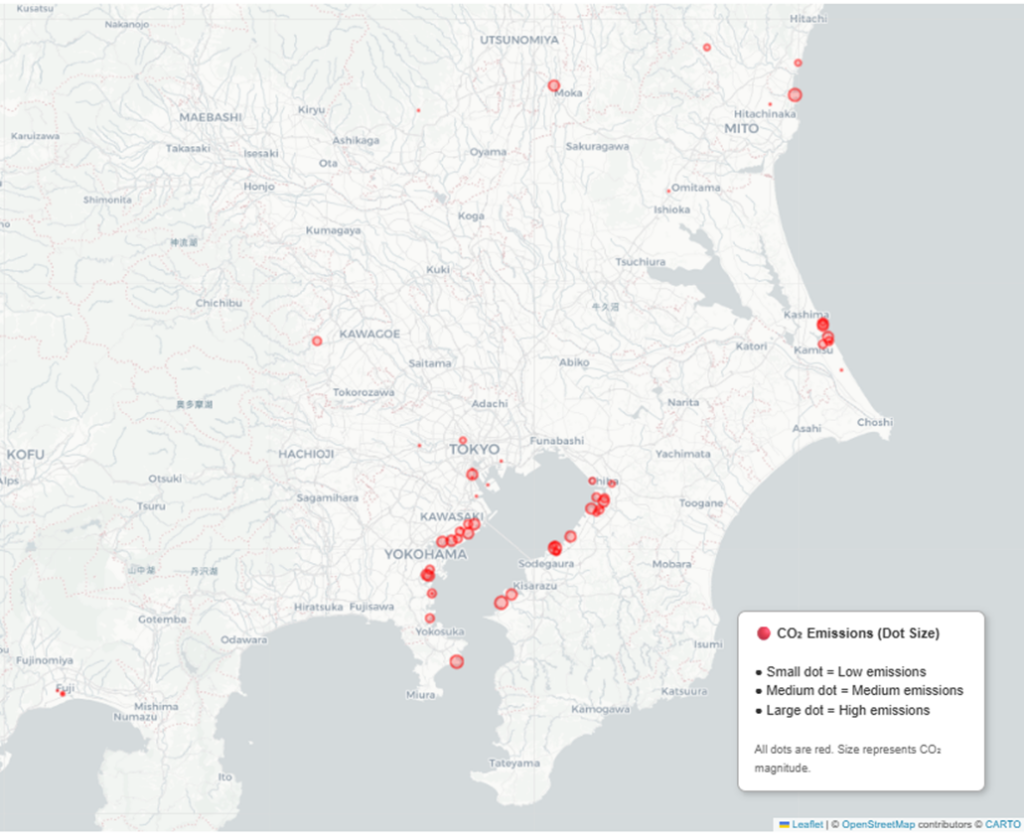

CO₂ Hotspots: Kanto

Sources: Climate Trace as of April 20th 2026.

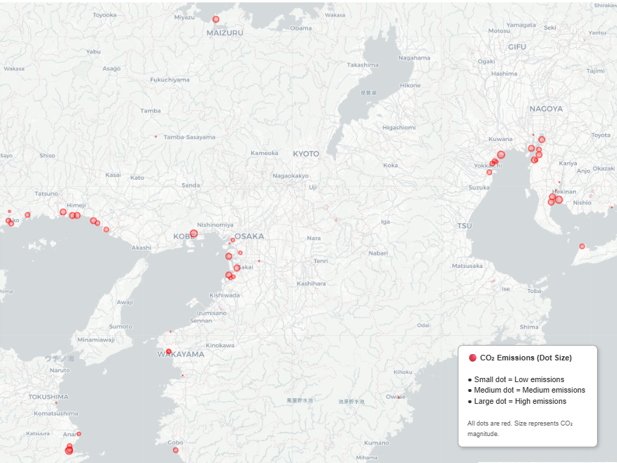

CO₂ Hotspots: Tokai and Kansai

Sources: Climate Trace as of April 20th 2026.

