Photo by Markus Spiske on Unsplash

Why ARL Matters for Clean Energy Investment

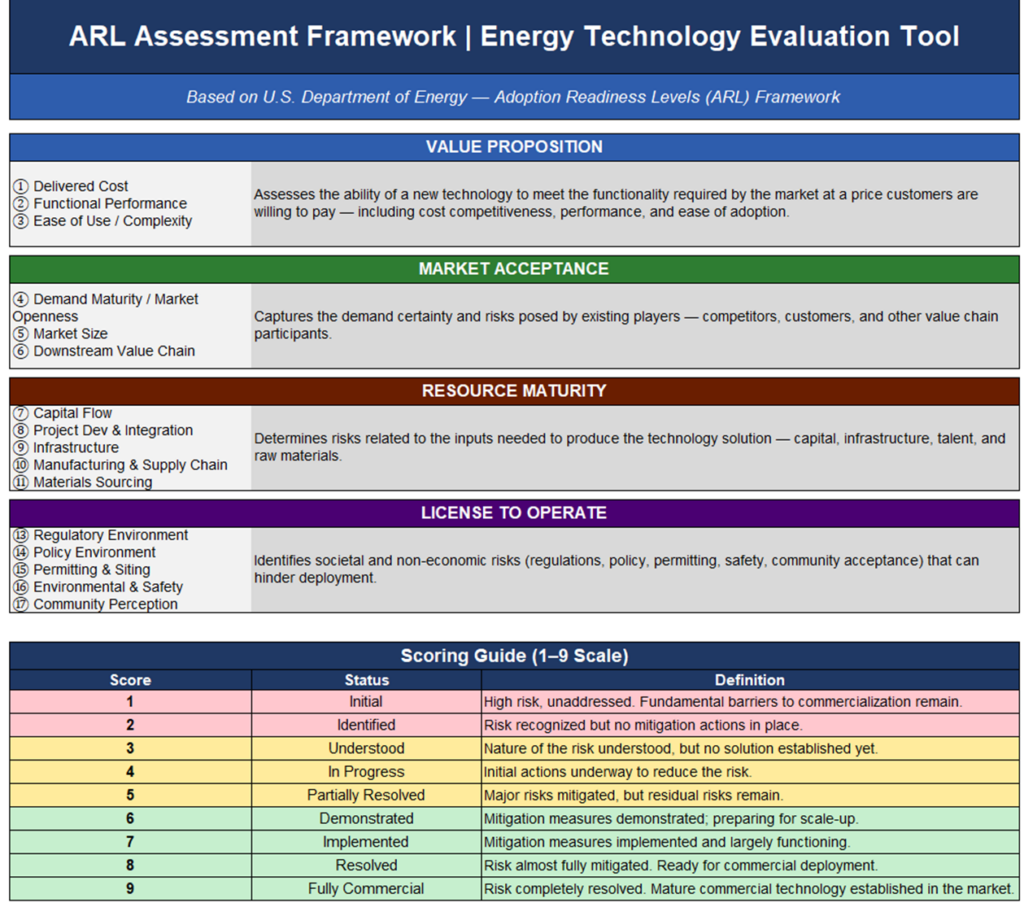

The U.S. Department of Energy’s Adoption Readiness Level (ARL) framework was developed by the Office of Technology Commercialization to address a persistent gap in technology evaluation: conventional methods focus almost exclusively on technical readiness, yet most clean energy technologies fail not in the laboratory, but in the market.FN1 The ARL framework complements the well-established Technology Readiness Level (TRL) scale by mapping commercialization risk across 17 dimensions grouped into four risk buckets.

The U.S. Department of Energy’s Adoption Readiness Level (ARL) framework

Source: US DOE as of April 20, 2026. Download ARL Guide

For investors and policymakers evaluating nascent clean technologies, ARL provides a structured, reproducible diagnostic. A technology that scores 9/9 on TRL but 2/9 on capital flow or 3/9 on supply chain maturity is not commercially ready — and capital deployed prematurely will be destroyed. The ARL score, averaged across all 17 dimensions, provides an overall commercialization readiness signal that sits alongside, but is independent of, technical performance metrics.FN2

A critical supplement to ARL — especially relevant for technologies where clean alternatives are inherently more expensive than incumbents during the transition period — is the concept of Willingness to Buy (WTB). Even if a technology is technically superior and policy-supported, commercialization is impossible without offtakers: committed buyers willing to pay a premium for the clean version. The existence, credibility, and scale of offtake agreements are therefore a key leading indicator of commercial viability that the ARL framework alone does not fully capture, but which investment analysts must evaluate in parallel.FN3

“A technology that scores 9/9 on TRL but 2/9 on supply chain is not commercially ready. The ARL framework makes these gaps visible before capital is destroyed.”

