Beyond Technology Readiness: Why Market Adoption Matters

Japan’s hydrogen strategy is premised on a straightforward ambition: replace fossil energy with clean hydrogen at a national scale by 2050.[FN1] What is far less straightforward is how competing hydrogen storage and transport technologies will navigate the gap between laboratory demonstration and mass-market adoption. Technical readiness is necessary but not sufficient — the history of energy innovation is littered with technologies that were technically sound yet commercially stranded.

The U.S. Department of Energy’s Adoption Readiness Level (ARL) framework was developed precisely to address this gap. First introduced in 2020 by DOE’s Office of Technology Transitions (now the Office of Technology Commercialization), the ARL framework complements the widely used Technology Readiness Level (TRL) scale by evaluating the non-technical barriers that can block or delay commercialization.[FN2] Where TRL asks “can the technology work?”, ARL asks “can the technology be adopted?”

“Often, commercialization fails not because of the technology’s fundamental capability, but because of non-technical adoption barriers — market structures, regulatory gaps, supply chain limitations, or community perception — that were never properly mapped.” — U.S. DOE Office of Technology Commercialization

This article applies the ARL framework to four hydrogen storage and transport technologies that are central to Japan’s decarbonization push: Tokuyama Corporation’s magnesium hydride solid-state hydrogen system, Shimizu Corporation’s Hydro Q-BiC building-integrated solid-state system, Kawasaki Heavy Industries’ liquefied hydrogen (LH₂) supply chain, and Chiyoda Corporation’s SPERA Hydrogen MCH/LOHC system. The analysis evaluates each technology across all 17 ARL dimensions, assigning indicative scores on the 1–9 ARL scale.

Understanding the Adoption Readiness Level Framework

The ARL framework was developed by the U.S. DOE Office of Technology Commercialization (OTC) in partnership with industry stakeholders. It assesses 17 adoption risk dimensions organized into four core risk buckets, translating the assessment into a 1-to-9 readiness score analogous to TRL levels.[FN3] An ARL of 1 indicates that key adoption risks remain uncharacterized; ARL 9 indicates that the technology has been successfully adopted and deployed at commercial scale.

The ARL Framework

Source: US Department of Energy, Last accessed as of May 2026.

Value Proposition

The Value Proposition bucket assesses whether a technology can deliver what the market needs at a price the market can accept. It encompasses three dimensions:

Source: US Department of Energy, Last accessed as of May 2026.

Market Acceptance

The Market Acceptance bucket captures demand-side dynamics and the competitive landscape — including the structure of the market, barriers to entry, and the alignment of incentives across the value chain.

Source: US Department of Energy, Last accessed as of May 2026.

Resource Maturity

The Resource Maturity bucket evaluates whether the physical, financial, and human inputs needed to produce the technology at scale are available. It includes six dimensions — the largest of the four buckets.

Source: US Department of Energy, Last accessed as of May 2026.

License to Operate

The License to Operate bucket identifies societal, regulatory, and political risks that can block deployment even when all technical and commercial conditions are met.

Source: US Department of Energy, Last accessed as of May 2026.

The Four Technologies Under Assessment

This analysis evaluates four technologies from two distinct carrier families: solid-state (metal hydride) and liquid-phase (LH₂ and LOHC/MCH). The pairing allows a structured comparison of near-building-scale and long-distance supply-chain-scale approaches.

