Photo by Tatyana Rubleva on Unsplash

Japan holds the world’s third-largest geothermal resource—nearly all untapped. As METI deploys ¥110 billion behind next-generation technologies, which industrial giants are commercially ready to deliver?

The Paradox at the Heart of Japanese Energy

Japan is one of the most volcanically active nations on earth. Over 100 active volcanoes line the archipelago, sitting atop geothermal resources that the Ministry of Economy, Trade and Industry (METI) estimates at 23 GW of conventional capacity—and potentially 77 GW if next-generation extraction technologies prove viable. Japan ranks third globally in geothermal resource potential, behind only the United States and Indonesia.FN1

Yet in fiscal year 2024, geothermal provided just 0.3% of Japan’s electricity.FN2 The country, which gave the world some of its first commercial geothermal plants in the 1960s, ranks a distant tenth in installed capacity today. The reasons are well-documented: a two-decade development freeze triggered by opposition from the onsen (hot spring resort) industry, strict national park drilling prohibitions, and regulatory fragmentation. Over 80% of Japan’s geothermal potential sits within or adjacent to nationally protected lands.

That freeze is now breaking. Prime Minister Shigeru Ishiba, who made geothermal a personal campaign platform, has pushed geothermal into Japan’s Strategic Energy Plan (SEP), published in February 2025.FN3 METI launched a public-private council in April 2025 to develop next-generation geothermal guidelines, and in May 2026 committed ¥110.2 billion (approximately USD 691 million) from the Green Innovation Fund to subsidize survey and drilling costs for three frontier technology categories: Enhanced Geothermal Systems (EGS), supercritical geothermal, and closed-loop systems.FN4

The policy shift matters because Japan also possesses a structural manufacturing advantage almost no other country can replicate: its industrial firms control roughly 70% of the global market for conventional geothermal steam turbines.FN5 Three companies—Mitsubishi Heavy Industries (MHI), Toshiba Energy Systems & Solutions, and Fuji Electric—are the backbone of that dominance. The question this report addresses is not whether Japan has geothermal potential. It is whether these manufacturers are commercially ready to convert that potential into delivered capacity—and which of them is best positioned as the technology frontier shifts.

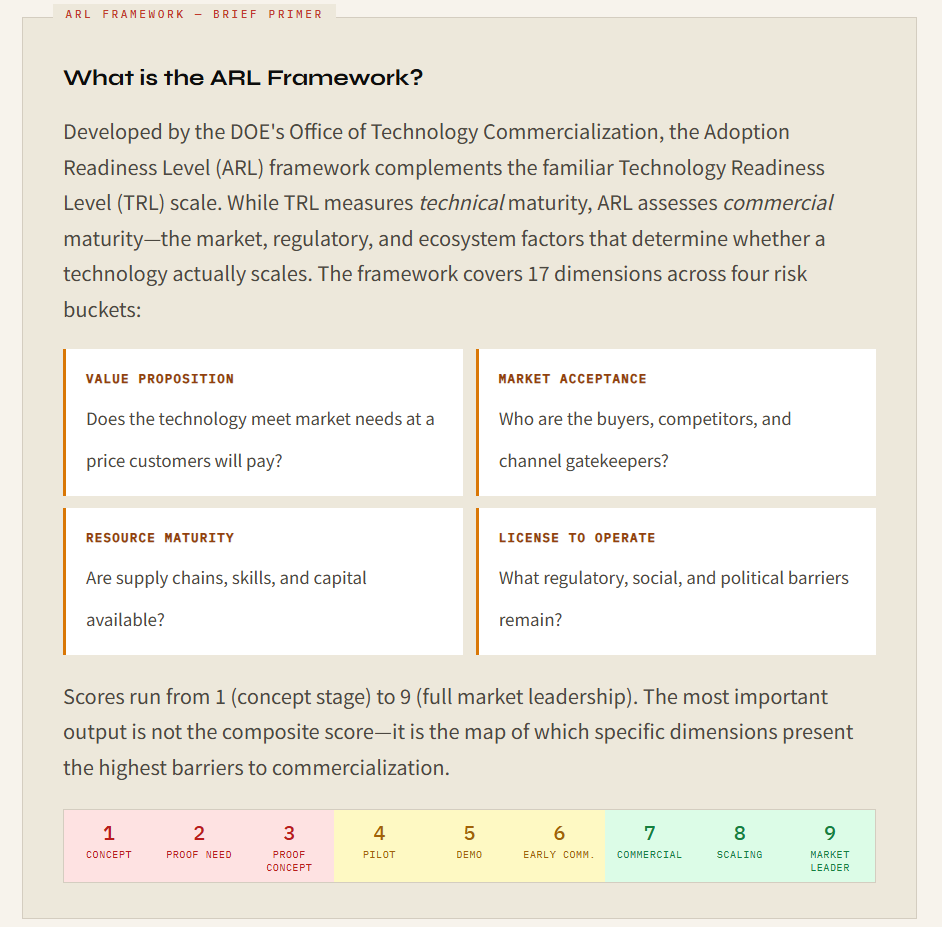

We answer that question using the U.S. Department of Energy’s Adoption Readiness Level (ARL) framework—a structured tool for evaluating the non-technical, commercial barriers that determine whether a technology reaches the market at scale.

