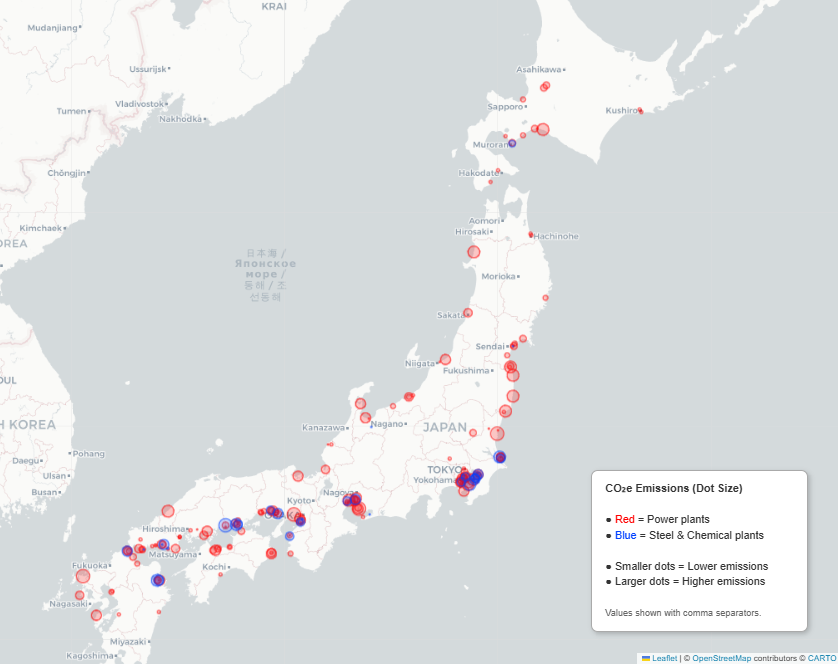

This map shows power plants, steel mills, and chemical complexes in Japan that each emit more than 100,000 tonnes of CO₂e per year, making them subject to regulation under the GX‑ETS.

As mandatory carbon trading arrives in FY2026, the map of regulated facilities reveals why steel and chemicals—already 54% of industrial CO₂e—will define the system’s credibility.

Japan’s Green Transformation Emissions Trading Scheme (GX-ETS) has crossed its most consequential threshold yet: in May 2025, the Diet enacted legislation making participation mandatory—beginning in fiscal year 2026—for all facilities emitting 100,000 tonnes or more of CO₂ annually.FN1 The rule is expected to bring between 300 and 400 companies into scope, collectively accounting for roughly 60% of Japan’s domestic greenhouse gas output.FN2 That mandate is not abstract policy language; it maps directly onto a specific industrial geography visible in the figures below—a corridor of large-stack facilities concentrated along the Pacific coast, the Osaka Bay industrial belt, and the Keihin complex encircling Tokyo and Yokohama.FN3