Perovskite Solar: Technology Overview and Strategic Context

Perovskite solar cells have attracted extraordinary research interest over the past decade, with certified laboratory efficiencies now exceeding 30% for perovskite-silicon tandem architectures — surpassing the practical efficiency ceiling of conventional silicon PV.FN4 The technology’s primary appeal is threefold: potential for higher efficiency, simpler and lower-cost manufacturing processes (roll-to-roll deposition), and physical properties — lightweight, flexible — that enable installation on surfaces inaccessible to conventional rigid silicon panels.

In Japan, perovskite has emerged as a national strategic technology. Japan’s Ministry of Economy, Trade and Industry (METI) has set a 2040 target of 20 GW of annual perovskite production capacity and is backing this with substantial funding through the Green Innovation Fund and the GX Supply Chain Construction Support Project.FN5 Japan’s natural iodine endowment — approximately 30% of global supply — gives domestic producers a rare materials advantage over silicon-based competitors that rely on Chinese polysilicon.FN6

At the same time, incumbent silicon PV manufacturers — led by Chinese giants LONGi Green Energy and Trina Solar — are not passive bystanders. Both companies are actively pursuing perovskite-silicon tandem R&D: LONGi achieved a 34.85% tandem cell efficiency (NREL certified) in April 2025, and Trina Solar achieved 32.6% on an industrial-format cell (Fraunhofer certified) in December 2024.FN7 This convergence means the competitive landscape for perovskite is not simply “new entrants vs. incumbents” — it is increasingly a race between pure-play perovskite producers (Sekisui Chemical, Panasonic) and silicon-dominant companies that intend to absorb perovskite technology into their existing scale advantages.

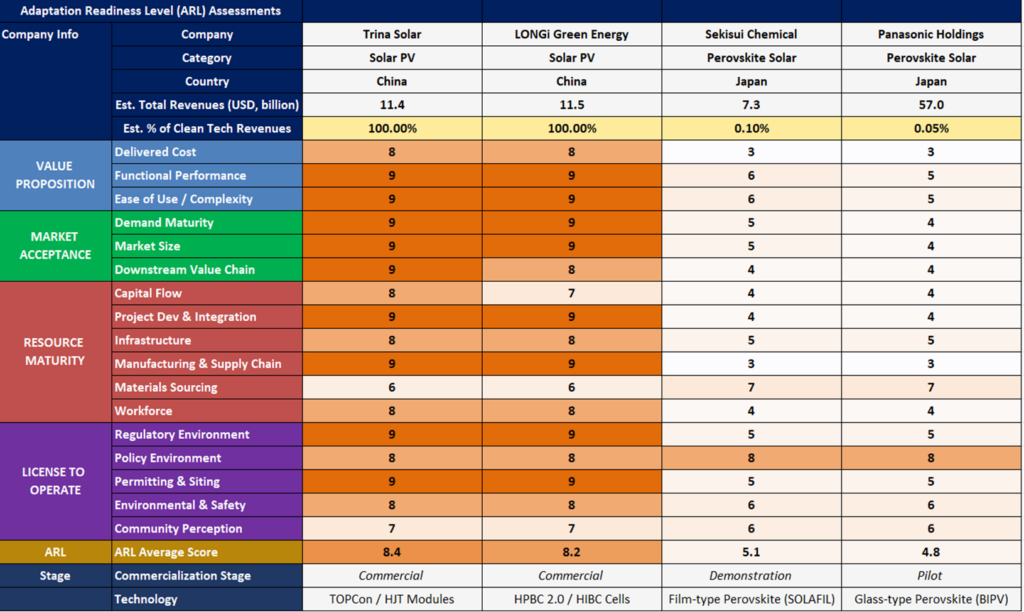

ARL Scorecard: Perovskite vs. Incumbent Silicon PV

The table below summarises ARL dimension scores for the four companies assessed. Trina Solar and LONGi Green Energy represent the incumbent silicon PV benchmark; Sekisui Chemical and Panasonic Holdings represent the leading Japanese perovskite challengers.