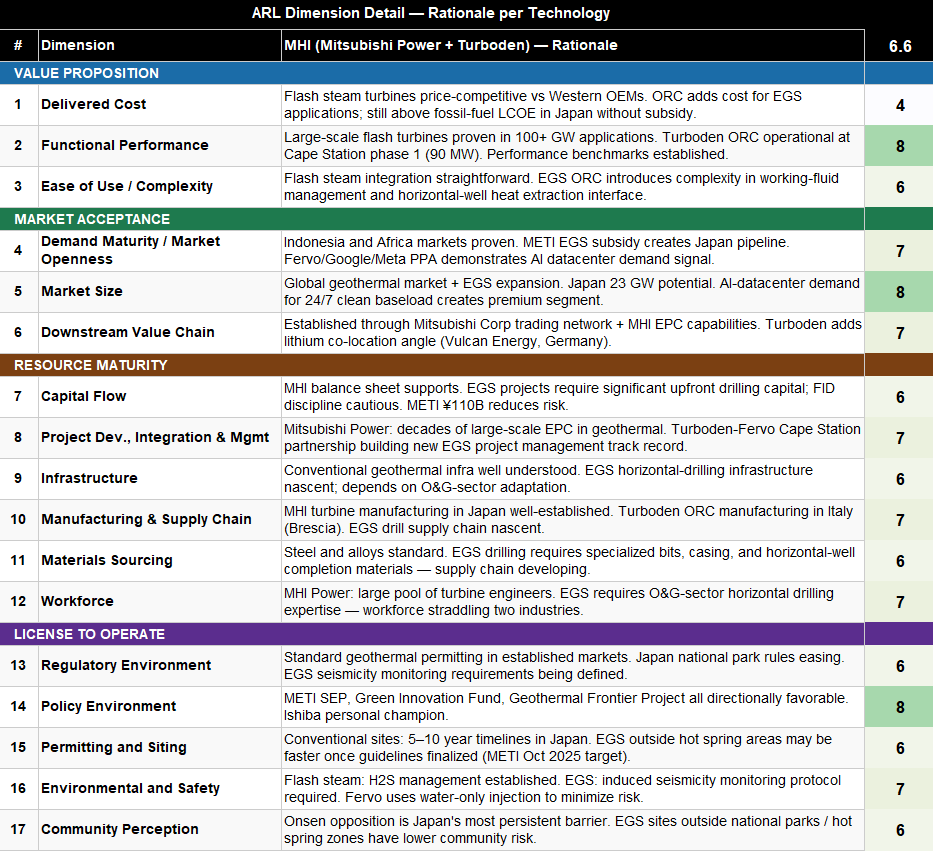

Mitsubishi Heavy Industries

MHI’s geothermal business operates across two distinct technology platforms. Mitsubishi Power, its power generation subsidiary, manufactures large-scale flash steam turbines that have been deployed across Southeast Asia, Central America, and Japan since the 1970s—the backbone of MHI’s geothermal revenue. The second platform is Turboden, an Italian ORC (Organic Rankine Cycle) turbogenerator maker acquired by MHI, which uses heat-to-electricity conversion optimized for lower-temperature or variable-enthalpy resources.

Between 2021 and 2023, MHI was a dominant but essentially conventional player: winning large-scale contracts (including the 55 MW Lumut Balai Unit 2 in Indonesia), executing plant retrofits, and deploying its TOMONI® digital analytics system on existing assets. The innovation agenda was incremental.FN6

In 2024, two decisions redefined MHI’s geothermal positioning. First, in February 2024, MHI made a strategic equity investment in Fervo Energy—the leading Enhanced Geothermal Systems (EGS) developer in the United States, headquartered in Houston.FN7 Second, in April 2024, Turboden signed a landmark collaboration with Fervo to supply power plant equipment for Cape Station, Fervo’s flagship EGS project in southwest Utah. Turboden is supplying engineering and procurement for the initial 90 MW phase, including three generators with six ORC turbines, with manufacturing already underway.FN8

Cape Station is not simply a large project—it is a commercial proof point. Fervo has secured power purchase agreements with Google and Meta, making AI data center demand the primary off-take for next-generation geothermal.FN9 Total projected capacity at Cape Station reaches 400–500 MW at full buildout. Fervo also demonstrated dramatic drilling cost reduction, cutting per-well costs from $9.4 million to $4.8 million between Project Red (2022) and Cape Station (2024).FN9