Technology Profiles

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

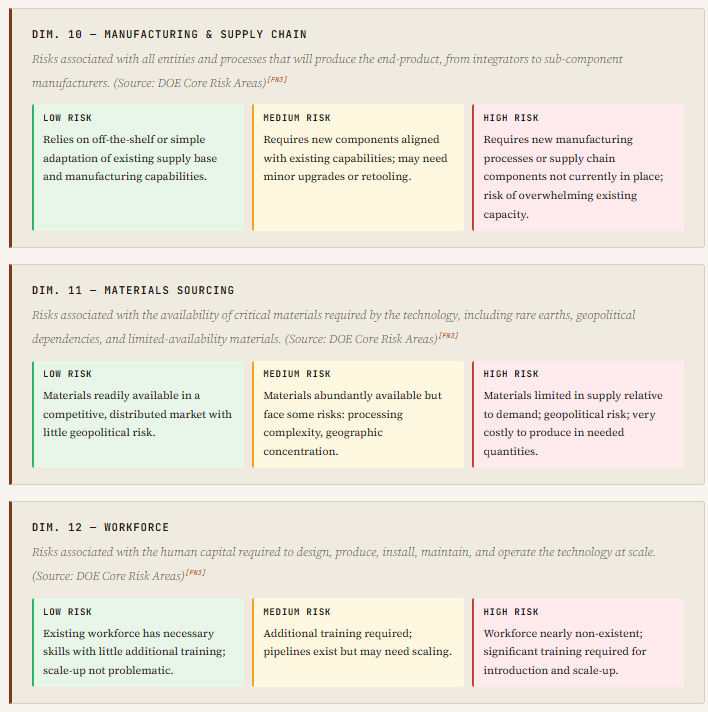

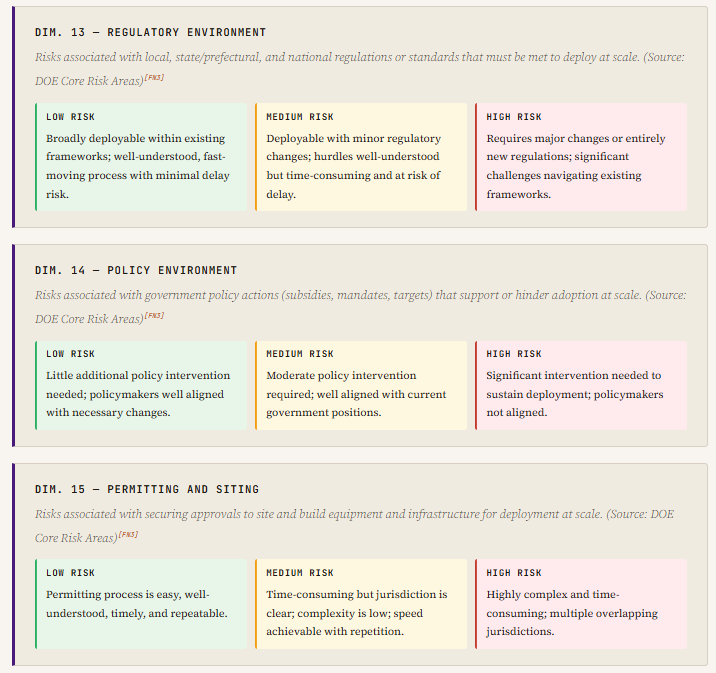

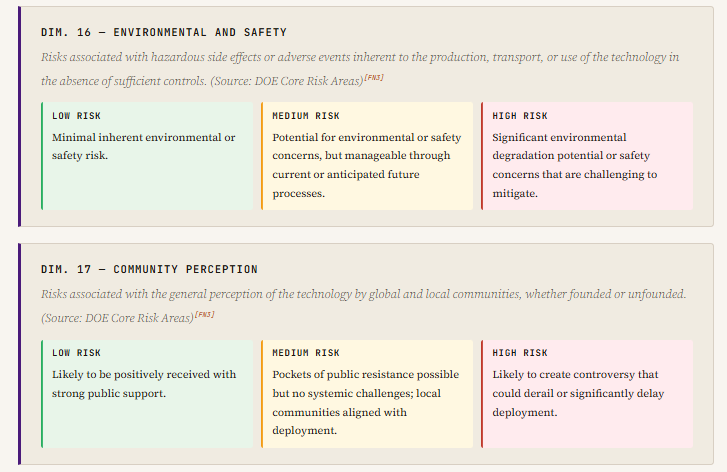

Detailed ARL Evaluation: All 17 Dimensions

The following assessments apply the DOE ARL framework criteria directly to each technology. Scores are indicative estimates based on publicly available information as of May 2026, intended to illustrate relative strengths and weaknesses rather than serve as definitive quantitative ratings.