Perovskite vs Conventional PV: Adaptation Readiness Assessment at Company Levels

Data analyzed and estimated by SIDR and AI as of April 20, 2026. Estimated % of Clean Tech Revenues is based on AI‑generated estimates of perovskite solar cell revenues. Users should exercise caution when relying on these figures. Download data.

Dimension-by-Dimension Analysis

Cost Competitiveness (Dimension ①)

This is the most acute gap between incumbent and challenger. Silicon PV modules from Trina Solar and LONGi are priced at approximately $2.97–$3.03 per watt installed, with LCOE now reaching $30–60/MWh in optimal conditions — a level that has already displaced many fossil fuel sources on pure cost grounds.FN8 Sekisui Chemical’s SOLAFIL film-type perovskite product is currently priced at three to four times the cost of conventional silicon panels, and the company projects cost parity only after achieving 1GW of annual production scale — a milestone targeted for 2030.FN9 Panasonic’s glass-type BIPV product faces a similar cost structure. The ARL score of 3/9 on delivered cost for both perovskite producers reflects this stark reality: without offtakers willing to pay a substantial premium — whether governments, corporate sustainability commitments, or niche commercial users constrained by roof load capacity — the technology cannot yet sustain a commercial market without subsidization.

Manufacturing & Supply Chain (Dimension ⑩)

The silicon PV supply chain — from polysilicon through wafers, cells, and modules — is among the most mature and vertically integrated manufacturing ecosystems in clean energy. LONGi alone targets 120 GW of wafer output and 80–90 GW of module output in FY2025.FN10 Perovskite, by contrast, requires entirely new manufacturing processes. Sekisui Chemical is establishing a roll-to-roll film manufacturing process at its Kawasaki facility, scaling from 30 cm to 1-meter width, with 100 MW production capacity targeted for 2027.FN11 Lead content management and the establishment of a dedicated supply chain for perovskite-specific materials represent additional barriers not present in silicon PV. Scores of 3/9 for both Sekisui and Panasonic in this dimension appropriately reflect the nascency of the manufacturing base.

Materials Sourcing (Dimension ⑪) — An Unexpected Perovskite Advantage

One dimension where perovskite challengers score higher than silicon incumbents is materials sourcing. Silicon PV depends heavily on polysilicon, approximately 90% of which is produced in China, creating meaningful geopolitical concentration risk for non-Chinese manufacturers and their customers.FN12 Perovskite’s primary absorber material relies on iodine, of which Japan accounts for approximately 30% of global supply — giving Sekisui Chemical and Panasonic a rare domestic materials advantage that is strategically significant from an energy security standpoint.FN13

Policy Environment (Dimension ⑭) — Both Technologies Benefit

Importantly, both silicon PV and perovskite solar operate within a highly supportive policy environment, scoring 8/9. Global renewable energy mandates, Japan’s GX Strategy, METI’s ¥2 trillion Green Innovation Fund, and the U.S. Inflation Reduction Act’s 30% Investment Tax Credit collectively create strong tailwinds for all solar technologies.FN14 For perovskite specifically, METI’s designation of perovskite as a priority domestic technology — with a ¥157 billion subsidy commitment to Sekisui Chemical through February 2029 — provides a critical capital bridge during the pre-commercial phase.FN15

Adaptation Readiness Level (ARL) Profile — Sekisui Chemical

Data analyzed and estimated by SIDR and AI as of April 20, 2026. Users should exercise caution when relying on these figures. Download data.

Sekisui Chemical vs. Panasonic: Market Development Leadership

Within the perovskite competitive set, Sekisui Chemical has established a meaningful lead over Panasonic Holdings — not only in technical commercialization but, crucially, in market development. While both companies received METI GX subsidies and target similar BIPV/low-load-roof markets, Sekisui has moved decisively to create demand rather than waiting for it to emerge. The formal launch of the SOLAFIL product in April 2025, its deployment across five municipalities and organizations selected for METI’s FY2025 public facility pilot (including Saitama City, Shiga Prefecture, and West Nippon Expressway), and high-profile urban demonstration projects such as the Tokyo International Cruise Terminal and the Osaka headquarters exterior wall — Japan’s first perovskite installation on a building exterior — are actively building offtaker relationships and generating real-world performance data.FN16 Panasonic, meanwhile, has confirmed government funding and R&D capability, but its glass-type BIPV product remains at an earlier pilot stage with less visible market traction. Sekisui’s strategy of working directly with municipal and infrastructure offtakers — entities that are both willing to pay a premium and willing to accept early-stage technology in exchange for decarbonization credentials — is precisely the approach the WTB analysis demands.