Beyond North America, Turboden’s ORC technology is enabling a geothermal-lithium integration project in Germany for Vulcan Energy Resources—generating renewable power while extracting battery-grade lithium from geothermal brine.FN10 This co-location model, where a single resource site generates both electricity and critical minerals, is emerging as a structurally important new business case that Japan’s METI is watching closely.FN11

ARL Assessments for MHI

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

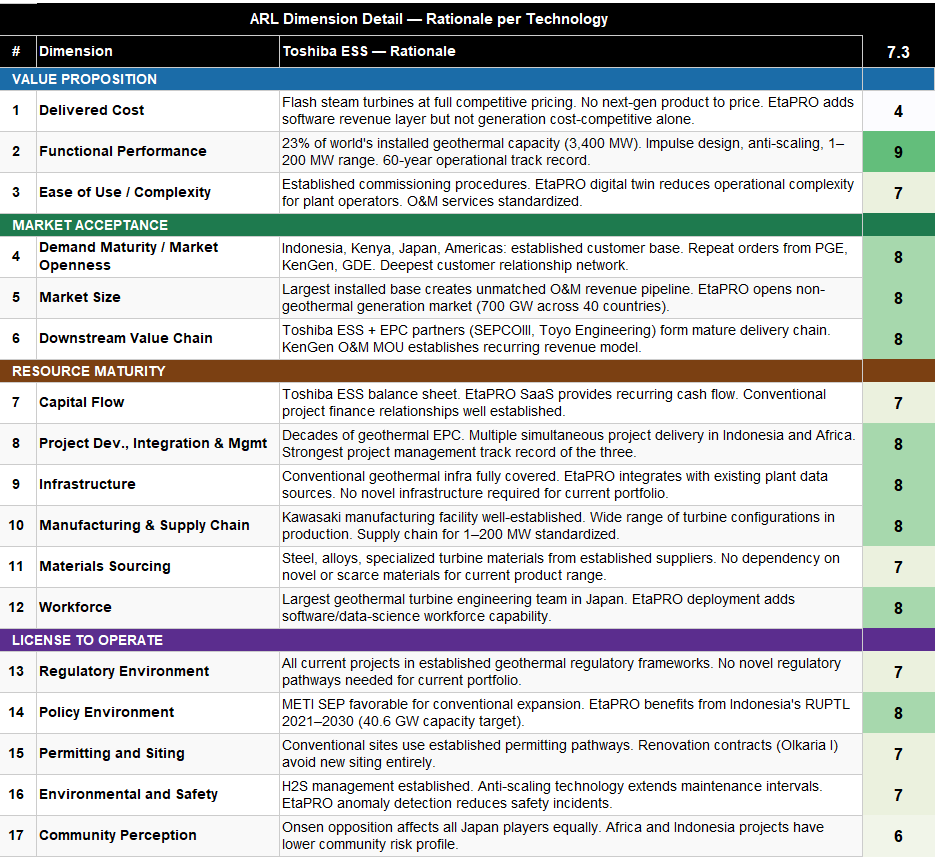

Toshiba Energy Systems & Solutions

Toshiba’s geothermal claim to leadership is grounded in six decades of operational history. The company delivered Japan’s first commercial geothermal turbine in 1966 to the Matsukawa plant in Iwate Prefecture—the country’s first full-scale geothermal power facility.FN12 As of 2024, Toshiba had supplied approximately 3,400 MW of geothermal steam turbines globally, representing roughly 23% of worldwide installed capacity—the largest share held by any single manufacturer on an installed-capacity basis.

The product range spans 1 MW to 200 MW in a single unit, covering virtually every hydrothermal resource configuration. Toshiba’s design philosophy centers on high-efficiency impulse turbine architecture, specialized rotating-part materials to resist the abrasive mineral content of geothermal steam, and proprietary anti-scaling technology to extend maintenance intervals. Single, double, triple, and four-flow configurations address different steam pressure and flow rate conditions.

Recent contract activity demonstrates sustained commercial momentum. In October 2024, Toshiba secured an order for the Wayang Windu Geothermal Power Plant Unit 3 expansion in Indonesia, targeting a 2026 commissioning.FN13 In January 2025, it won the 60.3 MW Patuha Unit 2 contract in West Java—scheduled for 2027—its second major Indonesia order in four months. Toshiba has now delivered six steam turbines in Indonesia totaling 311 MW.FN14 In March 2024, it received orders for renovation turbines at Kenya’s Olkaria I plant—the oldest geothermal plant in Africa—cementing a Memorandum of Understanding with KenGen for ongoing O&M services across East Africa.FN15

The most strategically differentiated element of Toshiba’s current portfolio is digital. In 2025, Toshiba America Energy Systems acquired the EtaPRO™ platform—a real-time digital twin system used across nearly 700 GW of generation assets in 40 countries.FN15 EtaPRO provides anomaly detection, vibration frequency analysis, and physics-based thermal performance modeling applicable to thermal, geothermal, hydro, wind, and solar plants. Its deployment to 165 Indian power plants (announced 2025) signals Toshiba’s ambition to capture software-driven recurring revenue, not merely one-time hardware contracts.

