Photo by Lee Lawson on Unsplash

As Japan’s second-round investment package signals a new era for nuclear power in America, GE Vernova Hitachi’s small modular reactor program edges toward commercialization — amid hard lessons from the Vogtle debacle and the enduring difficulty of building nuclear in the United States.

The Japan–U.S. Strategic Investment: How the Deal Was Struck

On March 19, 2026, U.S. President Donald Trump and Japanese Prime Minister Sanae Takaichi met at the White House to announce the second tranche of projects under Japan’s landmark $550 billion investment pledge — a figure originally agreed as part of bilateral tariff negotiations that reduced levies on Japanese exports to 15 percent.FN1

The centerpiece of the energy component: a commitment by GE Vernova Hitachi — the 50/50 joint venture between U.S.-based GE Vernova and Japan’s Hitachi Group — to invest up to $40 billion in building Small Modular Reactor (SMR) power plants in Tennessee and Alabama.FN2 Two additional deals totaling up to $33 billion were simultaneously announced for natural gas generation facilities in Pennsylvania and Texas, bringing the second-round energy total to approximately $73 billion.FN3

The White House framed the SMR commitment as a “groundbreaking commercial deployment of advanced SMRs in the U.S.” that would serve as a “next-generation stable power source, stabilizing electricity prices for American people and strengthening the Japan–U.S. leadership in global technological competition.”FN4 Offtake from these projects is explicitly expected to include supplying power to artificial intelligence data centers, reflecting the enormous surge in electricity demand driven by AI infrastructure.FN5

The nuclear announcement was part of a broader package that also covered critical minerals, science, space cooperation, and defense. Initial Reuters reporting in early March 2026 had suggested Westinghouse might be involved in a nuclear component; ultimately it was the GE Vernova Hitachi joint venture — with its BWRX-300 design — that was officially named as the vehicle.FN6

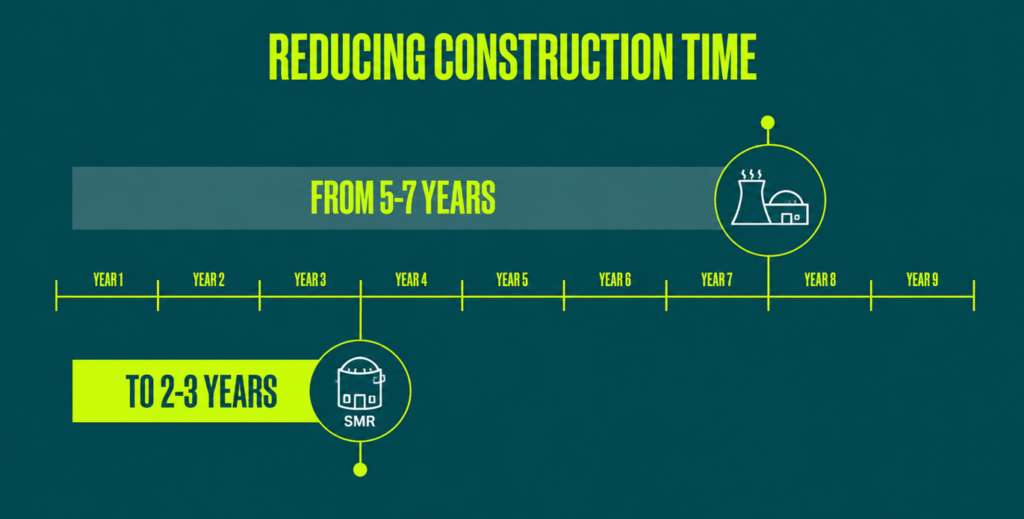

The BWRX-300 at a GlanceThe BWRX-300 is a 300 MWe boiling water small modular reactor developed by GE Vernova Hitachi Nuclear Energy (GVH). It uses natural circulation for cooling, incorporates passive safety systems, and leverages the design and licensing basis of GEH’s NRC-certified Economic Simplified Boiling Water Reactor (ESBWR). The plant footprint is reduced by approximately 90% compared to traditional large-scale reactors. Construction is targeted at 24–36 months per unit. The first commercial BWRX-300 under construction in North America is at Ontario Power Generation’s Darlington New Nuclear Project in Canada, where construction began in May 2025, with operation targeted for 2030.