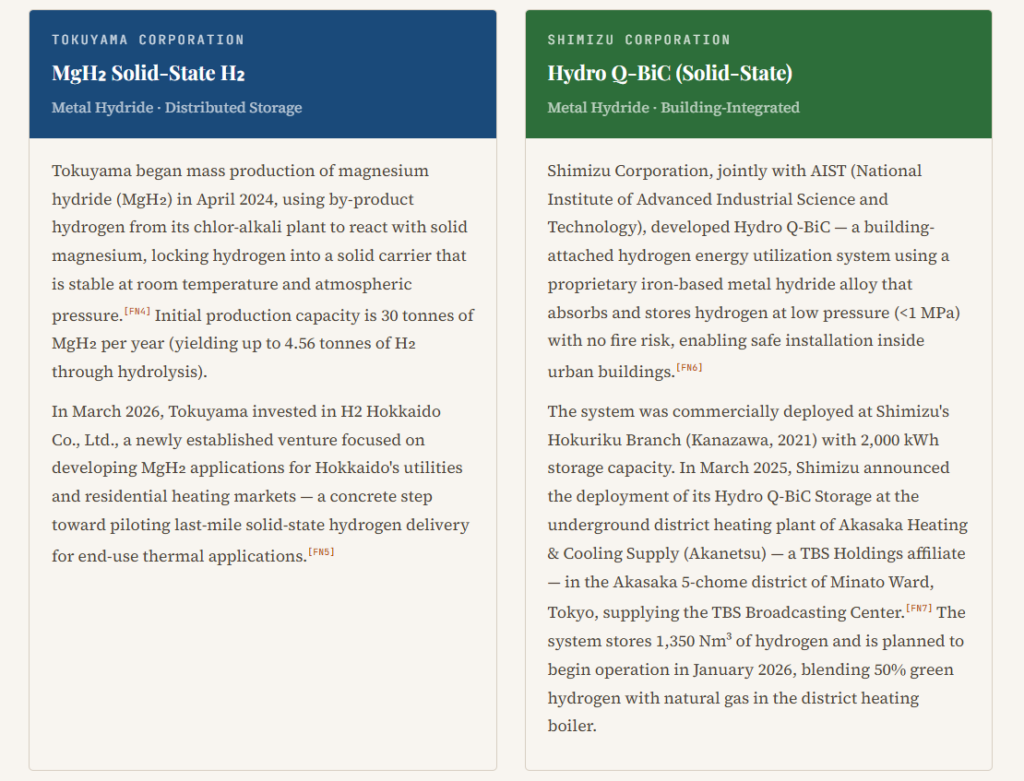

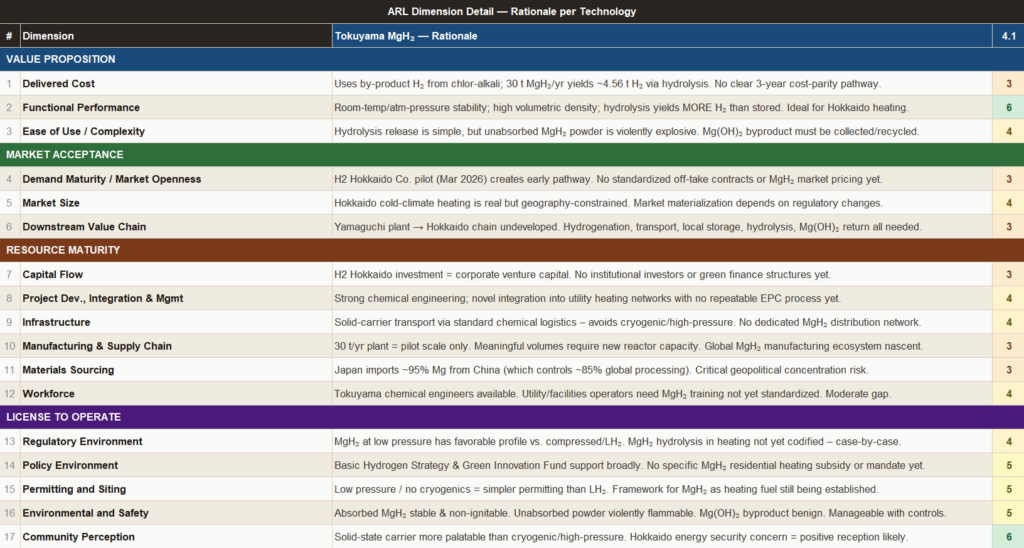

Tokuyama MgH2

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

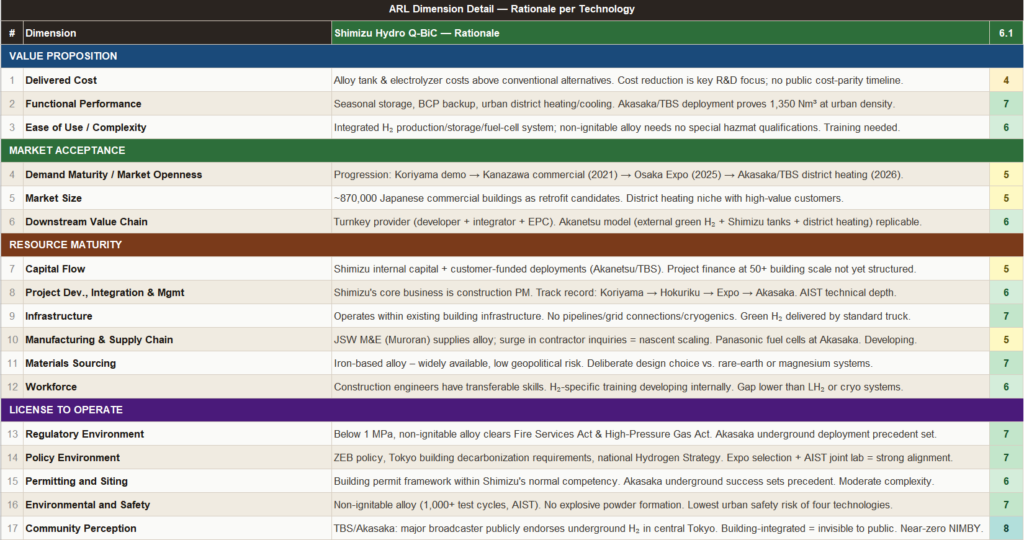

Shimizu Hydro Q-BIC

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

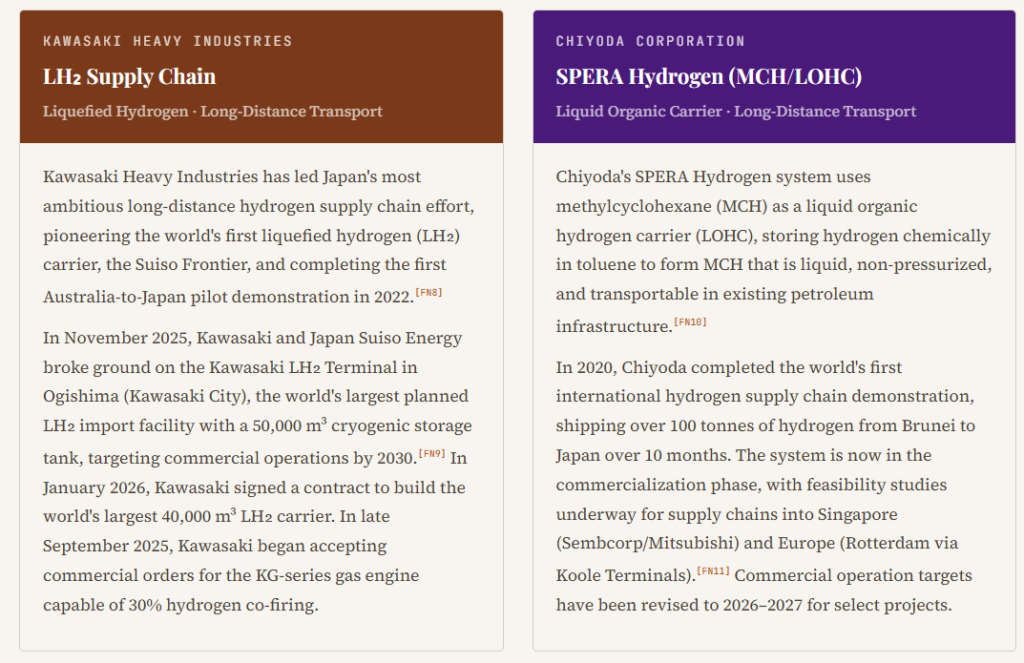

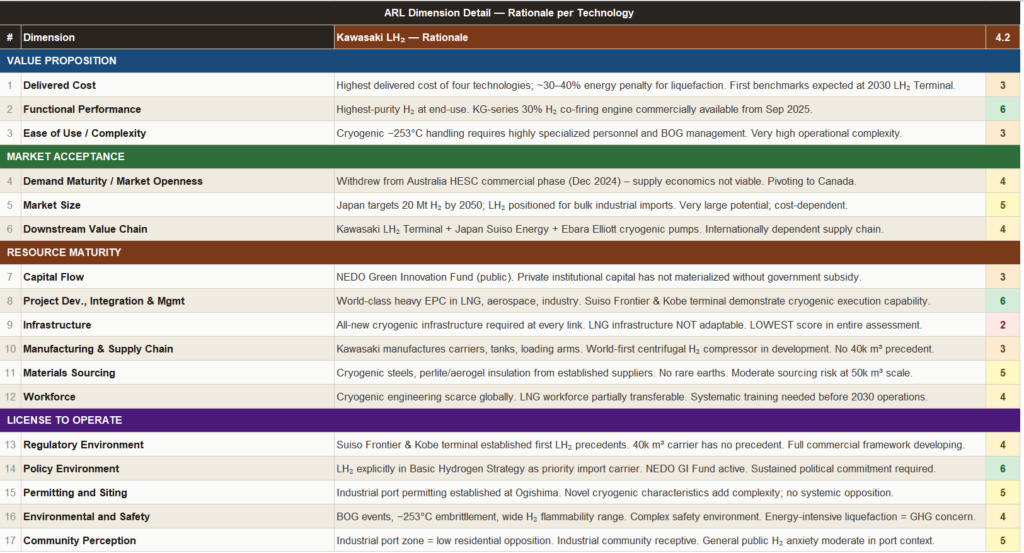

Kawasaki LH2

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

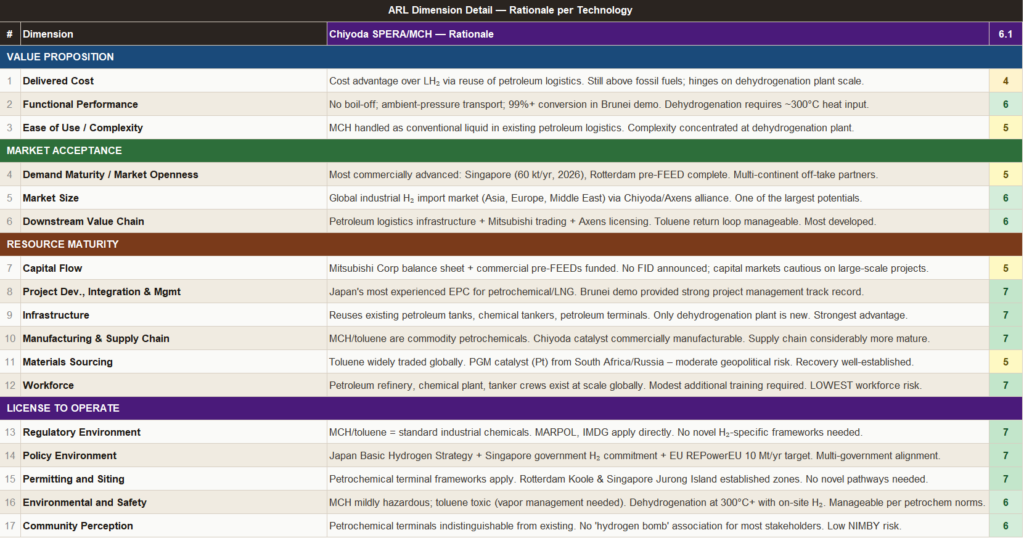

Chiyoda SPERA

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

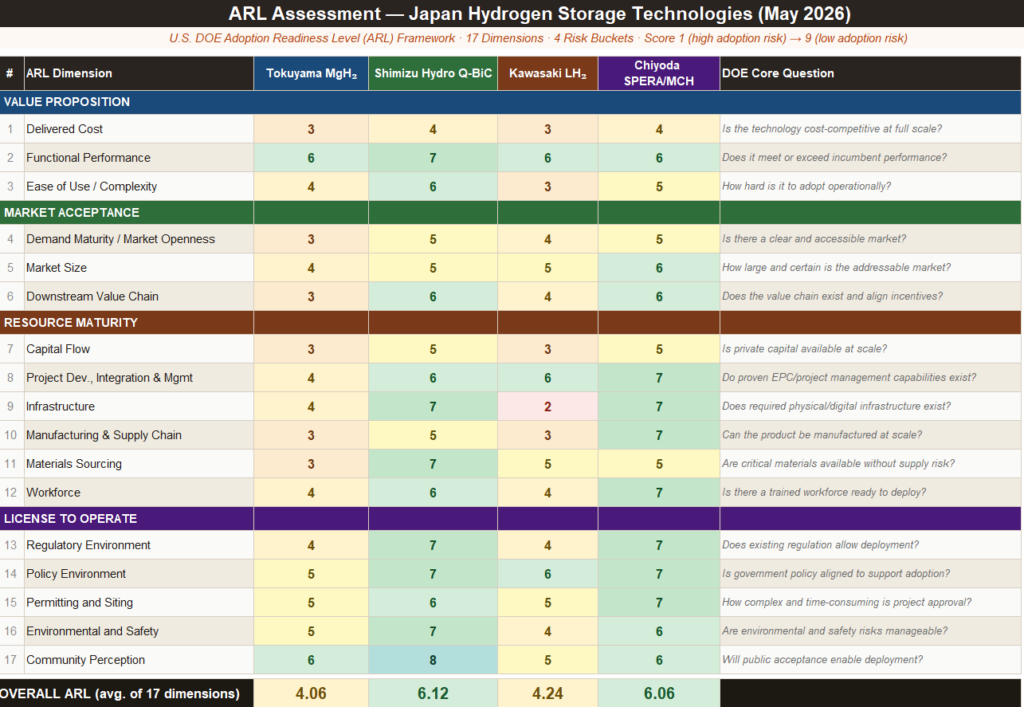

Side-by-Side ARL Score Summary

The table below summarizes the indicative ARL score (1–9 scale) for each of the four technologies across all 17 dimensions. Higher scores indicate lower adoption risk. Scores below 4 indicate critical barriers requiring active intervention.

ARL Assessment

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

Conclusions