The central ARL challenge for Toshiba is the absence of any disclosed next-generation technology program. While EtaPRO is valuable regardless of generation technology, Toshiba has made no announced equity investment in EGS, no closed-loop partnership, and no supercritical R&D program. Its 2024–2026 innovation narrative is about optimizing existing conventional assets—not building the next generation.

ARL Assessments for Toshiba

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

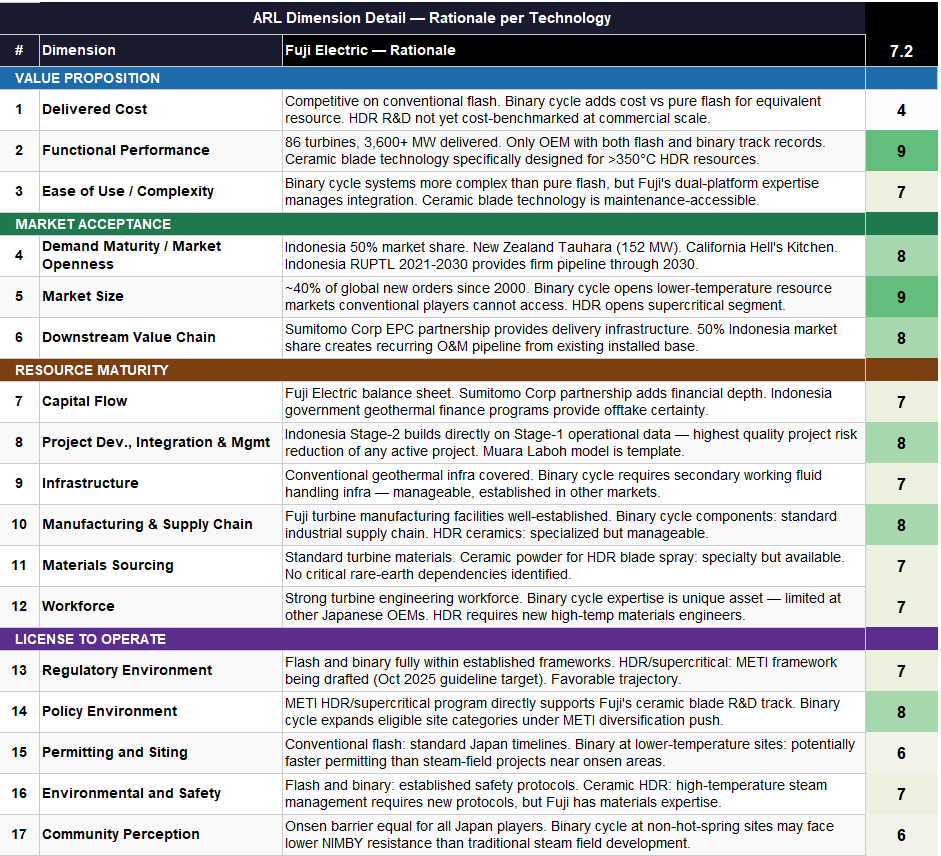

Fuji Electric Co., Ltd.

Fuji Electric is the most under-discussed of the three companies—and arguably the most strategically resilient. Since delivering Japan’s first practical geothermal power plant turbine in 1960, the company has accumulated the world’s highest new-order market share in geothermal steam turbines: approximately 40% of all global orders since 2000.FN16 As of May 2025, Fuji Electric had delivered 86 geothermal turbines with a total installed capacity exceeding 3,600 MW across five continents.

What distinguishes Fuji Electric from its Japanese peers is a critical technology breadth: it is the only company among the three with a product lineup and verified track record spanning both flash (conventional steam) and binary cycle systems. Flash systems use steam extracted directly from the reservoir to drive turbines. Binary cycle systems heat a secondary working fluid—with a lower boiling point than water—using geothermal brine, enabling power generation from lower-temperature resources that flash systems cannot economically exploit. Fuji Electric’s binary and flash integration capability is not a product catalogue entry—it reflects genuine engineering depth.

