Introduction

While the global hydrogen market remains modest in scale relative to conventional fossil fuel and electricity systems, the past decade has seen a marked acceleration in technological progress across production, storage, transport, and end‑use applications.FN1 Commercialization has advanced most rapidly in industrial sectors where hydrogen is already embedded within core operations—refining, ammonia, chemicals, steelmaking, and large‑scale manufacturing—because these value chains possess pre‑existing infrastructure, established customer demand, and well‑defined performance requirements.FN2 In such settings, hydrogen technologies exhibit substantially higher commercial adaptability: firms are not required to cultivate entirely new markets but instead compete on cost, operational efficiency, and supply reliability within mature industrial ecosystems.FN3 This stands in contrast to emerging mobility and power‑generation applications, where infrastructure build‑out, customer acceptance, and long‑term economics remain considerably more uncertain.FN1

Using the U.S. Department of Energy’s Adoption Readiness Level (ARL) framework, we assessed 23 leading companies positioned for high commercial adaptability across the hydrogen value chain, spanning industrial hydrogen production, mobility, infrastructure, storage and transport, and hydrogen‑based power generation.FN1

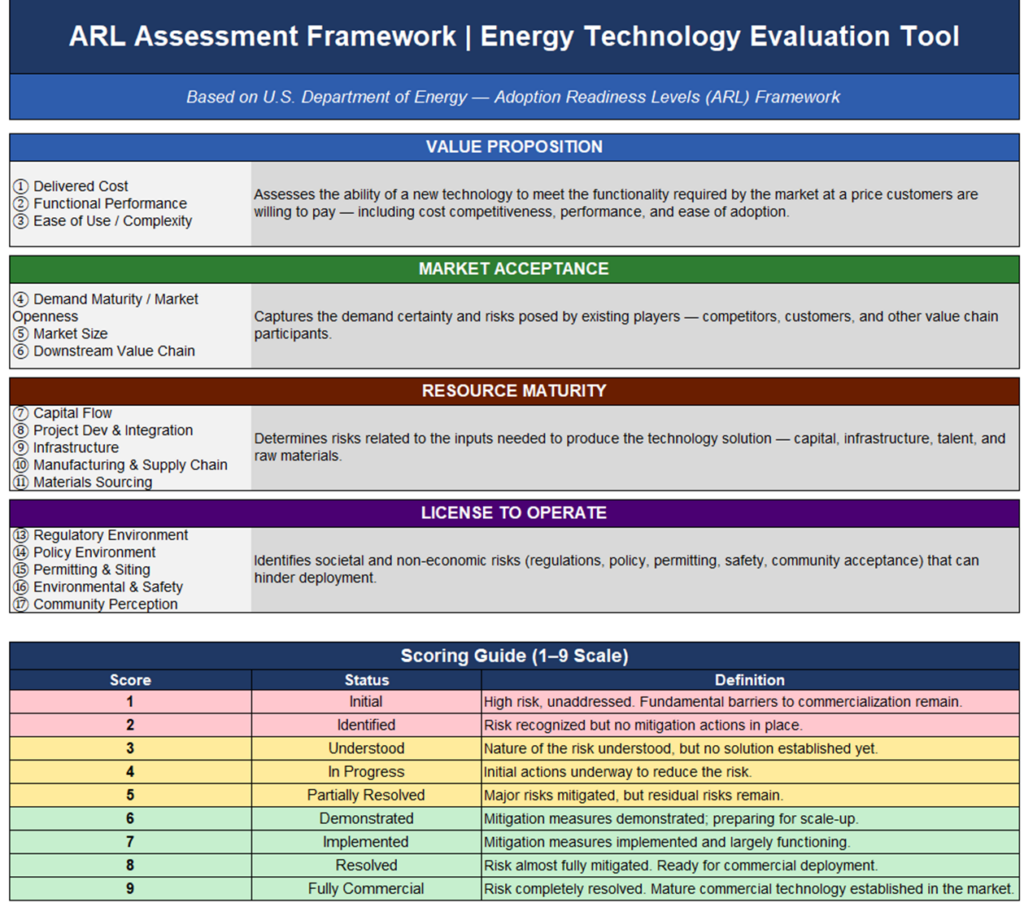

The U.S. Department of Energy’s Adoption Readiness Level (ARL) framework

Source: US DOE as of April 20, 2026. Download ARL Guide

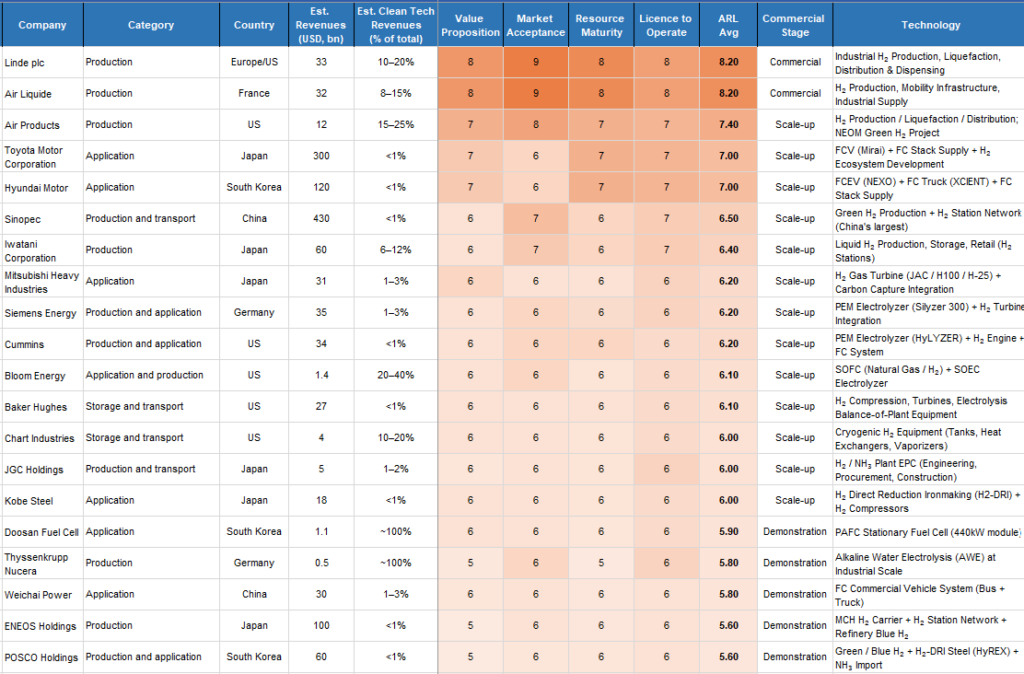

The expanded evidence‑based scorecard shows that industrial incumbents—Linde, Air Liquide, and Air Products—maintain the highest ARL scores (8.2–8.2), supported by mature infrastructure, strong functional performance, competitive delivered hydrogen costs, and deeply integrated downstream networks.FN2 Their leadership reflects the structural advantage of operating within industrial gas systems where hydrogen is already indispensable to refining, chemicals, steel, and large‑scale manufacturing.FN2 Companies such as Iwatani, Kawasaki Heavy Industries, and Chart Industries reinforce this pattern by demonstrating advanced readiness in liquid hydrogen logistics, cryogenic storage, and terminal infrastructure—highlighting that commercialization hinges as much on supply‑chain execution as on production technology itself.FN3

ARL Scorecard of Leading Hydrogen Companies Across the Value Chain

Data analyzed and estimated by SIDR and AI as of April 20, 2026. Estimated % of Clean Tech Revenues is based on AI‑generated estimates of perovskite solar cell revenues. Users should exercise caution when relying on these figures. Download data.