Notes: See “GE Vernova Hitachi’s BWRX‑300 — Making Next‑Generation Nuclear a Reality.”

Regulatory Context:

Why No Demonstration Reactor First? The Case for Going Commercial Directly

A natural question arises: how can GE Vernova Hitachi proceed directly to large-scale commercial construction of the BWRX-300 in the United States without having built a full-scale prototype or demonstration reactor on American soil first? The answer lies in a deliberate and carefully engineered licensing strategy spanning more than a decade.

Standing on the Shoulders of a Certified Design

The BWRX-300 is not a novel reactor concept built from scratch. It is a tenth-generation evolution of GE’s boiling water reactor lineage, scaled down from the ESBWR — a 1,500 MWe design that received full design certification from the U.S. Nuclear Regulatory Commission in 2014.FN7 Because the BWRX-300 explicitly leverages the ESBWR’s established licensing basis, GE Vernova has asserted that the NRC has already reviewed and accepted approximately 80 percent of the BWRX-300’s components under pre-existing approvals.FN8

GE Vernova Hitachi began the formal NRC pre-licensing process in December 2019, submitting the first of a series of Licensing Topical Reports (LTRs) — technical documents that seek NRC approval for specific design approaches and methodologies in advance of a full construction permit application.FN9 More than two dozen LTRs have been filed and reviewed in the years since, establishing a substantial regulatory record.

The Darlington Precedent

Critically, the BWRX-300 is not awaiting its first-ever construction. In May 2025, Ontario Power Generation (OPG) broke ground on the first BWRX-300 unit at its Darlington New Nuclear Project site in Canada, making it the first commercial SMR under construction in North America.FN10 The Canadian project, which underwent a joint regulatory review by Canada’s CNSC and the U.S. NRC, provides a real-world construction template ahead of the Tennessee and Alabama deployments. The Darlington unit is scheduled to enter operation in 2030.

The Canadian build functions as a de-facto “first-of-a-kind” (FOAK) commercial prototype, giving GVH, regulators, and the supply chain a working construction campaign from which to learn before U.S. sites break ground.

TVA’s NRC Application: Tennessee’s Clinch River

In May 2025, the Tennessee Valley Authority (TVA) submitted the first U.S. application to the NRC for a construction permit to build a BWRX-300 at the Clinch River site near Oak Ridge, Tennessee.FN11 TVA had previously secured an Early Site Permit for SMRs at Clinch River — certifying site suitability on safety, environmental, and emergency planning grounds — and had been engaged in NRC pre-licensing activities since 2019. The NRC accepted the application for review, and the NRC’s review is expected to conclude within approximately 17 months from acceptance, though any technical complications could push timelines.FN12 TVA has indicated that preliminary site preparation could begin as early as 2026 even while the construction permit review is ongoing.

TVA also received a $400 million DOE grant in December 2025 to accelerate the BWRX-300 deployment, and is leading a utility coalition that has applied for an additional $800 million in DOE support.FN13

“Construction of the first BWRX-300 unit is estimated to be completed by the end of 2029, with commercial operation targeted by the end of 2030.” — GE Vernova Hitachi Nuclear Energy

The Alabama Component

The Alabama portion of the $40 billion commitment is less specifically defined in the March 2026 announcements, but TVA operates the Browns Ferry Nuclear Station in Alabama — three existing boiling water reactors whose licenses were renewed by the NRC in December 2025 for an additional 20 years, extending operation through the mid-2050s.FN14 GVH and TVA have discussed deploying multiple BWRX-300 units; TVA’s experience operating boiling water reactors makes it a natural candidate for BWRX-300 fleet expansion into Alabama following the Clinch River lead unit.