In Indonesia—the world’s second-largest geothermal producer—Fuji Electric holds an approximately 50% market share, having delivered 19 turbines. The May 2025 contract for Muara Laboh Stage-2 (adjacent to Stage-1, which has been operational since 2019) is a textbook example of compounding installed-base advantage: Stage-1 operational performance data reduces Stage-2 project risk, and the existing on-site infrastructure lowers development costs.FN17

Perhaps most significant for the next decade is Fuji Electric’s disclosed R&D program targeting Hot Dry Rock (HDR) geothermal—essentially an enhanced geothermal approach that targets rock temperatures exceeding 350°C, well above the range that conventional turbine materials and steam chemistry can tolerate. Fuji Electric has developed a proprietary ceramic powder-spray blade shield technology to address the corrosion and erosion that occurs at these temperatures. Conventional turbine design uses stainless steel plates brazed onto blade edges—but brazed joints fail above ~300°C, and the stainless steel itself cannot withstand the more aggressive chemistry of supercritical-range steam. The ceramic spray solution addresses both failure modes simultaneously.FN18

Fuji Electric also supplied turbines to CTR’s Hell’s Kitchen project at California’s Salton Sea—a 1,100 MW geothermal development that co-locates power generation with lithium extraction from the geothermal brine.FN19 This directly parallels the Vulcan Energy model that MHI’s Turboden is enabling in Germany, and provides Fuji Electric with commercial validation of the geothermal-lithium co-location thesis from a different geography.

ARL Assessments for Fuji Electric

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

The ARL framework reveals a dynamic that aggregate market share data obscures: Japan’s three major geothermal OEMs are not simply competing for the same contracts. They are positioned—differently and imperfectly—for different versions of the geothermal future. None of them is fully ready for all three of METI’s next-generation technology tracks. Each has significant ARL gaps alongside genuine strengths.

The non-technical barriers that ARL targets—regulatory speed, community acceptance, EGS drilling supply chains, and developer confidence in frontier project economics—remain the binding constraints on Japan’s 23 GW ambition, regardless of which manufacturer supplies the turbines. METI’s ¥110B subsidy program is explicitly designed to reduce those barriers. The question is whether it does so fast enough, and in which technology category, to determine which of these three industrial companies captures the largest share of the transition.

For Japan’s broader energy security thesis, all three scenarios point in the same direction: geothermal is no longer a marginal, constrained resource in the policy conversation. It is becoming a central pillar of the country’s push to reduce fossil fuel dependence, revitalize rural regions, and establish a new export technology category. The manufacturing base is ready. The policy framework is forming. The remaining work is commercial—exactly what the ARL framework is designed to map.