Adaptation Readiness Level (ARL) Profile — Panasonic

Data analyzed and estimated by SIDR as of April 20, 2026. Users should exercise caution when relying on these figures. Download data.

Key Insight: Willingness to Buy & Offtaker Strategy

The most consequential near-term differentiator for perovskite commercialization is not technical efficiency — it is the cultivation of committed offtakers. Clean technologies that are inherently more expensive than incumbents require buyers willing to pay the “green premium.” Municipal governments, expressway operators, and corporate sustainability commitments represent the credible early offtaker base that can sustain volume while manufacturing costs decline toward parity. Sekisui Chemical’s demonstrated success in securing these offtake relationships — through METI pilot selection and high-profile urban deployments — represents a more advanced commercialization posture than technical readiness scores alone would suggest.FN17

Summary: Perovskite in Competitive Context

When viewed through the ARL lens, perovskite solar — as represented by Sekisui Chemical and Panasonic Holdings — trails incumbent silicon PV significantly on delivered cost competitiveness and supply chain maturity, with ARL averages of 5.1 and 4.8 respectively against 8.4 for Trina Solar and 8.2 for LONGi Green. The gap is largest in delivered cost (Dimension ①: 3 vs. 8) and manufacturing and supply chain (Dimension ⑩: 3 vs. 9), reflecting the structural reality that perovskite remains a pre-scale technology at two to four times the price of incumbent silicon PV. Both technologies enjoy equally strong policy support (Dimension ⑭: 8 for all four companies), and perovskite holds an unexpected advantage in materials sourcing (Dimension ⑪: 7 vs. 6), anchored by Japan’s domestic iodine supply. Meanwhile, the Chinese solar giants are not idle: LONGi and Trina Solar are actively developing perovskite-silicon tandem architectures that could allow them to extend their manufacturing and supply chain dominance into the next generation of solar technology, further intensifying the competitive pressure on Japan’s perovskite producers. Sekisui Chemical leads Panasonic in market development and offtaker creation — and it is this commercial progress, not merely technical advancement, that warrants close monitoring. The technology’s path to cost parity runs through scale, and scale runs through offtakers: the companies that secure committed buyers first will be best positioned to achieve the production volumes needed to drive manufacturing costs down the learning curve to eventual parity with silicon PV.FN18

Conclusion

Perovskite solar cells represent a technically compelling next-generation photovoltaic technology with certified efficiencies now exceeding 30% for tandem architectures — a level that silicon PV cannot reach alone. The DOE ARL framework reveals, however, that technical promise and commercial readiness are not synonymous. Against the incumbent silicon PV benchmark set by Trina Solar (ARL 8.4) and LONGi Green Energy (ARL 8.2), Japanese perovskite producers Sekisui Chemical (ARL 5.1) and Panasonic Holdings (ARL 4.8) face material gaps in cost competitiveness, supply chain maturity, and market penetration that cannot be closed by R&D investment alone. The most critical lever is willingness to buy: the existence of committed offtakers — particularly public-sector and infrastructure entities willing to pay the current cost premium in exchange for decarbonization and energy security benefits — determines whether manufacturing volumes can grow fast enough to drive costs down the learning curve. Sekisui Chemical has demonstrated more advanced progress on this front than Panasonic, making it the more commercially mature perovskite investment proposition at this stage. The convergence of Chinese silicon PV leaders into perovskite-silicon tandem development adds urgency: Japan’s window to establish a competitive domestic perovskite industry may be shorter than the 2030 cost-parity timeline suggests. For SIDR readers, the watchlist for this technology should include not only efficiency records and production milestones, but — above all — the accumulation of offtake commitments that signal the market’s willingness to pay for what the laboratory has already proven.FN19

Japanese translations

1. ARL評価が重要な理由

米国エネルギー省(U.S. DOE)の技術商業化局(Office of Technology Commercialization)が開発したARL(Adoption Readiness Level)フレームワークは、技術評価における長年の盲点を解消するために設計された。従来の評価手法は技術的成熟度(TRL)に偏りすぎており、クリーンエネルギー技術の多くは研究室では成功しながらも、市場で失敗するという現実があった。FN1 ARLフレームワークは、17の評価次元を4つのリスクバケットに整理し、TRLを補完する形で「商業化リスク」を体系的に可視化する。

Value Proposition(価値提案)コスト競争力・機能性能・導入の容易さ——市場が実際に支払う価格帯で機能を提供できるか?