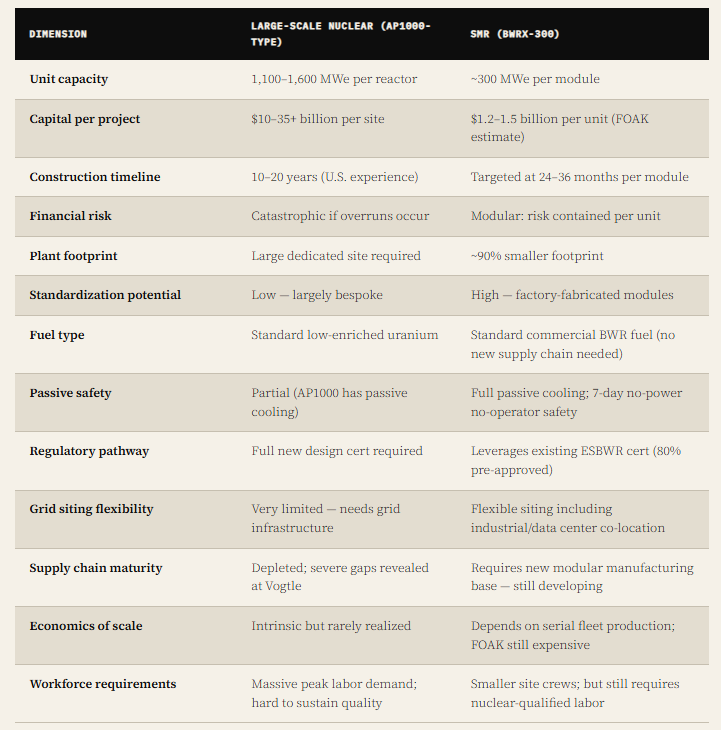

A single BWRX-300 unit is estimated to cost between $1.2 billion and $1.5 billion. At 300 MWe each, deploying sufficient capacity to approach the $40 billion investment envelope would require an order of 25–30 units — a fleet-scale ambition that, if realized, would transform the U.S. nuclear landscape and produce the economies of serial production that SMR advocates have long promised.FN15

GE Vernova’s commercial contract with TVA has been described as the first commercial SMR contract of its kind in North America, giving the BWRX-300 program a unique regulatory and commercial head start over competing SMR designs in the U.S. market.FN16

Historical Warning

The Vogtle Debacle: What Happens When Large-Scale Nuclear Goes Wrong in America

To understand why the SMR approach is so politically and commercially compelling, one need only study the cautionary saga of Plant Vogtle — the most expensive power plant ever built on Earth, and a monument to the extraordinary difficulty of constructing new large-scale nuclear in the United States.

The Promise: AP1000 Reactors for Southern Company

In 2006, Southern Nuclear — a subsidiary of Southern Company — began planning to add two new 1,100 MW AP1000 reactors (Units 3 and 4) to its Vogtle site in Waynesboro, Georgia, engaging Westinghouse Electric Company (then a Toshiba subsidiary) as the prime engineering-procurement-construction contractor. The AP1000, a pressurized water reactor, had received NRC design certification and was touted as the new generation of safe, standardized U.S. nuclear. When the project received Georgia Public Service Commission approval in 2009, the estimated total cost was $14.3 billion, with Units 3 and 4 expected to enter service by April 2016 and April 2017 respectively.FN17

Neither target was met — by years.

Lawsuit, Bankruptcy, and Toshiba’s $3.68 Billion Settlement

By 2012, deep disputes had emerged between Westinghouse and the Vogtle co-owners over $600 million in costs related to shield building design changes, $244 million in project delays, and $74 million in additional structural module design changes. Southern Company disclosed that the dispute had escalated from mediation into federal court litigation, with CEO Thomas Fanning asserting that the plant’s owners were not liable for these costs.FN18

The situation deteriorated catastrophically. On March 29, 2017, Westinghouse Electric Company filed for Chapter 11 bankruptcy protection in U.S. courts — driven in large part by the massive cost overruns at Vogtle and at a second AP1000 project at V.C. Summer in South Carolina.FN19 Under parental guarantee agreements signed in 2008 when Westinghouse received the original Vogtle order, Toshiba Corporation was on the hook for the construction shortfalls.

In June 2017, Toshiba agreed to pay Vogtle’s four owners a maximum of $3.68 billion in instalments through January 2021. By December 2017, Toshiba had accelerated and completed the full early payment of $3.225 billion — the outstanding balance on that guarantee.FN20 A parallel $2.168 billion settlement was reached with the V.C. Summer owners in South Carolina, though those two reactors were ultimately abandoned rather than completed, at a cost of roughly $9 billion with nothing to show for it.FN21

Following Westinghouse’s bankruptcy, Brookfield Business Partners acquired 100 percent of Westinghouse from Toshiba for approximately $4.6 billion in January 2018 — completing Westinghouse’s exit from Chapter 11 as a restructured firm.FN22

