The NVIDIA Vera Rubin NVL72 rack — 72 Rubin GPUs, 36 Vera CPUs, 260 terabytes per second of internal bandwidth, and the weight of a pickup truck — is the defining unit of next-generation AI infrastructure.[FN2] Connecting thousands of such racks into AI factories that span entire buildings, and linking those buildings at continental scale, is an infrastructure challenge copper alone cannot solve. Opto-electronic convergence is the answer — and Japan sits at the center of that transition.

What Is Opto-Electronic Convergence?

Opto-electronic convergence — 光電融合 (kōden yūgō) — integrates optical and electrical signaling within computing infrastructure to transmit data at far higher bandwidth and far lower power consumption than copper-based alternatives. By replacing electrical pathways with light at progressively shorter integration distances, the technology eliminates the power constraints that once capped AI cluster scale. Hyperscalers estimate it can reduce communication-related energy consumption by 30–50%.[FN3]

The integration frontier moves in stages — from the long distances between data centers, inward through racks and boards, and ultimately to the connections between chips on a single package. Each stage represents a distinct commercial opportunity; each favors a different set of companies.

NTT’s IOWN: The Ecosystem Architecture

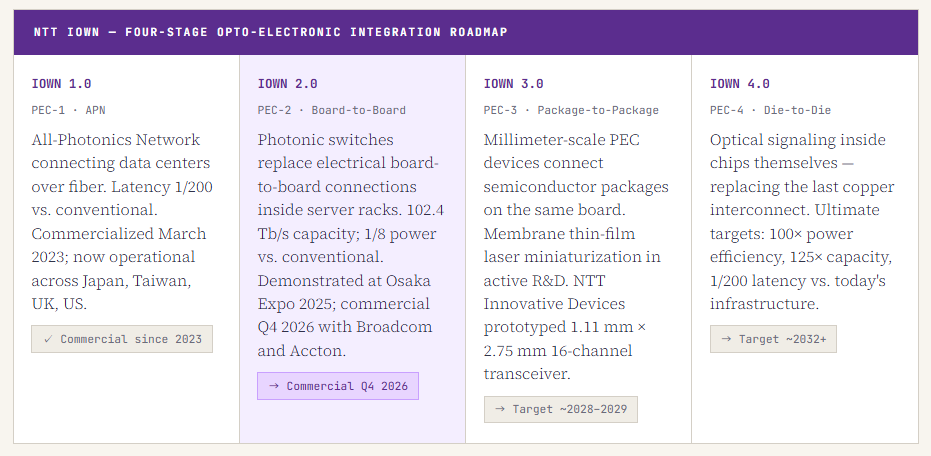

No organization has mapped this integration journey more systematically than NTT. Its Innovative Optical and Wireless Network (IOWN) initiative — backed by over 150 global member companies including Google, Microsoft, NVIDIA, Cisco, and Sony — defines four progressive stages of photonic integration through its Photonics-Electronics Convergence (PEC) device roadmap.[FN3]

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

NTT does not manufacture alone. It operates through NTT Innovative Devices Corporation (est. June 2023) for PEC device design, and relies on a supply ecosystem that maps directly onto the three wire companies in this report. Sumitomo Electric received the IOWN Global Forum’s “2025 Implementation of the Year Award” and demonstrated APN transceiver transmission over 30 km at the Forum’s Stockholm summit in April 2025.[FN3] Furukawa Electric’s laser and optical semiconductor heritage positions it as a natural PEC component supplier. Fujikura’s ultra-high-density cables underpin the APN physical layer already in commercial operation.

IOWN is not one company’s technology — it is Japan’s collective answer to what comes after copper. The three wire companies and NTT are four parts of one system, each indispensable at a different layer and a different point in time.

The Three Wire Companies: ARL Profiles

Naito Securities identifies Furukawa Electric (5801), Sumitomo Electric (5802), and Fujikura (5803) as the central wire companies in Japan’s opto-electronic convergence supply chain, each with a differentiated focus as shown in the screenshot.[FN1] Applying the DOE’s 17-dimension ARL framework reveals not only where each stands technically, but where their commercial risks and advantages lie.

Fujikura Ltd.

High-Density Cabling Leader · Revenue: Already materializing

The commercial standout. Fujikura’s Spider Web Ribbon®/Wrapping Tube Cable® (SWR®/WTC®) — cables with up to 13,824 fibers deployable in existing conduit — is the physical backbone of AI data center interconnect globally. A US DoC framework agreement (up to $20B), ¥300B capex to triple production, and FY2025 revenue growth of 22.5% to ¥979 billion confirm its role as a strategic infrastructure asset. Its world-record 600 km MCF preform points to continued technical leadership. ARL composite: 8.7.[FN3]

Sumitomo Electric Industries Ltd.