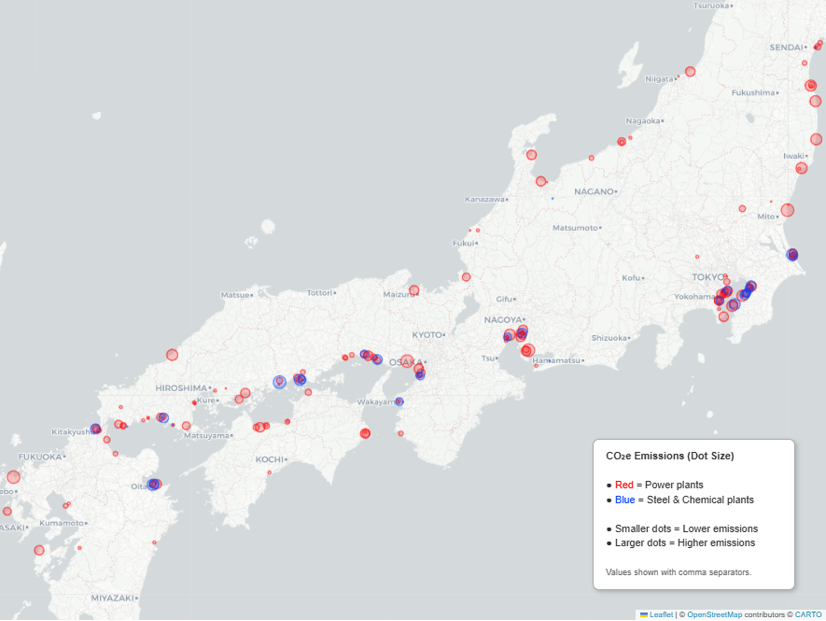

Map of Japan showing CO2e emissions by power plants and steel/chemical facilities – Honshu close-up

Dot size represents CO₂e volume (comma-separated values ≥ 10,000,000 t indicated by large markers). The dense cluster around Osaka–Hiroshima and the Keihin mega-region accounts for a disproportionate share of industrial load. Source: Author compilation; base map © OpenStreetMap / CARTO.

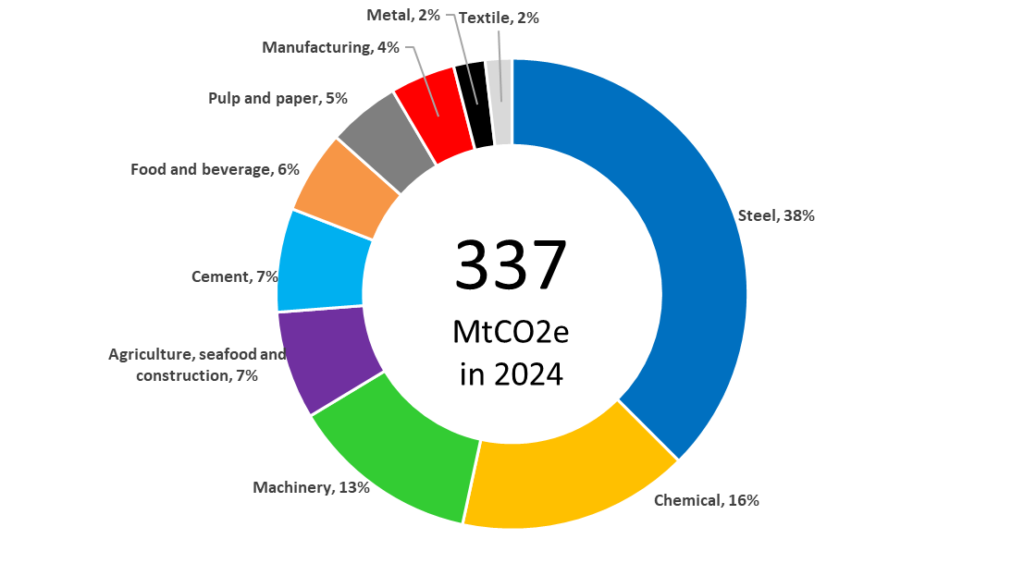

The spatial concentration visible in the maps reflects the sectoral arithmetic shown in Figure 3: out of 337 MtCO₂e generated by mapped industrial sectors in 2024—itself approximately 32% of Japan’s total national inventory of 1,054 MtCO₂eFN4—steel accounts for 38% and chemicals for a further 16%, together constituting 54% of the industrial sub-total, or roughly 182 Mt.FN5 Every large blast-furnace complex and major petrochemical complex visible as a blue dot in the figures sits above the 100,000-tonne threshold that triggers GX-ETS compliance, making these facilities the primary addressees of Japan’s first mandatory carbon price.FN6

Donut chart: CO2e emissions by industrial sector, Japan 2024, total 337 MtCO2e

Steel (38%) and chemicals (16%) alone account for 54% of the 337 MtCO₂e industrial total. Machinery (13%), cement (7%), and agriculture/seafood/construction (7%) complete the top five contributors. Source: National Institute of Environmental Studies.