Applying the ARL framework across all 17 dimensions reveals that Japan’s hydrogen future is not a winner-takes-all contest: each technology occupies a distinct commercialization position defined by its use case, scale, and regulatory context rather than its engineering merit alone. Shimizu’s Hydro Q-BiC leads the field at ARL 6.12 — its non-ignitable, low-pressure iron-based alloy has cleared Japan’s building codes, entered a live commercial contract with Akasaka Heating & Cooling Supply at the TBS Broadcasting Center, and built a replicable model for urban district energy integration that no competing technology has yet matched.[FN7] Chiyoda’s SPERA/MCH system is close behind at ARL 6.06, leveraging a century of petroleum logistics infrastructure to achieve the strongest Resource Maturity and License to Operate scores of the four — but remains stalled short of a Final Investment Decision because feedstock cost uncertainty has not yet yielded the long-term revenue certainty that commercial capital requires.[FN10] Kawasaki’s LH₂ supply chain, despite record-breaking engineering achievements, scores ARL 4.24, held back by the single lowest dimension score in this entire analysis — Infrastructure (ARL 2) — reflecting the irreducible reality that every link in the cryogenic chain must be built from scratch, a constraint that the December 2024 withdrawal from the Australia HESC commercial phase confirmed is not merely technical but economic.[FN14] Tokuyama’s MgH₂ approach, scientifically the most innovative of the four, sits at ARL 4.06: the H2 Hokkaido Co., Ltd. investment (March 2026) points in the right direction, but six of 17 dimensions remain in high-risk territory simultaneously — most critically, a geopolitical dependence on China for approximately 85% of global magnesium processing capacity that cannot be resolved without deliberate supply chain diversification as a precondition for any serious scale-up.[FN5]

Across all four technologies, Delivered Cost (ARL 3–4) is the universal bottleneck: no hydrogen carrier is cost‑competitive with fossil fuels at the commodity level in 2026. This makes clear that the most productive near‑term policy approach is not an undifferentiated sector‑wide subsidy, but a set of ARL‑targeted instruments calibrated to each technology’s specific commercialization barrier — cost‑reduction grants for Shimizu’s alloy manufacturing, CfD‑style revenue guarantees to unlock Chiyoda’s FID, sustained NEDO capital for Kawasaki’s 2030 terminal, and magnesium supply‑chain diversification mandates for Tokuyama.

日本語翻訳

技術成熟度を超えて:なぜ市場展開が重要なのか

日本の水素戦略は明快な目標に基づいている。すなわち、2050年までに化石エネルギーをクリーン水素へと大規模に置き換えるというものだ。[FN1] しかし、実際には、水素の貯蔵・輸送技術が「研究室での実証」から「大規模な市場展開」へと移行するプロセスははるかに複雑である。技術的な成熟は必要条件ではあるが十分条件ではない。エネルギー技術の歴史には、技術的には優れていたにもかかわらず市場に広がらなかった例が数多く存在する。