Vogtle Completed — At Staggering Cost

Despite the chaos, Southern Nuclear pressed forward with Vogtle Units 3 and 4 under self-managed construction, backed by more than $12 billion in DOE loan guarantees. Unit 3 entered commercial operation on July 31, 2023 — more than seven years behind its original schedule. Unit 4 followed on April 30, 2024.FN23

The final price tag approached $36 billion in combined spending across all four Vogtle co-owners, plus the $3.7 billion Westinghouse/Toshiba settlement payments, putting total economic exposure near $35–36 billion — roughly 2.5 times the original estimate.FN24 Georgia Power’s customers absorbed nearly $8 billion in overruns through the largest rate increase in state history — a 23.7 percent residential electricity rate hike — while the project’s independent monitor concluded that the cost overruns had eliminated any economic benefit to ratepayers compared to simply building natural gas plants.FN25

“The completion of the Vogtle nuclear expansion has come at an enormous cost — $36 billion, making it the most expensive power plant ever built on Earth.” — Nuclear Costs.org, 2025

The Vogtle experience viscerally illustrates the risks of large, one-off, custom-engineered nuclear construction in the United States: an entrenched regulatory environment, a depleted skilled labor base, a fragile specialized supply chain, and the near-impossibility of cost control on a first-of-a-kind megaproject in the modern era.

Technology Assessment

SMR vs. Large-Scale Nuclear: Advantages and Challenges

The SMR Advantage

The BWRX-300’s central engineering insight is simplification through subtraction. GE Vernova Hitachi claims it has eliminated roughly 90 percent of the systems required by a conventional large-scale boiling water reactor — removing entire classes of support systems while relying on gravity-driven natural circulation and passive isolation condenser cooling to maintain safe operation for seven days without power or operator action during off-normal events.FN26 Because the BWRX-300 uses the same commercially available fuel type as existing U.S. boiling water reactors, it avoids one of the most significant barriers facing competing SMR designs: unproven fuel that lacks an established supply chain.FN27

Financially, the modular approach transforms a catastrophic all-or-nothing investment into a staged, scalable deployment. Each unit costing $1.2–1.5 billion (FOAK estimate) means that a single cost overrun does not threaten the viability of an entire project. Utilities can start with one unit, validate the model, and expand the fleet incrementally — the precise opposite of the Vogtle experience.

The SMR Challenges

The promise of cheaper nuclear power from SMRs depends critically on one condition that has never yet been demonstrated at scale: serial production. The economic case for SMRs rests on the “Nth-of-a-Kind” (NOAK) cost trajectory, in which learning-by-doing and supply chain maturity drive unit costs down significantly from the expensive FOAK units. If a robust fleet order book fails to materialize — as happened with Babcock & Wilcox’s mPower SMR program, which was cancelled in 2014 — the cost benefits may never be realized.FN28

The nuclear supply chain remains severely underdeveloped. Qualifying vendors to ASME N-Stamp standards is a multi-year process, and multiple SMR designs competing simultaneously for similar components risk creating bottlenecks in equipment availability.FN29 Nuclear construction depends on a shrinking population of highly skilled welders, inspectors, and project managers, many approaching retirement — a workforce crisis that applies as much to SMR construction as to large reactors.FN30

Regulatory timelines also present risk. While the BWRX-300 benefits from the pre-existing ESBWR certification, a full construction permit review by the NRC typically takes 17–24 months or longer, and any technical questions that arise could push schedules. The NRC’s review processes were designed for large reactors and are being adapted for SMRs, creating some procedural uncertainty even for well-documented designs.FN31

Technology Profile

GE Vernova Hitachi Nuclear Energy: The BWRX-300 in Technical Detail

GE Vernova Hitachi Nuclear Energy (GVH) is a 50/50 joint venture established between GE Vernova — spun off from General Electric in April 2024 as a standalone energy technology company — and Hitachi, Ltd., one of Japan’s largest industrial conglomerates with deep expertise in nuclear engineering and reactor manufacturing.

Reactor Design

The BWRX-300 is a ~300 MWe water-cooled boiling water reactor (BWR) that uses natural circulation — no main recirculation pumps are required — and incorporates fully passive safety systems. It is a direct descendant of the GE BWR lineage stretching back more than 60 years of operational experience worldwide.FN32 The design uses a steel-plate composite containment vessel (SCCV) and a reinforced reactor building (RB), both designed for modular factory fabrication. Open-top construction methodology eliminates the need for a dedicated reactor building crane from the outset, reducing construction complexity. The plant can be sited with minimal site excavation or backfill relative to conventional reactors.