The GX-ETS launched as a voluntary, baseline-and-credit system in FY2023 under the GX League, attracting over 700 participant companies representing more than 50% of national emissions—a broader voluntary base than most comparable schemes achieved in their preparatory phases.FN7 The transition to mandatory compliance, enacted by the Diet in May 2025 and effective from April 2026, transforms that voluntary coalition into a regulated cap-and-trade market operating on free-allocation allowances until paid auctions are phased in for the power sector from FY2033.FN8 For steel and chemical majors—whose facilities are clearly legible as the largest blue dots in Figures 1 and 2—the implication is a multi-year window during which allowance allocation methodology, benchmark-setting, and the treatment of J-Credits and JCM Credits as offsets will determine whether the carbon price translates into genuine abatement investment or primarily functions as an accounting exercise.FN9

The GX-ETS mandatory threshold of 100,000 tCO₂/year is a precise regulatory scalpel: it captures Japan’s most emissions-intensive industrial assets—the thermal power plants and integrated steel and chemical complexes visible on the coast from Fukuoka to Chiba—while leaving smaller emitters outside the compliance perimeter for now. The 337 MtCO₂e industrial total, and especially its steel-and-chemical core of 54%, means that Japan’s path to its 2030 NDC and 2050 net-zero target runs directly through the board rooms of a few dozen heavy-industry conglomerates. The maps make that geography of obligation concrete.

What remains to be tested is whether the carbon price signal—currently modest, with free allocation dominant until the 2030s—will be sufficient to accelerate the capital-intensive transitions required: hydrogen-direct-reduction steelmaking, electrified steam crackers, and CCS on legacy cement and chemical assets. If allowance benchmarks are set generously and offset eligibility remains broad, regulated firms may meet compliance targets without meaningful emissions reductions. Conversely, a tightening benchmark trajectory aligned with Japan’s 2030 target of 46% below 2013 levels would make the GX-ETS one of the most consequential industrial climate policies in the Asia-Pacific. The FY2026 calculation year will be the first evidentiary test.

Japanese translations

GX-ETS の監視下に入る日本の主要産業排出源

この地図は、日本国内で年間10万トン以上のCO₂eを排出している火力発電所、製鉄所、化学コンビナートを示しており、これらの施設はGX-ETSの規制対象となる。

2026年度から義務的な排出量取引制度が始まるにあたり、規制対象施設の地理的分布は、すでに産業部門CO₂eの54%を占める鉄鋼と化学が、この制度の実効性を左右する中心的セクターであることを明確に示している。

日本のグリーントランスフォーメーション排出量取引制度(GX-ETS)は、最も重要な転換点を迎えた。2025年5月、国会は年間10万トン以上のCO₂を排出するすべての施設に対し、2026年度から制度参加を義務付ける法改正を可決した。FN1 この規制により、約300〜400社が対象となり、日本国内の温室効果ガス排出量の約60%をカバーすると見込まれている。FN2 これは抽象的な政策文言ではなく、以下の図に示されるように、太平洋ベルト地帯、大阪湾岸工業地帯、そして東京・横浜を囲む京浜工業地帯に集中する大規模排出施設という、極めて具体的な産業地理に直結している。FN3

地図に見られる空間的集中は、図3に示したセクター別の構成比とも一致する。2024年にマッピングされた産業部門の排出量337 MtCO₂e(日本全体1,054 MtCO₂eの約32%)のうち、鉄鋼が38%、化学が16%を占め、両者で54%(約182 Mt)に達する。FN4–5 図中の青いドットで示される高炉一貫製鉄所や主要石油化学コンビナートはすべて、GX-ETSの義務対象となる10万トン閾値を超えており、日本初の義務的カーボンプライスの主要な対象者となる。FN6

GX-ETSは2023年度にGXリーグの下で自主的なベースライン&クレジット制度として開始され、700社以上が参加し、国全体の排出量の50%超をカバーした。これは準備段階としては国際的にも広い参加基盤である。FN7 2025年5月に可決され、2026年4月に施行される義務化によって、この自主的枠組みは、2033年度以降に電力部門から段階的に有償オークションが導入されるまで、無償割当を中心としたキャップ&トレード制度へと移行する。FN8 図1・図2で最大の青いドットとして示される鉄鋼・化学大手にとっては、この移行期における排出枠の割当方法、ベンチマーク設定、J-クレジットやJCMクレジットの扱いが、カーボンプライスが実際の設備投資を促すのか、それとも会計処理にとどまるのかを左右する。FN9