米国エネルギー省(DOE)が開発した Adoption Readiness Level(ARL)フレームワークは、まさにこのギャップを埋めるために設計された。2020年にDOEのOffice of Technology Transitions(現 Office of Technology Commercialization)が初めて導入したARLは、広く使われているTRL(技術成熟度)を補完し、商業化を阻む非技術的な障壁を体系的に評価する。[FN2] TRLが「技術は動くか?」を問うのに対し、ARLは「技術は市場に展開できるか?」を問う。

「商業化が失敗する理由の多くは、技術そのものではなく、市場構造、規制の空白、サプライチェーンの制約、コミュニティの認知といった“非技術的な展開障壁”が適切に把握されていなかったことにある。」 — 米国DOE Office of Technology Commercialization

本稿では、このARLフレームワークを、日本の脱炭素化において中核的役割を担う4つの水素貯蔵・輸送技術に適用する。対象は、トクヤマのマグネシウム水素化物(MgH₂)固体水素システム、清水建設の建物統合型 Hydro Q-BiC、川崎重工の液化水素(LH₂)サプライチェーン、千代田化工建設のSPERA Hydrogen(MCH/LOHC)である。本分析では、ARLの17次元すべてに基づき、各技術の相対的な強みと弱みを示す指標的スコアを付与する。

ARLフレームワークの理解

ARLはDOEのOffice of Technology Commercializationが産業界と協力して開発したもので、17の展開リスク次元を4つのリスク領域に整理し、TRLと同様に1〜9のスコアで表す。[FN3] ARL 1は展開リスクが未解明である状態、ARL 9は商業規模での展開が実現した状態を示す。

※上記図表参照

評価対象の4技術

本分析は、固体キャリア(メタルハイドライド)と液相キャリア(LH₂、LOHC/MCH)の2系統から4技術を選び、建物スケールと長距離サプライチェーンスケールの比較を可能にしている。

※上記図表参照

17次元の詳細ARL評価

以下の評価は、2026年5月時点の公開情報に基づく指標的スコアであり、絶対値ではなく相対的な成熟度を示す。

※上記図表参照

ARLスコアの総括

ARLの全17次元を横断的に適用すると、日本の水素キャリア技術は「勝者総取り」ではなく、用途・スケール・規制環境によって明確に棲み分けられていることが分かる。 清水建設の Hydro Q-BiC は ARL 6.12 と最も高く、非可燃・低圧の鉄系合金が建築基準をクリアし、TBS赤坂の地域熱供給との商業契約を実現し、都市部での再現可能なモデルを構築した点が突出している。[FN7] 千代田のSPERA/MCHは ARL 6.06 と僅差で続き、石油物流インフラを活用することで Resource Maturity と License to Operate の両面で最も強いが、原料水素コストの不確実性によりFIDに至っていない。[FN10] 川崎重工のLH₂は ARL 4.24 と低く、特にインフラ(ARL 2)が全分析中で最も低い。これは、極低温サプライチェーンの全工程が既存インフラを転用できず、完全にゼロから構築する必要があるという構造的制約を反映している。[FN14] トクヤマのMgH₂は ARL 4.06 で、科学的には最も革新的だが、17次元中6つが高リスク領域にあり、特に世界のマグネシウム精製の約85%を中国が占めるという地政学的依存が、スケールアップの前提条件として解消されていない。[FN5]

Delivered Cost が4技術共通のボトルネック

4技術すべてにおいて Delivered Cost(ARL 3〜4)が共通の制約となっており、2026年時点ではいずれのキャリアも化石燃料と価格競争できない。 この現実は、最も効果的な短期政策が「一律のセクター補助金」ではなく、ARLが示す個別の商業化障壁に合わせた政策設計であることを明確に示している。 具体的には、清水建設には合金製造のコスト低減補助、千代田にはFIDを開くためのCfD型収益保証、川崎重工には2030年ターミナル向けの継続的なNEDO資本支援、トクヤマにはマグネシウム供給網の多角化義務付けが該当する。

Footnotes

[FN1] Japan’s Basic Hydrogen Strategy (2023 revision) sets targets of 3 Mt/year by 2030, 12 Mt/year by 2040, and 20 Mt/year by 2050, aligned with the country’s carbon neutrality target. Ministry of Economy, Trade and Industry (METI), “Basic Hydrogen Strategy,” June 2023.

[FN2] U.S. Department of Energy, Office of Technology Commercialization, “Adoption Readiness Levels (ARL) Framework.” The ARL framework was first developed in 2020 by DOE’s Office of Technology Transitions in partnership with industry stakeholders.