Market Acceptance(市場受容性)需要の成熟度・市場規模・下流バリューチェーン——現実的・アクセス可能な買い手は存在するか?

Resource Maturity(資源成熟度)資本フロー・プロジェクト統合・インフラ・サプライチェーン・原材料・人材——実際に製造・スケール化できるか?

License to Operate(操業許可)規制・政策・許認可・環境安全・地域合意——社会は展開を許可するか?

投資家や政策立案者が新興クリーン技術を評価する際、ARLは再現性のある構造化された診断ツールを提供する。TRL9点でも、資本フローが2点、サプライチェーンが3点であれば商業的には未成熟であり、早期に投下した資本は毀損する。17次元の平均ARL値は、技術性能指標とは独立した「商業化準備度」の総合シグナルとなる。FN2

ARLを補完する重要な評価軸として、特にクリーンテクノロジーが移行期においてインカンバント技術より割高になる場合に不可欠なのが、Willingness to Buy(WTB:購買意欲)の概念である。技術的に優れ、政策支援があっても、プレミアムを支払ってでもクリーン版を購入するオフテイカー(買い手)の存在なしには商業化は成立しない。オフテイク契約の存在・信頼性・規模は、ARLだけでは完全に捉えられない商業的実行可能性の重要な先行指標であり、投資アナリストはARLと並行して評価する必要がある。FN3

「TRLが9点でもサプライチェーンが2点なら、その技術は商業的に未成熟である。ARLフレームワークは、資本が毀損される前にこのギャップを可視化する。」

2. ペロブスカイト太陽電池:技術概要と戦略的背景

ペロブスカイト太陽電池は過去10年間で急速な研究進展を遂げており、ペロブスカイト-シリコンタンデム構造での認証効率は30%を超え、従来型シリコン系太陽電池の実用効率上限を上回る水準に達している。FN4 この技術の主な訴求点は、より高い変換効率の可能性、ロール・ツー・ロール製膜による簡易かつ低コストな製造プロセス、そして軽量・フレキシブルという物性——従来の硬質シリコンパネルでは設置不可能な曲面・低耐荷重面への展開を可能にする特性——の三点である。

日本においてペロブスカイトは国家戦略技術に位置づけられており、METIは2040年に年産20GWの製造能力を目標として掲げ、グリーンイノベーション基金およびGXサプライチェーン構築支援事業を通じて大規模な資金支援を行っている。FN5 日本は世界のヨウ素供給量の約30%を占めており、この原材料上の優位性は、中国産ポリシリコンに依存するシリコン系競合他社に対して希少な地政学的アドバンテージをもたらしている。FN6

他方、インカンバントであるシリコン系太陽電池メーカー——LONGiグリーンエナジーとトリナ・ソーラーを筆頭とする中国勢——も傍観しているわけではない。LONGiは2025年4月にNREL認証で34.85%のタンデムセル効率を、トリナ・ソーラーは2024年12月にFraunhofer認証で産業フォーマットにおける32.6%を達成している。FN7 この収束は、競争構図が単純な「新興企業対インカンバント」ではなく、純粋なペロブスカイトメーカー(積水化学・パナソニック)と、既存の製造・サプライチェーン優位性の上にペロブスカイト技術を吸収しようとするシリコン主力企業との競争になりつつあることを示している。

3. ARL スコアカード:ペロブスカイト vs. シリコン系PV

下表は4社のARL次元別スコアをまとめたものである。トリナ・ソーラーおよびLONGiグリーンエナジーがシリコン系PVのベンチマーク、積水化学およびパナソニック ホールディングスが日本のペロブスカイト先行企業を代表する。