GX-ETSの10万トン閾値は、極めて精密な規制スケーリングである。福岡から千葉に至る沿岸部に立地する火力発電所、製鉄所、化学コンビナートといった日本の最も排出集約的な産業資産を確実に捉えつつ、より小規模な排出源は当面の義務対象外としている。 337 MtCO₂eという産業排出量、特にその54%を占める鉄鋼・化学の中核は、日本の2030年NDCおよび2050年ネットゼロ目標が、数十社の重工業大企業の経営判断に直接依存していることを意味する。地図はその「義務の地理」を可視化している。

今後問われるのは、現在は控えめで2030年代まで無償割当が中心となるカーボンプライスが、必要とされる資本集約的な移行——水素直接還元製鉄、電化スチームクラッカー、セメント・化学設備へのCCS——を加速させるだけの力を持つかどうかである。 もしベンチマークが緩く設定され、オフセットの利用範囲が広いままであれば、企業は実質的な削減なしに制度を遵守できてしまう。逆に、2013年比46%減という2030年目標に整合したベンチマークの引き締めが行われれば、GX-ETSはアジア太平洋地域で最も重要な産業気候政策の一つとなる可能性がある。2026年度の算定が、その最初の試金石となる。

References & Notes

FN1 In May 2025, Japan enacted the amended GX Promotion Law mandating participation in the compliance ETS for companies with direct CO₂ emissions of 100,000 t/year or more. The law came into effect in April 2026. Source: IETA, Japan Emissions Trading Scheme (GX‑ETS), July 2025.

FN2 Approximately 300–400 companies are estimated to fall within scope, collectively covering around 60% of Japan’s GHG emissions. Sources: Responsible Alpha, Japan’s Carbon Emissions Trading: A Risk Mitigation Approach, August 2025; InfluenceMap, GX Basic Policy and Roadmap.

FN3 Facility locations and relative emissions magnitude are derived from an author‑compiled proprietary database and visualised using Leaflet / OpenStreetMap / CARTO. All facilities shown exceed the 100,000‑ton threshold relevant to GX‑ETS Phase 2.

FN4 Japan’s total national GHG inventory is referenced at 1,054 MtCO₂e (base year for comparison). The mapped industrial total of 337 MtCO₂e represents approximately 32% of that figure. Source: Ministry of the Environment, Japan’s GHG Emissions Data (latest reporting year).

FN5 Sectoral breakdown per Figure 3: Steel 38% (≈128 Mt), Chemical 16% (≈54 Mt), Machinery 13%, Agriculture/Seafood/Construction 7%, Cement 7%, Food and Beverage 6%, Pulp and Paper 5%, Manufacturing 4%, Metal 2%, Textile 2%. Source: Author compilation, 2024 data.

FN6 The mandatory system targets large firms in steel, energy, chemicals, and related sectors. Source: Carbon Herald, Japan To Mandate Emissions Trading For All Companies Emitting Over 100,000 Tons, November 2024.

FN7 The GX League voluntary phase (FY2023–FY2025) attracted more than 700 companies representing over 50% of national emissions. Source: ICAP, Japan GX‑ETS.

FN8 Paid auctions are scheduled to begin in stages from FY2033, initially limited to the power generation sector. Source: Carbon Direct, Inside Japan’s GX‑ETS Carbon Market.

FN9 Eligible offsets are currently limited to J‑Credits (domestic) and JCM Credits (bilateral, under Article 6.2). The offset perimeter is a key variable determining whether regulated firms can comply without operational emissions reductions. Source: IETA, op. cit.

Japan Climate Series · S1:DR← Part I: Japan’s GHG Reduction Trajectory: Progress Made, Steep Climb Ahead