Balanced Systems Integrator · Revenue: Near-to-mid-term

Sumitomo’s advantage is breadth across the full opto-electronic stack — from semiconductor chips through cables to system integration. Its 2025 inclusion in NVIDIA’s Spectrum-X Photonics ecosystem (the only Japanese wire company named) is a concrete near-term revenue catalyst. Its GPU disaggregation via silicon-photonic optical circuit switch (with AIST, July 2025), VCBEL flip-chip CPO platform (OFC 2025), and IOWN “2025 Implementation of the Year Award” confirm it as NTT’s closest wire-company partner. ARL composite: 7.6.[FN3]

Furukawa Electric Co., Ltd.

Optical Engine Specialist · Revenue: 2027–2028 window

The most precisely scoped strategy of the three: deep expertise in laser devices and optical semiconductors — the components at the heart of every CPO device and PEC package. Through OFS and the newly unified Lightera brand (April 2025), Furukawa commands global recognition in pump lasers and specialty photonics. Its compact 12-core CPO optical connector (March 2025) — one-sixth an MPO’s footprint — bridges its laser heritage to the emerging CPO market. NEDO and NICT grant selection provide government validation of its long-term roadmap. ARL composite: 7.1.[FN3]

NTT Corp. + NTT Innovative Devices

Platform Architect · Revenue: Phased 2023–2032

NTT’s role is architecturally distinct from the wire companies: it defines the standards and integration timelines to which the entire supply chain aligns. Through IOWN and its 150-member Global Forum, NTT sets the PEC roadmap that creates demand for Furukawa’s lasers, Sumitomo’s silicon photonics, and Fujikura’s fiber. IOWN 1.0 APN is already revenue-generating; PEC-2 targets Q4 2026 commercial launch. FY2025 revenue reached ¥14.4 trillion (+5.1%); its FY2030 EBITDA target of ¥4 trillion is anchored on AI infrastructure and photonics growth. Data center capacity targeted to grow from 2,000 MW to 3,000 MW by FY2030.[FN3]

Full 17-Dimension ARL Score Table

The following table applies all 17 DOE ARL dimensions — across Value Proposition, Market Acceptance, Resource Maturity, and License to Operate — to the three wire companies in the context of opto-electronic convergence for AI infrastructure.[FN4]

ARL Assessments of Opto-Electronic Convergence

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

Notes for ARL Assessments of Opto-Electronic Convergence

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

Conclusion: Three Time Horizons, One System

The 17-dimension ARL analysis confirms what the IOWN roadmap implies structurally: opto-electronic convergence is not a single market but a sequence of markets, each unlocking over a different time horizon, each favoring a different company. Investors who evaluate all three wire companies on the same near-term revenue metric are reading an incomplete picture.

Fujikura (5803) Now → 2027

The infrastructure layer that exists today. SWR®/WTC® ultra-high-density fiber is the physical backbone of every AI data center being built at scale. Revenue is materializing at a pace the company itself cannot fully meet. The US DoC partnership and ¥300B capex commitment make Fujikura a de facto state-level infrastructure asset in both Japan and the US. Its ARL composite of 8.1 is the highest of the three precisely because the commercial journey is most advanced.

Sumitomo Electric (5802) 2025–2028

The systems integrator for the transition layer. Named in the NVIDIA Spectrum-X Photonics ecosystem and recognized by the IOWN Global Forum, Sumitomo is best positioned to capture the CPO and optical circuit switch markets as they move toward production. Its VCBEL glass substrate platform and GPU disaggregation demonstration are revenue candidates in a 2026–2028 window. Its ARL of 7.6 reflects clear technical leadership tempered by the time still required for these markets to fully open.

Furukawa Electric (5801) 2027–2030

The component specialist for the deepest integration layer. Furukawa’s laser and optical semiconductor heritage positions it uniquely for the PEC device supply chain — the components inside the optical engines that both NTT’s IOWN and NVIDIA’s CPO architecture require. Its ARL of 7.1 reflects genuine technical edge tempered by a longer commercialization runway. The 2027–2028 window, when CPO transitions from qualification to volume production, is the earnings inflection point to watch.

NTT’s role is architecturally distinct: it does not manufacture cables or laser chips, but it defines the standards and timelines to which the entire supply chain aligns. IOWN 2.0’s Q4 2026 commercial launch is a milestone for all three wire companies — it is the moment board-level opto-electronic convergence transitions from demonstration to demand generation.