| ARL次元 | トリナ・ソーラー シリコンPV | LONGi シリコンPV | 積水化学 ペロブスカイト | パナソニック ペロブスカイト |

|---|---|---|---|---|

| ① – ③ VALUE PROPOSITION(価値提案) | ||||

| ① 実現コスト | 8 | 8 | 3 | 3 |

| ② 機能・性能 | 9 | 9 | 6 | 5 |

| ③ 使いやすさ/複雑性 | 9 | 9 | 6 | 5 |

| ④ – ⑥ MARKET ACCEPTANCE(市場受容性) | ||||

| ④ 需要成熟度 | 9 | 9 | 5 | 4 |

| ⑤ 市場規模 | 9 | 9 | 5 | 4 |

| ⑥ 下流バリューチェーン | 9 | 8 | 4 | 4 |

| ⑦ – ⑫ RESOURCE MATURITY(資源成熟度) | ||||

| ⑦ 資本フロー | 8 | 7 | 4 | 4 |

| ⑧ PJ開発・統合管理 | 9 | 9 | 4 | 4 |

| ⑨ インフラ | 8 | 8 | 5 | 5 |

| ⑩ 製造・サプライチェーン | 9 | 9 | 3 | 3 |

| ⑪ 原材料調達 | 6 | 6 | 7 | 7 |

| ⑫ 労働力・人材 | 8 | 8 | 4 | 4 |

| ⑬ – ⑰ LICENSE TO OPERATE(操業許可) | ||||

| ⑬ 規制環境 | 9 | 9 | 5 | 5 |

| ⑭ 政策環境 | 8 | 8 | 8 | 8 |

| ⑮ 許認可・立地 | 9 | 9 | 5 | 5 |

| ⑯ 環境・安全 | 8 | 8 | 6 | 6 |

| ⑰ コミュニティ認知 | 7 | 7 | 6 | 6 |

| ARL平均スコア | 8.4 | 8.2 | 5.1 | 4.8 |

| 商業化ステージ | Commercial | Commercial | Demonstration | Pilot |

4. 次元別分析

コスト競争力(次元①)

インカンバントとチャレンジャーの間で最も顕著な差が生じているのがこの次元である。トリナ・ソーラーおよびLONGiのシリコン系モジュールは設置込みで約2.97〜3.03ドル/Wで提供されており、最適条件下でのLCOEはすでに30〜60ドル/MWhに達し、多くの化石燃料電源を純コストの面で駆逐している水準にある。FN8 一方、積水化学のSOLAFILフィルム型ペロブスカイトは現状で従来型シリコンパネルの3〜4倍の価格帯にあり、コストパリティの達成には年産1GWというスケールが必要とされ、それが実現されるのは2030年の見込みである。FN9 パナソニックのガラス型BIPVも同様のコスト構造にある。両社のARLスコア3点(満点9点)は、この厳しい現実を適切に反映している。

製造・サプライチェーン(次元⑩)

シリコン系PVのサプライチェーンは、クリーンエネルギー分野で最も成熟した垂直統合型製造エコシステムの一つである。LONGi単独で、2025年度に120GWのウェハ出荷と80〜90GWのモジュール出荷を目標としている。FN10 ペロブスカイトは対照的に、全く新しい製造プロセスを必要とする。積水化学は川崎の施設でロール・ツー・ロール製膜を確立中であり、幅30cmから1mへのスケールアップを進め、2027年に100MWの生産能力達成を目指している。FN11

原材料調達(次元⑪)——ペロブスカイトの意外な優位性

ペロブスカイトのチャレンジャー企業がシリコン系インカンバントを上回る次元が原材料調達である。シリコン系PVは約90%が中国産のポリシリコンに依存しており、非中国メーカーとその顧客にとって地政学的集中リスクを生じさせている。FN12 ペロブスカイトの主要吸収材はヨウ素に依存しており、日本は世界供給量の約30%を占めている——積水化学とパナソニックにとって、エネルギー安全保障の観点から戦略的に重要な原材料上の国内優位性をもたらしている。FN13

政策環境(次元⑭)——双方に好意的

重要な点として、シリコン系PVとペロブスカイト太陽光は共に非常に支持的な政策環境(8点/9点)に置かれている。グローバルな再生可能エネルギー義務化、日本のGX戦略、METIの2兆円グリーンイノベーション基金、そして米国IRAの30%投資税額控除が、あらゆる太陽光技術に強い追い風をもたらしている。FN14 ペロブスカイトについては特に、積水化学への2029年2月までの1,570億円の補助金コミットメントが、商業化前段階における重要な資本ブリッジとなっている。FN15