Fuel and Operating Cycle

A deliberate and strategically important design choice was the use of commercially available standard BWR fuel — the same fuel currently manufactured and supplied for operating U.S. boiling water reactors. This is in sharp contrast to several competing SMR designs (including high-assay low-enriched uranium, or HALEU-fueled designs) that require new fuel enrichment and fabrication facilities that do not yet exist at commercial scale. The BWRX-300 fuel supply chain is established and functional today. Operating cycles range from 12 to 24 months, with a 60-year design life.FN33

Safety Architecture

The BWRX-300’s safety strategy applies a Defense-in-Depth approach designed for international deployability. The isolation condenser system — inherited from the parent ESBWR design and maintained at full scale relative to the smaller reactor — enables indefinite cooling for seven days without power or operator intervention during off-normal events. This passive cooling capability draws lessons directly from the Fukushima Daiichi accident, after which both GE and Hitachi incorporated passive heat removal as a design requirement for all future reactor concepts.FN34

Regulatory Pedigree

The NRC has been engaged with the BWRX-300 since December 2019, reviewing more than two dozen licensing topical reports. The CNSC and NRC have conducted a joint regulatory review as part of the Canada-U.S. collaboration under Ontario Power Generation’s Darlington project — the results of which will inform the U.S. NRC’s review of TVA’s Clinch River application. The BWRX-300 has also completed Step 2 of the UK’s Generic Design Assessment (GDA) process, making it one of the most internationally reviewed SMR designs in existence.FN35

International Momentum

Beyond Canada and the U.S., the BWRX-300 has attracted development interest in Poland (Orlen Synthos Green Energy selected a site at Włocławek), Finland and Sweden (Fortum early works agreement, July 2025), Estonia (government-approved planning for a 600 MW nuclear plant using BWRX-300 technology), and the United Kingdom (£33.6 million government funding under the Future Nuclear Enabling Fund). Samsung C&T of South Korea has formed a strategic alliance with GVH to advance BWRX-300 deployment, adding a world-class construction contractor with major nuclear project experience.FN36

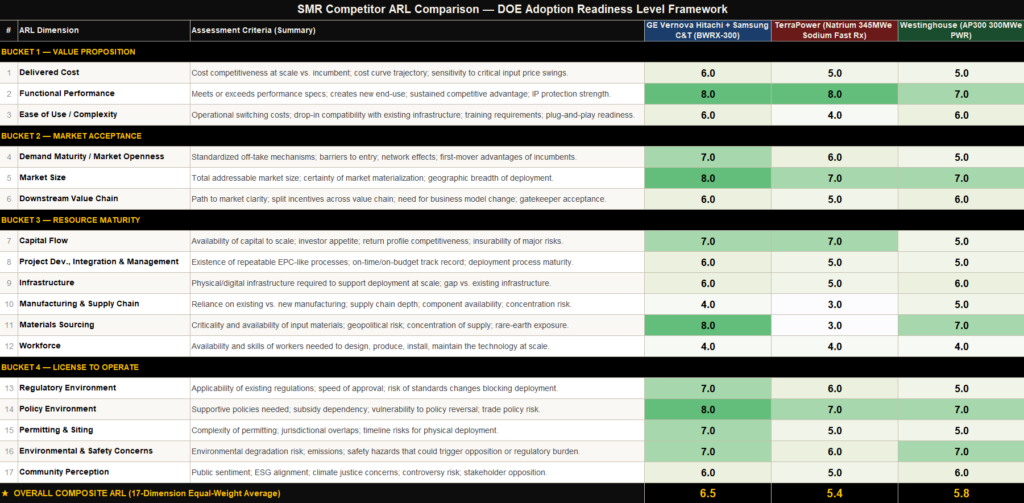

Adoption Readiness Assessment of Emerging SMR Technologies (DOE ARL Framework)

Data and analysis prepared by SIDR Research Desk and AI. This document incorporates AI-assisted analysis. While the content has been reviewed for accuracy and consistency, AI-generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification. ARL framework: U.S. Department of Energy Office of Technology Commercialization, 2024.