[FN3] U.S. Department of Energy, “Core Risk Areas — ARL Framework.” All 17 risk dimensions, their definitions, and low/medium/high risk criteria are drawn directly from this authoritative DOE source.

[FN4] Tokuyama Corporation began mass production of magnesium hydride (MgH₂) in April 2024, using by-product hydrogen from its chlor-alkali plant at an initial capacity of 30 tonnes/year. Hydrogen Insight / World-Energy.org, “Japanese firm starts mass production of metal-based hydrogen carrier,” April 2024.

[FN5] Tokuyama Corporation invested in H2 Hokkaido Co., Ltd. in March 2026 to develop new applications for magnesium hydride targeting Hokkaido utility and residential heating markets. Fuel Cells Works, “Materials Group Backs Magnesium Hydride Venture to Advance Solid-State Hydrogen Storage,” March 2026.

[FN6] Shimizu Corporation and AIST jointly developed the Hydro Q-BiC hydrogen energy utilization system, commercially deployed first at Shimizu’s Hokuriku Branch office (Kanazawa, 2021) with 2,000 kWh storage capacity using a proprietary iron-based, non-ignitable metal hydride alloy. Shimizu Corporation, “From the Institute of Technology: A CO₂-free future powered by hydrogen energy.”

[FN7] Shimizu Corporation’s Hydro Q-BiC Storage was selected for deployment at Akasaka Heating & Cooling Supply Co., Ltd. (Akanetsu, a TBS Holdings affiliate) in the Akasaka 5-chome district, Minato Ward, Tokyo. The system stores 1,350 Nm³ of hydrogen; Panasonic fuel cells were installed by October 2025; operational start January 2026. pv-magazine International, “Japanese energy supplier to use green hydrogen for district heating, power,” March 2025; Shimizu Corporation news release, March 2025.

[FN8] Kawasaki Heavy Industries completed the world’s first international liquefied hydrogen supply chain pilot from Australia to Japan (via HySTRA consortium) in February 2022 using the 1,250 m³ Suiso Frontier carrier and the Kobe Hy touch terminal. Kawasaki Hydrogen Road.

[FN9] Kawasaki Heavy Industries and Japan Suiso Energy broke ground on the Kawasaki LH₂ Terminal (Ogishima, Kawasaki City) in November 2025, targeting Japan’s first commercial-scale LH₂ import facility (50,000 m³ storage tank, operational ~2030). A 40,000 m³ LH₂ carrier was contracted in January 2026. Kawasaki press releases, November 2025 and January 2026.

[FN10] Chiyoda Corporation’s SPERA Hydrogen system (LOHC-MCH) has been in development since 2002, with pilot test (10,000 hours) in 2014 and the world’s first international H₂ supply chain demonstration completed in 2020 (Brunei to Japan, 100+ tonnes H₂). Chiyoda Corporation, “Hydrogen LOHC-MCH System.”

[FN11] Chiyoda Corporation, Mitsubishi Corporation, and Koole Terminals completed a feasibility study and advanced to Pre-FEED for a Rotterdam LOHC-MCH hydrogen import project (commercial operation targeted 2026–2027). Separately, Chiyoda, Mitsubishi Corporation, and Sembcorp Industries advanced a Singapore LOHC-MCH project targeting 60 kt/year H₂ (2026 operation). H2 Bulletin, October 2022; Revolve Hydrogen, November 2022.

[FN12] Shimizu Corporation’s Hydro Q-BiC Lite was selected as hydrogen supply chain equipment for the 2025 Osaka World Expo, supplying green hydrogen to NTT and Panasonic Group pavilion fuel cells. Newswitch (Nikkan Kogyo Shimbun), October 2024.

[FN13] Japan Steel Works M&E (JSW M&E, Muroran, Hokkaido), which supplies the metal hydride alloy for Shimizu’s Hydro Q-BiC, reported a sharp increase in inquiries from major construction firms over the past year. Nikkei Shimbun, “Shimizu: Can Buildings Become ‘Giant Batteries’?”, December 2021.

[FN14] Kawasaki Heavy Industries withdrew from the HESC (Hydrogen Energy Supply-chain) commercial phase with Australia in December 2024, citing the inability to secure cost-competitive green hydrogen feedstock at scale. The company subsequently pivoted its supply chain development focus to Canada. Enki Research / various reports, 2025–2026.