The longer arc matters equally. If NTT achieves its IOWN 3.0 and 4.0 targets — package-level photonics by ~2029 and chip-level by ~2032 — the value of the optical semiconductor layer (Furukawa’s core) will appreciate significantly, while the commodity fiber layer (Fujikura’s core today) grows in volume but may face margin compression over time. Sumitomo’s full-stack position may prove the most durable of the three across the entire decade-long arc of this transition.

Taken together, Fujikura, Sumitomo Electric, Furukawa Electric, and NTT form a coherent Japanese industrial system for opto-electronic convergence — one best understood as a coordinated national strategy rather than four independent investment cases. Each company is indispensable. Each operates at a different layer of the same architecture. And the architecture, driven by the relentless demand of AI, is not going away.

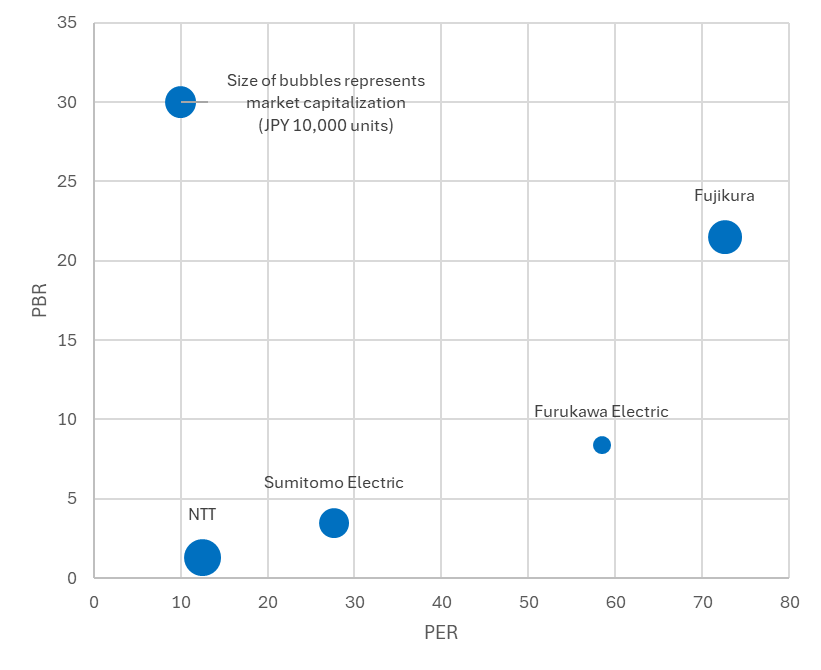

Equity Valuation of the Four Japanese Companies

Data are based on the PER and PBR reported by Nikkei as of May 8, 2026. PER (Price Earnings Ratio) indicates how many times a company’s earnings are reflected in its share price. A higher PER generally suggests that investors expect stronger future growth or are willing to pay a premium for the company’s earnings. PBR (Price Book-value Ratio) represents how many times a company’s net assets are reflected in its share price. A higher PBR typically implies that investors value the company’s assets more highly, often due to strong profitability, brand value, or expected future returns.

References

[FN1] Naito Securities, 光電融合 中核電線3社の注力分野 (Focus Areas of the Three Core Wire Companies in Opto-Electronic Convergence), research presentation, May 2026. Provided by client as screen capture.

[FN2] NVIDIA Corporation — Vera Rubin NVL72 platform specifications; NVIDIA Vera Rubin POD Technical Blog; Spectrum-X Photonics Co-Packaged Optics ecosystem announcement, GTC 2026, Jan–Apr 2026. developer.nvidia.com; nvidianews.nvidia.com.

[FN3] Company IR and press releases: Fujikura Ltd. (5803) — US DoC framework agreement Oct 2025, ¥300B capex Mar 2026; Sumitomo Electric (5802) — GPU disaggregation OCS demo with AIST Jul 2025, VCBEL CPO paper OFC 2025, IOWN GF Implementation of the Year Award Nov 2025; Furukawa Electric (5801) — Lightera launch Apr 2025, CPO 12-core connector Mar 2025, NEDO/NICT selection 2024; NTT Corporation (9432) — IOWN R&D Forum 2025 keynote Nov 2025, PEC-2 commercial schedule Feb 2026, FY2025 results May 2026; NTT DATA Group “What Makes IOWN So Impressive?” 2025; IOWN Global Forum Stockholm summit Jun 2025. All at respective corporate IR pages.

[FN4] U.S. Department of Energy, Office of Technology Commercialization — Adoption Readiness Level (ARL) Framework, 17 Dimensions across 4 Risk Buckets. energy.gov/technologycommercialization/adoption-readiness-levels-arl-framework