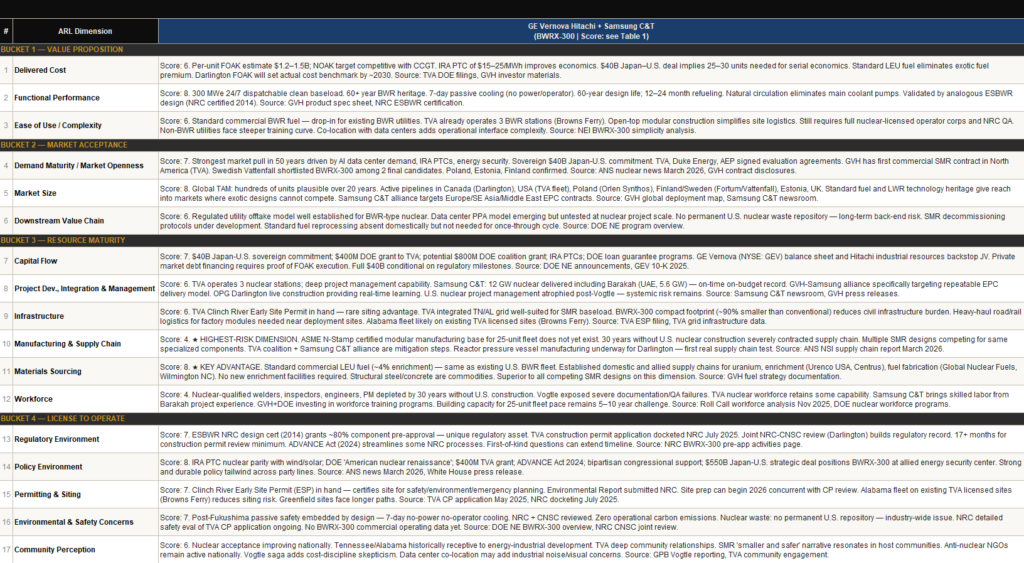

ARL Evaluation of the BWRX‑300: GE Vernova Hitachi + Samsung C&T

Data and analysis prepared by SIDR Research Desk and AI. This document incorporates AI-assisted analysis. While the content has been reviewed for accuracy and consistency, AI-generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification. ARL framework: U.S. Department of Energy Office of Technology Commercialization, 2024.

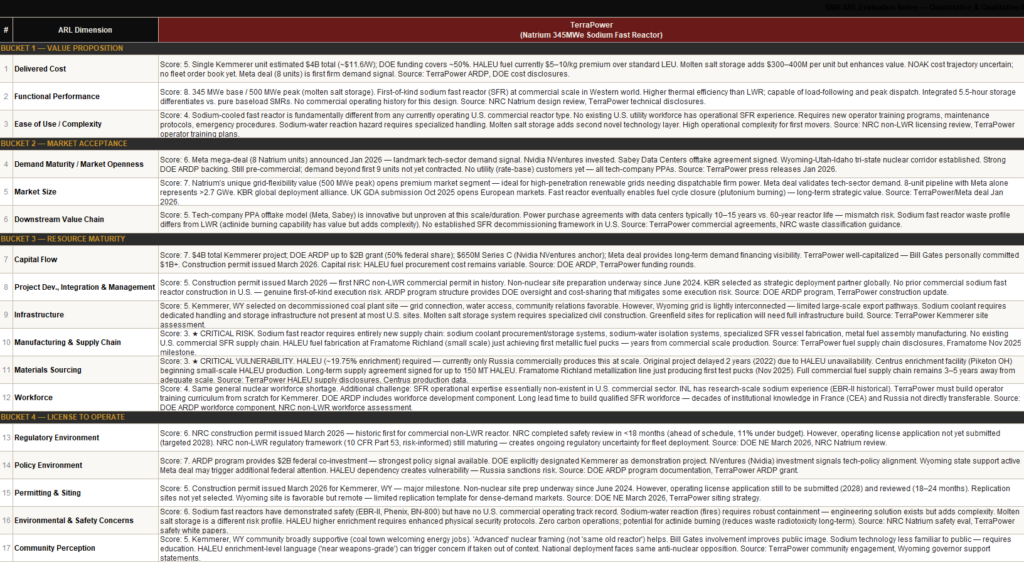

ARL Evaluation of the Natrium 345MWe Sodium Fast Reactor: Terra Power

Data and analysis prepared by SIDR Research Desk and AI. This document incorporates AI-assisted analysis. While the content has been reviewed for accuracy and consistency, AI-generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification. ARL framework: U.S. Department of Energy Office of Technology Commercialization, 2024.