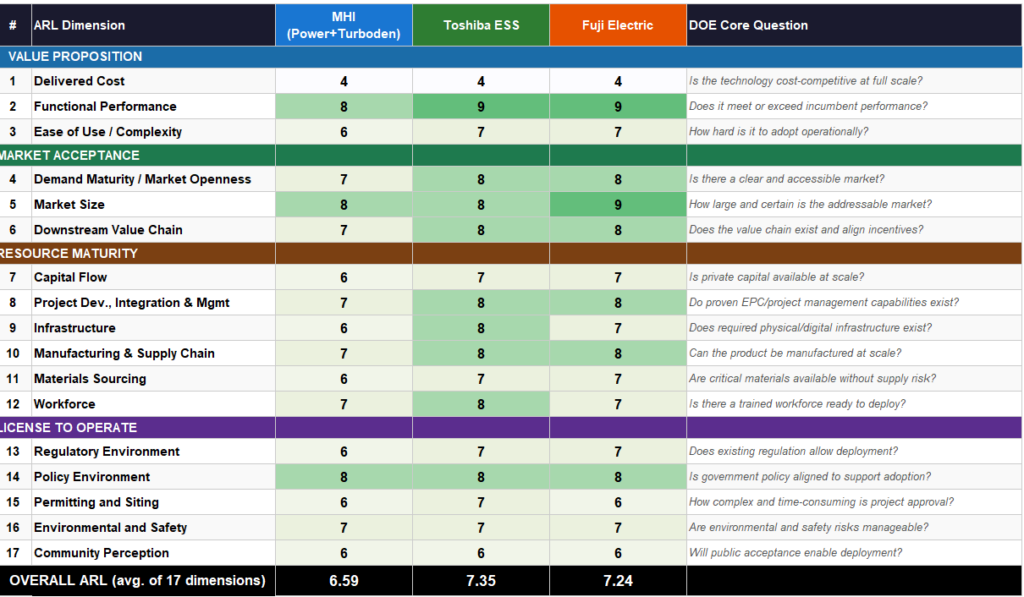

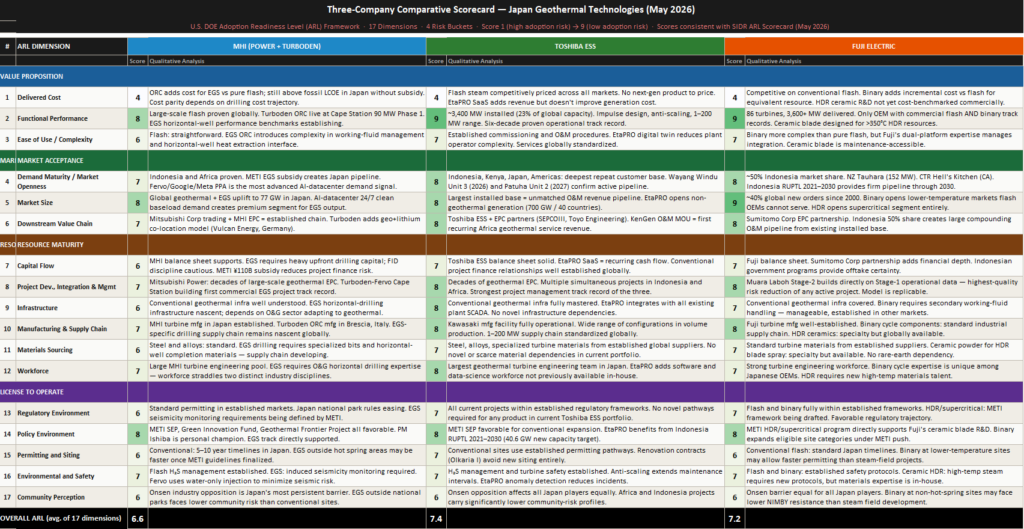

Full 17-Dimension ARL Scorecard

The table below applies the complete DOE ARL framework across all 17 dimensions for each company’s geothermal technology portfolio. Scores run from 1 (high adoption risk) to 9 (low adoption risk).

Comparative ARL Scorecard

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

Qualitative ARL Assessments

Data and analysis prepared by AI and SIDR. This document incorporates AI‑assisted analysis. While the content has been reviewed for accuracy and consistency, AI‑generated outputs may contain errors or omissions. Final interpretations and judgments should be made with appropriate expert verification.

Conclusions

The ARL framework reveals that Japan’s three major geothermal OEMs are not competing for the same market — they are positioned for different versions of the geothermal future. Toshiba leads on near-term commercial maturity (7.35) but faces structural next-generation risk.FN20 Fuji holds the most resilient technology breadth (7.24) with binary and HDR options that align directly with METI’s diversification agenda. MHI carries the highest adoption risk today (6.59) but the highest upside if EGS scales on the US trajectory — and is the only company among the three with a live commercial EGS project to point to. Across all scenarios, the binding constraints are shared: Community Perception (all score 6), Permitting & Siting (6–7), and EGS Infrastructure (MHI: 6) reflect non-technical barriers that METI’s ¥110B program is explicitly designed to remove. The manufacturing capability exists. The policy alignment is the strongest it has ever been. The remaining work is commercial — closing the gap between Japan’s 23 GW resource potential and its ~600 MW installed reality.

日本語翻訳

日本は世界第3位の地熱資源を保有している——そのほとんどが未開発のままだ。METI(経産省)が次世代技術に1,102億円を投じる中で、どの産業大手が商業化に向けて準備が整っているのか。

日本のエネルギーの中心にあるパラドックス

日本は世界でも有数の火山国である。100以上の活火山が列島に連なり、その下には経産省が従来型で23GW、次世代技術が実用化されれば最大77GWと推計する地熱資源が広がっている。地熱資源量では米国、インドネシアに次ぐ世界3位だ。FN1

しかし2024年度、日本の地熱発電比率はわずか0.3%にとどまった。FN2 1960年代に世界初期の商業地熱発電所を送り出した国でありながら、現在の導入容量は世界10位に過ぎない。理由はよく知られている。温泉業界の反対による20年に及ぶ開発凍結、国立公園内での掘削規制、そして許認可制度の分断である。日本の地熱資源の80%以上が国立公園内または隣接地に存在する。

しかし、その凍結は今まさに解けつつある。地熱を個人的な政策テーマに掲げてきた石破茂首相は、2025年2月に公表された第7次エネルギー基本計画(SEP)に地熱を正式に組み込んだ。FN3 2025年4月には次世代地熱ガイドライン策定のための官民協議会が発足し、2026年5月にはグリーンイノベーション基金から1,102億円を拠出し、以下の3つの先端技術カテゴリーにおける調査・掘削費用を補助すると発表した。FN4

- EGS(Enhanced Geothermal Systems:高温岩体地熱)

- 超臨界地熱

- クローズドループ地熱

この政策転換が重要なのは、日本が他国にはほぼ再現不可能な構造的製造優位性を持つからだ。日本企業は従来型地熱蒸気タービンの世界市場の約70%を握っている。FN5 三菱重工(MHI)、東芝エネルギーシステムズ(Toshiba ESS)、富士電機の3社がその中心だ。