Conclusion

The geographic concentration of Japan’s residential emissions creates both a challenge and an opportunity: the decarbonisation problem is, to a significant degree, a problem of three districts and two dominant utilities. Investors and policymakers focused on Japan’s residential emissions pathway should direct analytical attention — and capital engagement — toward the decarbonisation strategies of JERA and Kansai Electric Power, whose grid transition timelines will either enable or foreclose Japan’s 2030 residential climate target.FN9 With the deadline now fewer than four years away, the window for course correction is narrow, and bolder, faster action from grid operators and regulators is essential.FN10

— ◆ —

日本の家庭部門の脱炭素化:地域集中という構造的課題

日本の住宅部門は年間約1億4700万トンのCO₂を排出しており、これは日本全体の約10億トンの排出量の約15%に相当する。FN1 しかし、この排出量は日本の10地区に均等に分布しているわけではない。関東・関西・東海の3地区だけで住宅部門排出量の60%超を占めており、東京圏、大阪・神戸・京都圏、名古屋圏といった大都市圏に世帯が高度に集中している構造を反映している。FN2

調査期間中、沖縄地区は住宅部門排出量の「割合ベース」で最も速い伸びを示したが、上記3大地区も絶対量として大きな増加を続けており、人口規模そのものが排出量を押し上げる主要因であることが明確である。FN3 こうした高集中地域に電力を供給する事業者、特に関東・東海で圧倒的な発電シェアを持つJERA、および関西地域を担う関西電力(KEPCO)は、住宅部門の脱炭素化における戦略的中核を占める。FN4 これらの事業者の発電所転換計画、再エネ調達方針、火力資産のリタイア速度は、暖房・冷房・ヒートポンプ普及など電化に伴う住宅部門の電力起因排出が政府の要求水準で減少できるかどうかを左右する主要因となる。FN5

「日本の3大排出地区を支える電力会社は周縁的な存在ではない。脱炭素化の“クリティカルパス”そのものである。」

日本政府は、住宅部門排出を2030年までに2013年比で半減させる目標を掲げている。FN6 しかし、主要地区の排出量は2013〜2014年頃まで増加を続け、その後ようやく緩やかな減少に転じたにすぎず、この傾向はほぼ全ての地区で共通している。FN7 残された削減幅は大きく、受動的な対策や漸進的な効率改善だけでは到底足りない。関東・関西・東海に電力を供給する系統の脱炭素化を加速させることに加え、家庭の電化と省エネ改修を積極的に推進する政策が、政策当局と投資家にとって最も直接的なレバーとなる。FN8

結論

日本の住宅部門排出は地理的に高度に集中しており、これは同時に課題であり機会でもある。脱炭素化の本質は、「3地区と2つの主要電力会社」の問題と言ってよい。 住宅部門の排出削減に関心を持つ投資家と政策当局は、JERA と関西電力の脱炭素戦略に分析・資本の両面で注目すべきである。これらの事業者の系統転換のタイムラインが、日本の2030年住宅部門目標を実現するか、あるいは不可能にするかを決定づける。FN9 2030年まで残り4年を切った今、軌道修正のための時間は限られており、系統運用者と規制当局によるより大胆で迅速な行動が不可欠である。FN10

References

FN1 — Ministry of the Environment, Japan. Greenhouse Gas Emissions Data. Residential sector aggregate, fiscal year basis. Japan’s total national emissions approximately 1.0 Gt CO₂e.

FN2 — Regional breakdown derived from district-level residential emissions data; Kanto District alone accounts for approximately 35% of residential sector totals. See accompanying pie chart.

FN3 — Time-series data 1990–2024, indexed to 1990 baseline. Okinawa shows highest proportional growth; Kanto, Kansai, and Tokai show sustained absolute growth with peaks around 2013–2014.

FN4 — JERA Co., Inc. is the largest power generation company in Japan, operating thermal plants predominantly serving the Chubu and Kanto regions. Kansai Electric Power Co. (KEPCO) is the principal utility for the Kansai region.

FN5 — Scope 2 emissions from electricity consumption represent the dominant and most tractable component of residential sector CO₂ in electrified Japanese households.

FN6 — Government of Japan. Japan’s Nationally Determined Contribution (NDC). Submitted to the UNFCCC; residential sector sub-target implies approximately 50% reduction from 2013 levels by FY2030.

FN7 — Time-series analysis indicates district-level peaks circa 2013–2014 at 60–100% above 1990 baseline; subsequent declines have been gradual and insufficient relative to target trajectory.

FN8 — IEA. Japan Energy Policy Review. Electrification of end-uses combined with grid decarbonisation identified as highest-impact residential emissions reduction pathway.

FN9 — Engagement frameworks for institutional investors: Climate Action 100+ target list includes JERA parent companies and KEPCO as systemically important emitters in the Japanese power sector.

FN10 — As of April 2026, approximately 44 months remain until the FY2030 target deadline, requiring annualised rates of reduction significantly above recent observed trends.