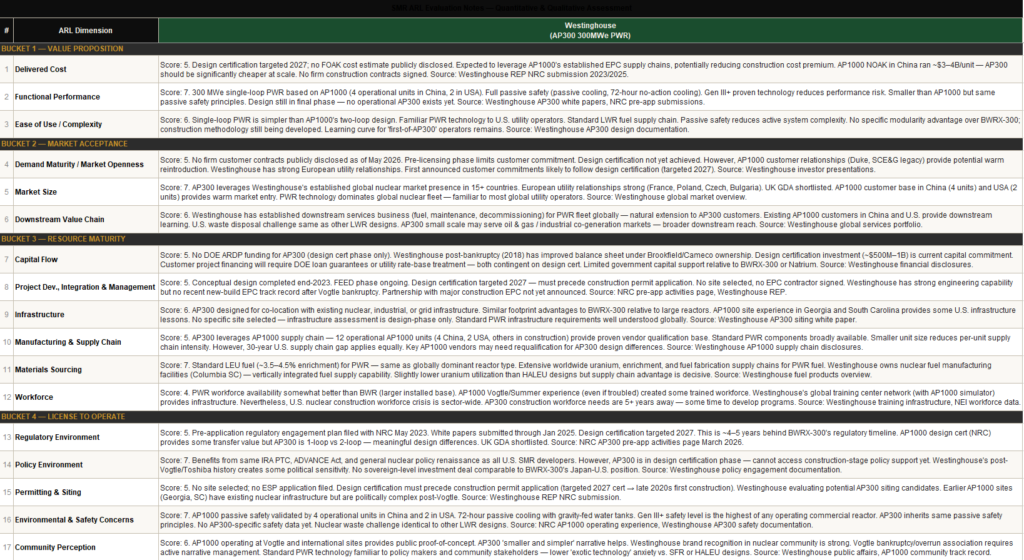

ARL Evaluation of the AP300 300MWe PWR: Westinghouse

Data and analysis prepared by SIDR Research Desk and AI. This document incorporates AI-assisted analysis. While the content has been reviewed for accuracy and consistency, AI-generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification. ARL framework: U.S. Department of Energy Office of Technology Commercialization, 2024.

Conclusion: A High-Stakes Bet on Modular Nuclear

The announcement of GE Vernova Hitachi’s $40 billion SMR commitment for Tennessee and Alabama represents one of the most significant nuclear investment pledges in U.S. history — and one of the most complex delivery challenges. The BWRX-300 program enters commercial deployment with genuine technical advantages: proven BWR heritage, 80% pre-certified components, active NRC pre-licensing since 2019, an already-under-construction lead unit in Canada, and favorable fuel supply chain conditions that competing designs cannot match.

But the ghosts of Vogtle loom large. The United States has not successfully built new nuclear on time and on budget in modern history. The supply chain is depleted. The workforce is aging. The regulatory process is long. And the modular economics that make SMRs theoretically compelling have never been demonstrated at commercial scale in North America.

What is different this time — and genuinely different — is the policy and financial architecture. The $550 billion Japan–U.S. investment framework, DOE grant programs, IRA production tax credits, and bipartisan political support create a funding environment unmatched in post-TMI (Three Mile Island) nuclear history. The Darlington construction program in Canada provides a real-world proving ground. And the urgency of AI data center power demand gives utilities an economically motivated customer base willing to pay for firm, dispatchable clean power.

The BWRX-300’s ARL profile tells a story of a technology that is technically ready, politically supported, and commercially contracted — but industrially under-resourced. The next five years will determine whether the United States can rebuild the nuclear industrial capabilities that Vogtle showed were wearing down, or whether this ambitious program joins the long list of nuclear projects that promised transformation and delivered disappointment.

For additional context, see the related story, Strategic Investment to Strengthen Power Capacity and Supply Chain Resilience through U.S.–Japan Cooperation: https://s1dr.com/2026/03/24/strategic-investment-us-japan-energy-supply-chain/

References

FN1 Nuclear Engineering International, “US, Japan in SMR deal,” March 23, 2026.