本レポートが問うのは「日本に地熱資源があるか」ではない。 「この3社は、その資源を実際の発電容量へと変換できる商業準備が整っているのか。そして技術フロンティアが変化する中で、誰が最も有利なのか」である。

その問いに答えるために、本レポートは米国エネルギー省(DOE)のARL(Adoption Readiness Level)フレームワークを用いる。これは、技術が市場規模で展開されるかどうかを左右する「非技術的・商業的障壁」を体系的に評価するツールだ。

三菱重工(MHI)

MHIの地熱事業は2つの技術プラットフォームから成る。

- 大型フラッシュ蒸気タービン(Mitsubishi Power)

- 1970年代以降、東南アジア・中米・日本で多数導入

- MHIの地熱収益の中核

- ORC(Organic Rankine Cycle)ターボ発電(Turboden)

- イタリア企業を買収

- 低温・変動エンタルピー資源向け

2021〜2023年のMHIは、55MWのLumut Balai Unit 2(インドネシア)など大型案件を受注し、既存設備の改修やTOMONI®デジタル分析システムの展開など、堅実だが保守的な事業運営だった。FN6

しかし2024年、MHIの地熱戦略は大きく転換した。

① Fervo Energy(米EGSトップ企業)への戦略投資(2024年2月)FN7

② FervoのCape Station(ユタ州)へのTurboden設備供給契約(2024年4月)FN8

Cape Stationは単なる大型案件ではない。 GoogleとMetaがPPAを締結し、AIデータセンター需要が次世代地熱の主力オフテイクとなった商業実証案件である。FN9 総容量は400〜500MWに達する見込み。

Fervoは掘削コストを940万ドル → 480万ドルへ半減させ、EGS商業化の最大の障壁を突破しつつある。

北米以外でも、TurbodenはドイツのVulcan Energyの「地熱+リチウム抽出」プロジェクトを支えている。FN10 単一の地熱資源から電力と重要鉱物を同時生産するモデルは、METIが注視する新たな事業形態だ。FN11

東芝エネルギーシステムズ(Toshiba ESS)

東芝の地熱事業は60年の歴史に基づく。 1966年、岩手県松川に日本初の商業地熱タービンを納入。FN12 2024年時点で累計3,400MW(世界23%)を供給し、単一企業として世界最大の導入実績を持つ。

製品ラインナップは1〜200MWと幅広く、ほぼすべての地熱資源条件に対応。 高効率インパルスタービン、耐摩耗素材、スケーリング抑制技術などが特徴。

商業実績(2024〜2025)

- Wayang Windu Unit 3(インドネシア)受注(2024年10月)FN13

- Patuha Unit 2(60.3MW)受注(2025年1月)FN14

- ケニアOlkaria I更新タービン受注(2024年3月)FN15

デジタル戦略:EtaPRO™(2025年買収)

- 40カ国・700GWの発電資産を監視

- 165のインド発電所に導入予定 → ソフトウェア収益の拡大を狙う

ARL上の課題

- EGS・超臨界・クローズドループへの投資がゼロ

- 現状は「既存技術の最適化」に留まり、次世代技術の欠如がリスク

富士電機(Fuji Electric)

富士電機は3社の中で最も語られないが、最も戦略的に強靭な企業かもしれない。

2000年以降の世界新規受注シェア40%で世界トップ。FN16 2025年時点で86基・3,600MW以上を世界に供給。

最大の差別化:フラッシュ+バイナリー両方に強い唯一の日本企業

- フラッシュ:従来型蒸気タービン

- バイナリー:低温資源を活用できる → 資源多様化を狙うMETIの方向性と完全一致

インドネシア市場で50%シェア

- Muara Laboh Stage-2(2025年5月契約)FN17

- Stage-1の実績がStage-2のリスクを低減

HDR(350°C超)向けタービンR&D

- セラミック粉末スプレーブレード保護技術

- 従来材の限界(300°C)を突破 → 超臨界領域の腐食・摩耗問題を同時に解決FN18

地熱+リチウム抽出(米CTR)

- Salton Seaの1,100MWプロジェクトにタービン供給FN19 → MHIのVulcan案件と並ぶ商業実証

ARLフレームワークが示す本質

市場シェアでは見えないが、3社は同じ市場を争っていない。

- Toshiba:短期の商業成熟度でトップ(7.35)

- Fuji Electric:技術多様性で最も将来に強い(7.24)

- MHI:現時点のリスクは最大(6.59)だが、EGSが伸びれば最大のアップサイド

共通のボトルネックは、

- コミュニティ受容

- 許認可

- EGSインフラ

といった非技術的障壁であり、METIの1,102億円はこれを解消するためのもの。

結論

日本の地熱は、もはや政策議論の周縁ではない。 化石燃料依存の低減、地方創生、新たな輸出産業の柱として位置づけが変わりつつある。

製造基盤は整った。政策枠組みも整いつつある。 残る課題は「商業化」——まさにARLが可視化する領域である。

References

FN1 — METI / JOGMEC, Japan Geothermal Resource Potential Assessment, 2023–2024. Conventional resource: 23 GW; next‑generation uplift to ~77 GW. See also: ThinkGeoEnergy, Japan Geothermal Market Overview, 2024.