5. 積水化学 vs. パナソニック:市場開拓のリーダーシップ

ペロブスカイトの競合内では、積水化学がパナソニック ホールディングスに対して技術の商業化のみならず、とりわけ市場開拓の面で明確なリードを確立している。両社はMETI GX補助金を受け、類似のBIPV・低耐荷重屋根市場をターゲットとしているが、積水化学は需要の到来を待つのではなく、能動的に需要を創出する戦略を実行している。2025年4月のSOLAFIL製品の正式ローンチ、METI FY2025年度の公共施設パイロット事業(さいたま市、滋賀県、西日本高速道路等、5組織が選定)への展開、そして東京国際クルーズターミナルや大阪本社外壁——日本初の建物外壁へのペロブスカイト設置事例——などの高視認性都市部実証プロジェクトは、オフテイカーとの関係を積極的に構築し、実世界での性能データを蓄積しつつある。FN16 パナソニックは政府資金と研究開発能力を確保しているものの、ガラス型BIPV製品は市場開拓の可視性という点でより早期のパイロット段階にとどまっている。

Key Insight:Willingness to Buy(WTB)とオフテイカー戦略

ペロブスカイト商業化における最も重要な近期の差別化要因は技術的効率ではなく、コミットされたオフテイカーの確保である。インカンバント技術より本質的に高価なクリーンテクノロジーは、グリーンプレミアムを支払う意欲のある買い手を必要とする。地方自治体、高速道路事業者、企業のサステナビリティ・コミットメントは、製造コストがパリティに向かって低下する間の生産量を維持できる信頼性の高い初期オフテイカー層を形成する。METIパイロット選定と高視認性都市部展開を通じてこれらのオフテイク関係を確保した積水化学の実績は、技術的成熟度スコアが示す以上に進んだ商業化態勢を表している。FN17

6. 総括:競争文脈の中のペロブスカイト

ペロブスカイト太陽電池——積水化学(ARL 5.1)とパナソニック(ARL 4.8)が代表する——は、ARLレンズを通じて見ると、インカンバントのシリコン系PV(トリナ:8.4、LONGi:8.2)に対してコスト競争力とサプライチェーン成熟度で大きく劣後している。この格差はコスト(次元①:3 vs. 8)と製造・サプライチェーン(次元⑩:3 vs. 9)で最も大きく、ペロブスカイトがいまなお製造スケール前の段階にあり、インカンバント比2〜4倍の価格水準にあるという構造的現実を反映している。政策支援は双方に等しく好意的(次元⑭:全4社で8点)であり、ペロブスカイトは原材料調達(次元⑪:7 vs. 6)で予想外の優位性を持つ。一方、中国のシリコン系太陽光大手も座視してはおらず、LONGiとトリナ・ソーラーはペロブスカイト-シリコンタンデムの開発を積極的に進めており、既存の製造・サプライチェーン優位性を次世代技術へと拡張しようとしており、日本のペロブスカイトメーカーへの競争圧力をさらに高めている。積水化学は市場開拓とオフテイカー獲得でパナソニックをリードしており、技術の進展だけでなく、市場開拓といった観点からもこの技術を継続的に注目していく必要がある。コスト・パリティへの道はスケールを通り、スケールはオフテイカーを通る——最初に確固たる買い手を確保した企業が、学習曲線を下り切ってシリコン系PVとのコスト均衡を達成するうえで最も有利なポジションに立つことになる。FN18

結論

ペロブスカイト太陽電池は、タンデム構造での認証効率が30%を超えという技術的に説得力のある次世代太陽光技術であり、シリコン系PV単独では到達できない効率水準を実現している。しかしDOE ARLフレームワークは、技術的可能性と商業的準備度が同義ではないことを明示している。トリナ・ソーラー(ARL 8.4)・LONGiグリーンエナジー(ARL 8.2)が示すインカンバントベンチマークに対し、積水化学(ARL 5.1)・パナソニック(ARL 4.8)はコスト競争力、サプライチェーン成熟度、市場浸透において、R&Dへの追加投資だけでは埋められない実質的な差を抱えている。最も重要なレバーはWillingness to Buyである——特に公共部門やインフラ関連の主体のように、脱炭素化とエネルギー安全保障の便益と引き換えに現状のコストプレミアムを支払う意欲のあるオフテイカーの存在が、製造量を学習曲線に沿って加速させる上での決定的要因となる。積水化学はこの点でパナソニックより進んだ姿勢を示しており、現時点ではより商業的成熟度の高いペロブスカイト投資対象と評価できる。中国の太陽光大手がペロブスカイト-シリコンタンデム開発に参入してきていることは、日本が競争力ある国内ペロブスカイト産業を確立するための時間的余裕が、2030年のコストパリティ目標が示唆する以上に短い可能性を示唆する。SIDRの読者にとって、この技術のウォッチリストに含めるべき事項は、効率記録や生産マイルストーンだけでなく——何よりも——市場が研究室で証明済みのものへの支払い意欲を示すオフテイク・コミットメントの蓄積である。FN19

References

FN1 U.S. Department of Energy, Office of Technology Commercialization. Adoption Readiness Levels (ARL) Framework. Washington D.C.: DOE, 2024.