FN2 Enerdata, “The US and Japan will invest USD73bn in SMR and gas-fired power plants in the US,” March 23, 2026.

FN3 Japan Times, “Japan and U.S. announce second round of projects from Tokyo’s $550 billion pledge,” March 20, 2026.

FN4 U.S. Department of Commerce, “Joint Announcement on the Japan-U.S. Strategic Investment,” March 20, 2026.

FN5 E&E News/POLITICO, “Details emerge about US-Japan deal’s massive gas, nuclear AI projects,” March 24, 2026.

FN6 Reuters/Investing.com, “Exclusive: Japan, US aim to add nuclear power project to $550 billion investment package,” March 4, 2026.

FN7 World Nuclear News, “GE Hitachi initiates US licensing of BWRX-300,” January 31, 2020.

FN8 Energy for Growth Hub, “Which advanced nuclear models are likely to hit emerging markets first?” (Sept 2025 Update).

FN9 GE News, “GE Hitachi Nuclear Energy Begins NRC Licensing Process for BWRX-300 Small Modular Reactor,” January 30, 2020.

FN10 GE Vernova Hitachi, “BWRX-300 Small Modular Reactor” (official product page).

FN11 World Nuclear News, “TVA submits first US BWRX-300 construction application,” May 20, 2025.

FN12 AInvest, “GE Vernova’s SMR Project Gets $40B Policy Push—Execution Clarity Needed to Avoid Valuation Reset,” April 8, 2026.

FN13 U.S. Department of Energy, “NRC Dockets Construction Permit Application for TVA Small Modular Reactor,” July 11, 2025 (updated).

FN14 NucNet, “US Regulator Extends All Three Browns Ferry Nuclear Reactor Licences For 20 Years,” December 15, 2025.

FN15 Energy Central, “TVA Plans to Submit an Application for a Construction Permit to NRC for the BWRX-300 SMR.”

FN16 GE Vernova, Form ARS FY2025, SEC filing.

FN17 Power Magazine, “How the Vogtle Nuclear Expansion’s Costs Escalated,” September 24, 2018.

FN18 Lucian.uchicago.edu / Nuclear Street, “Vogtle Cost Dispute Escalates to Lawsuit,” November 2012.

FN19 Taxpayers for Common Sense, “DOE Loan Guarantee Program: Vogtle Reactors 3 & 4.”

FN20 World Nuclear News, “Vogtle owners receive full payment from Toshiba.”

FN21 Nuclear Costs, “Track Record — Nuclear Costs.”

FN22 World Nuclear News, “Westinghouse emerges from Chapter 11,” August 3, 2018.

FN23 Georgia Public Broadcasting, “A second new nuclear reactor is completed in Georgia,” April 29, 2024.

FN24 Power Magazine, “Vogtle Nuclear Expansion Price Tag Tops $30 Billion,” May 9, 2022.

FN25 Georgia Watch, “Georgia Power rates: Public to pay bulk of Plant Vogtle costs,” December 20, 2023.

FN26 U.S. Department of Energy, “First U.S. Small Modular Boiling Water Reactor Under Development,” February 19, 2020.

FN27 GE Vernova Hitachi, “BWRX-300 SMR: Proven technology for reliable power.”

FN28 American Nuclear Society (ANS), “NSI report addresses supply chain bottlenecks,” March 23, 2026.

FN29 Willis Towers Watson, “Building the future: navigating the challenges in small modular reactors,” October 2025.

FN30 Roll Call, “Worker shortage looms over new US nuclear power focus,” November 5, 2025.

FN31 Nuclear Regulatory Commission, “GVH BWRX-300 pre-application activities.”

FN32 Grokipedia, “BWRX-300.”

FN33 Nuclear Engineering International / NEI, “BWRX-300 Keeps It Simple—and Small,” May 2021.

FN34 Grokipedia, “BWRX-300” (passive safety and Fukushima context).

FN35 GE Vernova (nuclear landing page), “December 11, 2025 — GVH BWRX-300 completes Step 2 of Generic Design Assessment in UK.”

FN36 GE Vernova News, “GE Vernova Hitachi Nuclear Energy and Samsung C&T form strategic alliance to advance deployment of the BWRX-300 SMR,” October 7, 2025.

FN37 U.S. Department of Energy, “Adoption Readiness Levels (ARL) Framework.”