In hydrogen mobility, Toyota, Hyundai, and Doosan Fuel Cell exhibit comparatively strong scale‑up potential through FCEVs, heavy‑duty trucks, buses, and stationary fuel‑cell systems. Their progress is supported by engineering depth and policy alignment; however, ARL evidence indicates that delivered hydrogen cost remains the dominant commercial constraint.FN2 Relative to battery‑electric vehicles and internal‑combustion fleets, hydrogen mobility continues to face challenges in fuel economics, refueling‑station density, and customer adoption timing.FN3

In the power generation and heavy industrial sectors, Mitsubishi Heavy Industries and Kawasaki Heavy Industries illustrate two fundamentally distinct transition pathways. Mitsubishi Heavy Industries (ARL 6.2) benefits from its development of hydrogen‑compatible gas turbines, where dual‑fuel LNG–hydrogen combustion provides utilities with a pragmatic decarbonization trajectory that avoids immediate stranded‑asset exposure.FN2 This technological flexibility enhances near‑term bankability by enabling partial preservation of existing LNG infrastructure while incrementally integrating hydrogen into established operational frameworks.

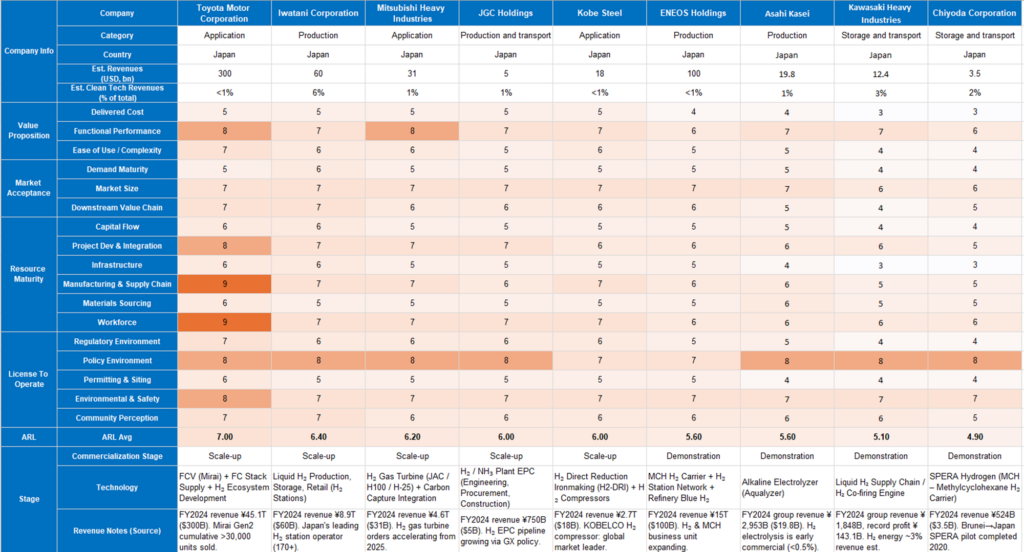

Japan’s Hydrogen Commercialization Landscape: ARL Benchmarking of Leading Industrial Players

Data analyzed and estimated by SIDR as of April 20, 2026. Estimated % of Clean Tech Revenues is based on AI‑generated estimates of perovskite solar cell revenues. Users should exercise caution when relying on these figures. Download data.

Kawasaki Heavy Industries (ARL 5.1), by contrast, is advancing a complementary but structurally different model centered on liquid hydrogen shipping, cryogenic storage systems, and terminal infrastructure. Its commercialization remains at the demonstration stage, yet its long‑term strategic significance is substantial, as the viability of international hydrogen trade will depend heavily on transport economics, maritime logistics, and import‑terminal readiness.FN3 JGC Holdings contributes to deployment through EPC integration across hydrogen projects, while Kobe Steel is progressing hydrogen‑based direct reduced iron (H₂‑DRI) technologies that underpin industrial decarbonization in steelmaking. Collectively, these cases demonstrate that hydrogen commercialization in Japan is most effective when hydrogen enhances existing industrial systems rather than attempting wholesale substitution.FN1