FN2 — Agency for Natural Resources and Energy (ANRE), FY2024 Energy Supply and Demand Actual Results (速報), METI, 2024. Geothermal share: 0.3% of total electricity generation.

FN3 — METI, 第7次エネルギー基本計画 (7th Strategic Energy Plan), February 2025. Geothermal target: 1–2% of power mix by FY2040.

FN4 — METI / NEDO, Green Innovation Fund — Next‑Generation Geothermal Power Generation Subsidy Program, announced May 2026. Total: ¥110.2 billion (approx. USD 691 million); covering up to two‑thirds of survey and drilling costs.

FN5 — ThinkGeoEnergy / International Geothermal Association (IGA), Global Geothermal Market and Technology Report, 2024. Japanese OEM share of global conventional geothermal turbine market: ~70%.

FN6 — Mitsubishi Power, Lumut Balai Unit 2 Geothermal Power Plant — Project Completion, Press release, 2024. 55 MW, PT Pertamina Geothermal Energy (PGE), South Sumatra, Indonesia.

FN7 — Mitsubishi Heavy Industries (MHI), Strategic Investment in Fervo Energy, Press release, February 2024.

FN8 — Turboden S.p.A. (MHI Group), Fervo Energy Cape Station — ORC Power Plant Equipment Supply Agreement, Press release, April 2024. 90 MW Phase 1; three generators; six ORC turbines.

FN9 — Fervo Energy, Cape Station Project Update — Google and Meta Power Purchase Agreements, 2024. Total projected capacity: 400–500 MW.

FN10 — Fervo Energy / Hart Energy, EGS Well Cost Reduction: Project Red to Cape Station, Technical briefing reported in Hart Energy, December 2024. Per‑well cost: USD 9.4M (2022) → USD 4.8M (2024).

FN11 — Vulcan Energy Resources & Turboden (MHI), Zero Carbon Lithium® Project — Geothermal Power and Lithium Extraction, Upper Rhine Valley, Germany, 2024.

FN12 — Toshiba Energy Systems & Solutions, Geothermal Business Overview — Global Installed Capacity and Track Record, Corporate disclosure, FY2024. First commercial turbine: Matsukawa, Iwate (1966); cumulative: ~3,400 MW / ~23% global share; Indonesia: 6 turbines, 311 MW.

FN13 — Toshiba ESS, Wayang Windu Unit 3 Turbine Order, Press release, October 2024; Patuha Unit 2 (60.3 MW) Supply Contract, Press release, January 2025.

FN14 — Toshiba ESS, Olkaria I Geothermal Plant Renovation Turbine Order and KenGen O&M MOU, Press releases, March–April 2024. Olkaria I, Kenya: oldest geothermal plant in Africa.

FN15 — Toshiba America Energy Systems, Acquisition of EtaPRO™ Performance Monitoring and Diagnostics Platform, Press release, 2025. ~700 GW covered; 40 countries; 165 Indian power plants announced.

FN16 — Fuji Electric Co., Ltd., Geothermal Power Generation Systems — Business Overview, 2024–2025. 86 turbines delivered; >3,600 MW; ~40% global new‑order share since 2000; Indonesia: 19 turbines, ~50% market share.

FN17 — Fuji Electric, Muara Laboh Geothermal Power Plant Stage 2 — Turbine Supply Contract, Press release, May 2025. Adjacent to Stage‑1 (85 MW, operational since December 2019), South Solok, West Sumatra, Indonesia.

FN18 — Fuji Electric, Hot Dry Rock (HDR) Geothermal Turbine Technology — Ceramic Powder‑Spray Blade Shield R&D, Technical paper / corporate disclosure, 2024. Target resource temperature: >350°C. Presented at Japan Geothermal Society Annual Conference.

FN19 — Controlled Thermal Resources (CTR), Hell’s Kitchen Geothermal Phase 1 — Development Update, 2024. Total project capacity: 1,100 MW; co‑location of power generation and lithium extraction from geothermal brine, Salton Sea, California. Fuji Electric turbine supply confirmed.

FN20 — SIDR (Strategic Intelligence for Deep Research), ARL Scorecard — Japan Geothermal Technologies (MHI, Toshiba ESS, Fuji Electric), Internal analytical assessment, May 2026. Scores derived by applying the U.S. DOE Adoption Readiness Level (ARL) framework to publicly available company disclosures, press releases, and regulatory filings. Not an official DOE evaluation.