FN2 U.S. Department of Energy, Office of Technology Commercialization. Core Risk Areas: ARL Framework Methodology. Washington D.C.: DOE, 2024.

FN3 Hydrogen Council. Green Premium Economics and Offtake Analysis. Brussels: Hydrogen Council, 2023. BloombergNEF. Clean Tech Offtake Market Analysis. London: BloombergNEF, 2024.

FN4 Trina Solar Press Release. “Trina Solar posts new milestones for tandem efficiency, module power.” pv‑magazine, December 24, 2024. LONGi Green Energy. “LONGi achieves 34.85% perovskite‑silicon tandem efficiency.” NREL certified, April 2025.

FN5 Ministry of Economy, Trade and Industry (METI). Support Project for the Introduction of Perovskite Solar Cell Social Implementation Models, FY2025. Tokyo: METI, 2025. Japan Renewable Energy Institute. Perovskite Solar Cell Policy Roadmap. Tokyo, 2024.

FN6 Sekisui Chemical Co., Ltd. Perovskite Solar Cell Business — Investor Presentation. January 7, 2025. METI. Critical Minerals and Domestic Supply Report. Tokyo: METI, 2024.

FN7 LONGi Green Energy. “LONGi achieves certified power conversion efficiency of 34.85% for perovskite–silicon tandem solar cell.” NREL certification, April 2025. Shaw, V. “Trina Solar posts milestones for tandem efficiency, module power.” pv‑magazine International, December 24, 2024.

FN8 SolarReviews. Best Solar Panel Brands 2025: Expert Reviews & Rankings. September 2025. BloombergNEF. LCOE Benchmark H2 2024. London: BloombergNEF, 2024.

FN9 RatedPower. “The rise of ultra‑thin perovskite solar cells.” September 30, 2025. Sekisui Chemical Co., Ltd. Investor Presentation, January 2025.

FN10 LONGi Green Energy Technology Co., Ltd. 2024 Annual Report: BC Tech Deployment Accelerates Across Industry. Xi’an: LONGi, April 29, 2025.

FN11 Bellini, E. “Sekisui Chemical invests in 100 MW perovskite solar production line.” pv‑magazine International, December 27, 2024.

FN12 International Energy Agency (IEA). Solar PV Global Supply Chains. Paris: IEA, 2022. BloombergNEF. China Polysilicon and Solar Supply Chain Report. London: BloombergNEF, 2024.

FN13 Sekisui Chemical Co., Ltd. Investor Presentation, January 2025. Ministry of Economy, Trade and Industry (METI). Critical Minerals Policy and Domestic Supply Report. Tokyo: METI, 2024.

FN14 Ministry of Economy, Trade and Industry (METI). Green Innovation Fund Overview and Project Portfolio. Tokyo: METI, 2024. U.S. Treasury Department. Guidance on Section 48 Investment Tax Credit under the Inflation Reduction Act. Washington D.C.: U.S. Treasury, 2023.

FN15 Bellini, E. “Sekisui Chemical to build 100MW perovskite solar cell factory.” pv‑tech, January 6, 2025.

FN16 Perovskite‑Info. “SEKISUI CHEMICAL and SSF launch ‘SOLAFIL’ film‑type perovskite solar cells.” April 2025. Sekisui Chemical Co., Ltd. “Japan’s Largest‑scale Verification of Film‑type Perovskite Solar Cells at a Port Facility.” Press release, May 24, 2024.

FN17 Sekisui Chemical Co., Ltd. METI FY2025 pilot adoption press release. April 2025. RatedPower. “The rise of ultra‑thin perovskite solar cells — commercial analysis.” September 2025.

FN18 BloombergNEF. Solar Energy Technology Learning Curves and Long‑Run Cost Trajectories. London: BloombergNEF, 2024. International Energy Agency (IEA). Perovskite Solar Cells: Technology and Commercialization Status. Paris: IEA, 2025.

FN19 U.S. Department of Energy. ARL Framework, 2024. Sekisui Chemical Co., Ltd. Investor Presentation, 2025. LONGi Green Energy. 2024 Annual Report, April 2025. Various pv‑magazine reports, 2024–2025.