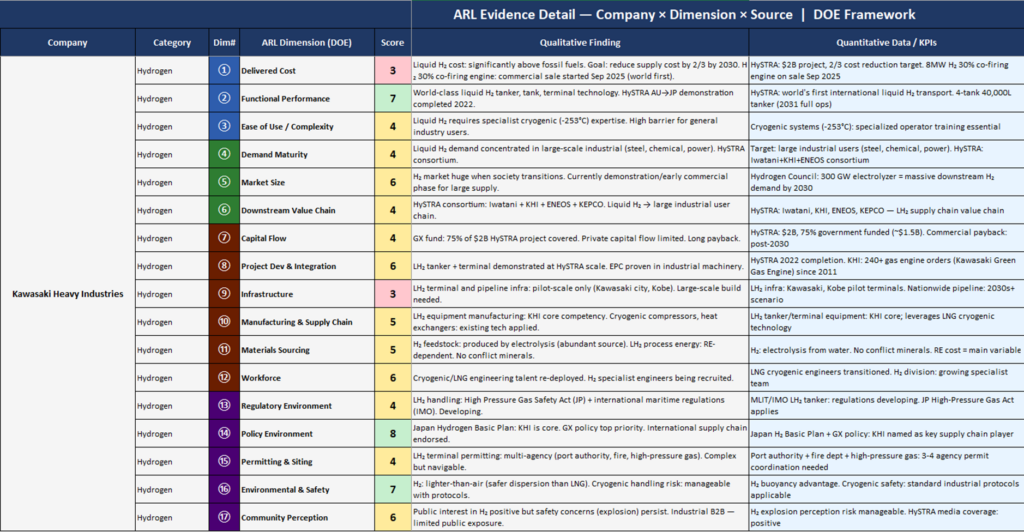

Adaptation Readiness Level (ARL) Profile — Kawasaki Heavy

Data analyzed and estimated by SIDR as of April 20, 2026. Estimated % of Clean Tech Revenues is based on AI‑generated estimates of perovskite solar cell revenues. Users should exercise caution when relying on these figures. Download data.

Conclusion

The ARL assessment of Japanese companies indicates that hydrogen commercialization advances most rapidly where incumbents can leverage pre‑existing infrastructure, customer relationships, and industrial capabilities. Firms such as Toyota and Iwatani exhibit stronger commercial adaptability precisely because hydrogen is already embedded within their operational ecosystems, while Mitsubishi Heavy Industries exemplifies how turbine flexibility can serve as a credible bridge between LNG and hydrogen‑based power generation. More capital‑intensive domains—such as liquid hydrogen shipping and international transport, led by Kawasaki Heavy Industries—remain strategically indispensable but are still in earlier commercial stages. Ultimately, Japan’s hydrogen transition is being shaped not by a singular technological breakthrough, but by the progressive integration of hydrogen into industrial systems where economic competitiveness, infrastructure readiness, and policy alignment can converge at scale.FN2

Japanese translations

ARL(導入準備度)フレームワークに基づく水素技術の評価

Introduction

世界の水素市場は、依然として化石燃料や電力システムに比べれば規模が小さいものの、過去10年間で生産、貯蔵、輸送、最終用途にわたる技術進展が顕著に加速してきた。FN1 商業化が最も速く進んでいるのは、すでに水素が中核的な操業に組み込まれている産業分野──精製、アンモニア、化学、製鉄、大規模製造──である。これらのバリューチェーンは既存インフラ、確立された需要、明確な性能要件を備えているためである。FN2 このような環境では、水素技術の商業適応力は大幅に高く、企業は新規市場の創出を迫られるのではなく、成熟した産業エコシステムの中でコスト、運用効率、供給信頼性を軸に競争することができる。FN3 これは、インフラ整備、顧客受容性、長期的経済性が依然として不確実なモビリティや発電用途とは対照的である。FN1

米国エネルギー省(DOE)の Adoption Readiness Level(ARL)フレームワークを用いて、水素バリューチェーン全体──産業用水素生産、モビリティ、インフラ、貯蔵・輸送、水素発電──で高い商業適応力を示す23社を評価した。FN1

拡張されたエビデンスベースのスコアカードによれば、産業ガス大手の Linde、Air Liquide、Air Products が最も高い ARL スコア(8.2–8.2)を維持している。これは、成熟したインフラ、強固な機能性能、競争力のある水素供給コスト、そして深く統合された下流ネットワークに支えられているためである。FN2 彼らのリーダーシップは、水素が精製、化学、製鉄、大規模製造に不可欠な産業ガスシステムの中で事業を展開するという構造的優位性を反映している。FN2 Iwatani、川崎重工業、Chart Industries なども、液化水素物流、極低温貯蔵、ターミナルインフラにおける高度な準備度を示しており、商業化が生産技術だけでなくサプライチェーンの実行力に大きく依存することを示している。FN3

水素モビリティ分野では、トヨタ、現代自動車、Doosan Fuel Cell が、FCEV、重量級トラック、バス、定置型燃料電池システムを通じて比較的強いスケールアップ可能性を示している。これらの進展はエンジニアリング能力と政策整合性に支えられているが、ARL のエビデンスは、供給される水素コストが依然として最大の商業的制約であることを示している。FN2 バッテリーEVや内燃機関車両と比較すると、水素モビリティは燃料経済性、充填ステーション密度、顧客採用のタイミングにおいて課題が残る。FN3

発電および重工業分野では、三菱重工業と川崎重工業が、根本的に異なる2つの移行モデルを体現している。 三菱重工業(ARL 6.2)は水素対応ガスタービンの開発により、LNG と水素のデュアルフューエル燃焼を通じて、電力会社に即時の座礁資産リスクを回避しつつ脱炭素化を進める実践的な道筋を提供している。FN2 この技術的柔軟性は、既存の LNG インフラを部分的に維持しながら、既存の運用フレームワークに段階的に水素を統合できるため、短期的な銀行性を高める。

川崎重工業(ARL 5.1)は、液化水素輸送、極低温貯蔵システム、ターミナルインフラを中心とする、補完的だが構造的に異なるモデルを推進している。商業化は依然として実証段階にあるものの、国際水素取引の実現可能性は輸送経済性、海上物流、輸入ターミナルの整備状況に大きく依存するため、その長期的戦略的重要性は大きい。FN3 JGC ホールディングスは水素プロジェクトの EPC 統合を通じて展開を支援し、神戸製鋼所は製鉄の脱炭素化を支える水素直接還元鉄(H₂‑DRI)技術を進展させている。これらの事例は、日本における水素商業化が、既存の産業システムを水素で強化する場合に最も効果的であり、全面的な代替を試みる場合ではないことを示している。FN1

Conclusion

ARL に基づく日本企業の評価は、既存インフラ、顧客関係、産業能力を活用できる領域で水素商業化が最も速く進むことを示している。トヨタや岩谷産業のような企業が高い商業適応力を示すのは、水素がすでにその事業エコシステムに組み込まれているためである。三菱重工業は、ガスタービンの柔軟性が LNG と水素発電の橋渡しとして信頼性の高い移行手段となり得ることを示している。 一方、川崎重工業が主導する液化水素輸送や国際物流のような資本集約型領域は、戦略的には不可欠であるものの、商業化の段階としては依然として初期にある。 最終的に、日本の水素移行は単一の技術的ブレークスルーによってではなく、経済競争力、インフラ整備状況、政策整合性が揃う産業システムの中に水素を段階的に統合していくプロセスによって形作られている。FN2

References

References

FN1 U.S. Department of Energy (DOE), Adoption Readiness Level (ARL) Framework for Technology Commercialization and Industrial Deployment.

FN2 Company disclosures, annual reports, investor presentations, and hydrogen project deployment data from Linde, Air Liquide, Air Products, Toyota, Hyundai, Mitsubishi Heavy Industries, Siemens Energy, and related industrial operators.

FN3 S1:DR Sustainability Insights analysis based on ARL evidence-based company scorecard for hydrogen technologies, 2026.